Texas Roadhouse (TXRH)

Texas Roadhouse TXRH 0.00%↑ runs southwestern-style restaurants, mainly in the United States. It operates the brands Texas Roadhouse, Bubba’s 33, and Jaggers.

Quality (5/5)

Texas consistently grows its top-line low-double-digits (LDD) over time. The exception to this was the pandemic, which was out of their control. Looking at the Koyfin chart below, Texas is one of the most consistent growth stories of any company:

About 95% of Texas Roadhouses are located in the United States, with Texas and Florida having the most restaurants. The West Coast has far less locations compared to the other regions.

Out of 722 total locations, ~86% are company-owned, while the rest are franchised. All international restaurants (6% of total) are franchised. The company has contractual arrangements that grant them the right to acquire the remaining equity interest in 18 of the 20 majority-owned company restaurants and 51 of the 55 domestic franchise restaurants.

Texas’s leverage, as measured as total assets / total equity, is ~2.4X. The only debt currently on the balance sheet is $757M of operating leases.

Visibility (4/5)

There is good visibility into the number of restaurants Texas will open each year, making the top-line forecastable. Historically Texas opened around 20-30 locations per year, which should result in ~800 locations in total over the next few years. Restaurant margin dollars are also consistent. I have a Tableau public dashboard that tracks comps and restaurant margin dollars & percentage.

Texas’s recurring revenue depends on customer loyalty. Typically, restaurants have rewards programs to encourage loyalty, but this is currently not a focus at Texas Roadhouse.

I took a point off in this category due to the difficulty forecasting input and labor costs since the pandemic. This has caused restaurant margin percentage to be below the median and management’s goal of high-teens. Management also specifically cited adjustments to its general liability insurance reserves and gift card breakage adjustments as reasons for the weaker margin percentage in Q3 2023.

Texas’s business model is understandable: delicious food at a reasonable price with fantastic service. There are complexities with beef costs and laws regarding minimum wages. Luckily, management provides easy-to-understand financial statements with limited non-GAAP adjustments.

Management (5/5)

Current CEO Gerald (Jerry) Morgan took over the role in March 2021 from founder Kent Taylor. Taylor sadly took his own life after struggling with severe tinnitus. CEO Morgan has over 20 years of experience at Texas Roadhouse, joining the company in 1997. It is difficult to replace Taylor, but if anyone were to do it, Morgan was a great choice.

Over the last decade, Texas generated $1.4B of cumulative free cash flow. I calculate a return on invested capital (ROIC) ~20% on average for the last ten years. Management opportunistically repurchases shares, with a $140M repurchase in 2019 and a $213M repurchase in 2022. Texas pays a dividend, currently yielding 1.8%. Management usually increases the dividend by a mid-teens percentage, but had to pause the dividend during the pandemic, so it does not a have “consecutive” growth streak going for it right now.

Stock-based compensation is about 2% of total revenue. Insiders own 0.5% of shares outstanding.

Demand Creation (3/5)

Texas creates demand by serving hand-cut steaks and made-from-scratch sides for a fair price in an inviting atmosphere. Additional demand has come from management’s growth strategy of opening 20 new locations per year, along with adding take-out capabilities. Assisting this strategy is the overall growth of casual dining, especially in suburban areas.

The company has delivered superior returns due to its differentiated dining experience. When one walks into one of the failing suburban dining chains, no one greets you at the door, you are not smelling the fresh baked bread, and the atmosphere is non-existent. Walking into Texas Roadhouse, it almost always matches the “Legendary Food, Legendary Service” guarantee.

“Jerry Morgan Executive - CEO: Well, I think it's all of it, to be honest with you. I think we work really, really hard to present an environment are made from scratch food or handmade, all of that adds value. When you walk into that restaurant and you smell that fresh baked bread and you know that we're cooking that steak to order for you, and we've got this friendly individually. We're still hungry to serve people at an extremely high-level. And when I look at the lines that are waiting at our restaurants, it tells me that we need to continue to focus on doing the things that we do. And they're loving, the food, they're loving the service. We need to be able to execute to get them in the restaurant, provide them with an experience thank them for coming to our business because it's still important for us to serve them at a high-level. And we're trying to earn their business every single day. Somebody woke up this morning thinking about where they were going to dinner, and I want them thinking about Texas Roadhouse, Bubba's 33 and Jaggers all day long to choose to walk through our doors. So we're hungry for it. Sorry dude got me excited.” (TXRH: 2023 Earnings call Q2 2023 Transcript, 2023-7-27)

Texas benefits from having made mistakes in the past and developing a blueprint for a successful restaurant that can be repeated throughout the country. The company has advantages when it comes to selecting new locations, buying building materials, and purchasing beef. I took off a couple points in this section due to the highly competitive nature of restaurants. Switching costs for customers is low. One could argue that it is difficult to get Texas Roadhouse quality (and quantity) of food at a similar or lower price. That is definitely an advantage, but if Texas Roadhouse disappeared tomorrow, people would just eat at a different restaurant. There is nothing mission-critical in nature of Texas’s business. Plus, it was deemed non-essential, except for take-out, during the pandemic. That is a bit scary knowing your business could get shut down and told it is not needed.

Pricing & Value (3/5)

Attached below is my discounted cash flow (DCF) analysis:

Feel free to download the spreadsheet and update it with your own assumptions! I forecasted LDD revenue growth and EBIT margins around 8%. There is continued reinvestment for new locations, digital investments, etc. My estimated value comes out to ~$75/share.

For pricing, TXRH stock has a 19-year mean-P/E of 25X. This is somewhat distorted by the wild swings during the pandemic.

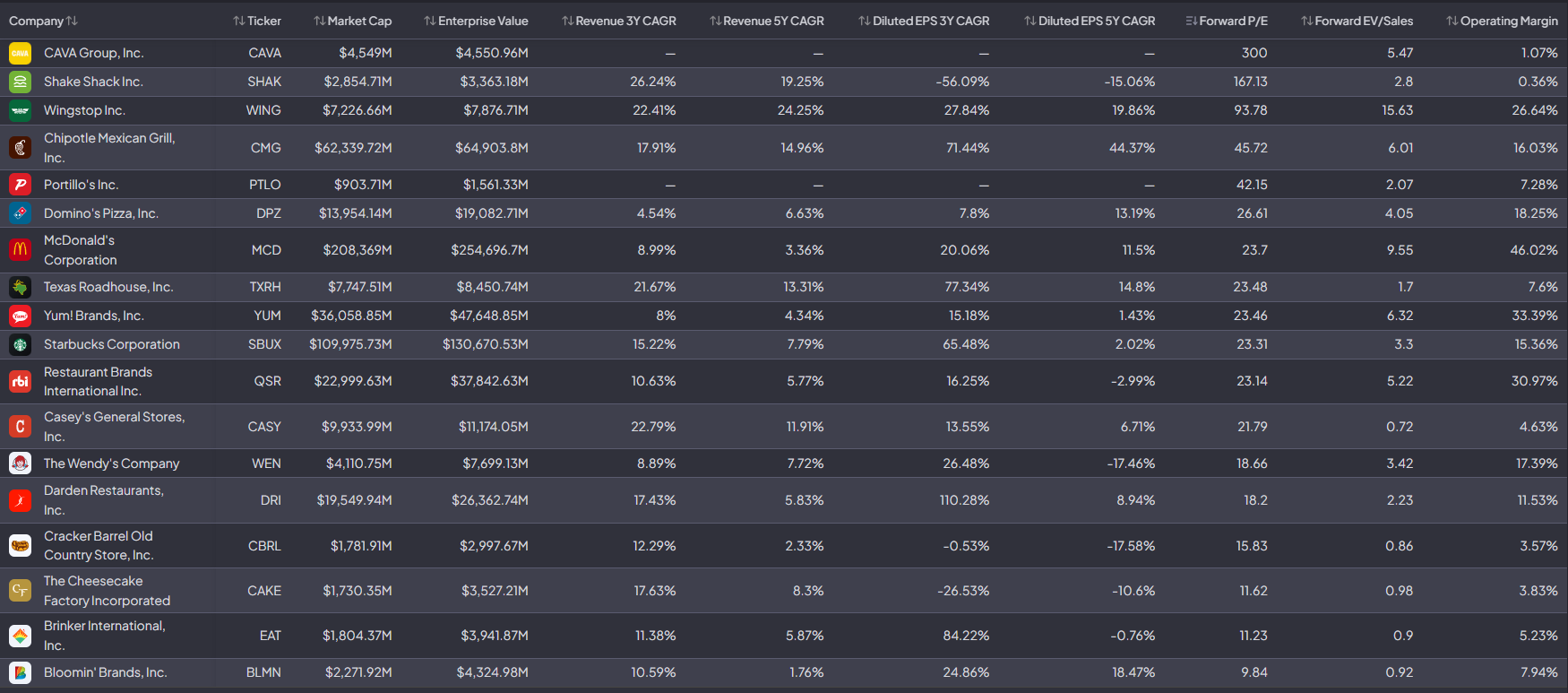

Compared to peers, TXRH is in the middle of the pack in terms of forward P/E. It is not quite as exciting as Chipotle CMG 0.00%↑ but it is a better operation than Cracker Barrel CBRL 0.00%↑ or Cheesecake Factory CAKE 0.00%↑ . I think it should trade with Domino’s DPZ 0.00%↑, McDonald’s MCD 0.00%↑ , and Starbucks SBUX 0.00%↑ around 23-25X. With TXRH’s EPS approaching $5.00, a 25X multiple would result in a price of $125/share.

Combining my valuation and pricing, I end up with a target buy-below price of $100/share, compared to $120 today. I already own TXRH stock. It has been one of my best performing positions over the last two years. This is no guarantee about future returns, but I would like to continue to hold it despite it being a bit pricey here. Since summer, shares traded from $115 to $90 back to $120 today. If it gets significantly below my buy price, I would consider making it a larger position in my portfolio.

Risks

The biggest risk right now is the prospect of a weaker U.S. consumer. Many market participants expected a recession in 2023 resulting in the U.S. consumer coming under pressure. It made sense, right? Higher interest rates, higher payments for cars & houses, higher costs for food, gas, etc., pandemic stimulus worn off, student loan payments starting again, and more. Amazingly, the consumer continued to do well, but will that continue into 2024? What if the combination of all these worries finally catches up to consumers in 2024? With the market and TXRH itself at all-time high prices, there might be more risk that consumers cannot spend as much on dining out in 2024.

Other risks include continued higher wages, input costs, and new construction costs. Although Texas focuses more on its top-line, if margins do not eventually improve to the high-teens target, it could have a negative effect on the stock.

Capex for Texas Roadhouse locations is increasing as a percentage of sales, so there is concern if future returns on investment can match or exceed the past.

In addition, weight-loss drugs were a big story in 2023. It seems like it was a lot of hype, but if the drugs start showing more proven results, it could potentially lead to lower appetites, which would lead to lower spending at Texas Roadhouse.

To conclude, Texas Roadhouse scores a 20/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below.

I recently did a review of TXRH’s Q3 2023 results in a post along with a few other companies, found here:

Disclosure:

I own TXRH stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.