MSA Safety (MSA)

MSA Safety MSA 0.00%↑sells safety equipment to firefighters, construction sites, and other industrial customers. The company was founded in 1914 and has a market cap of $7 billion today.

Quality (4/5)

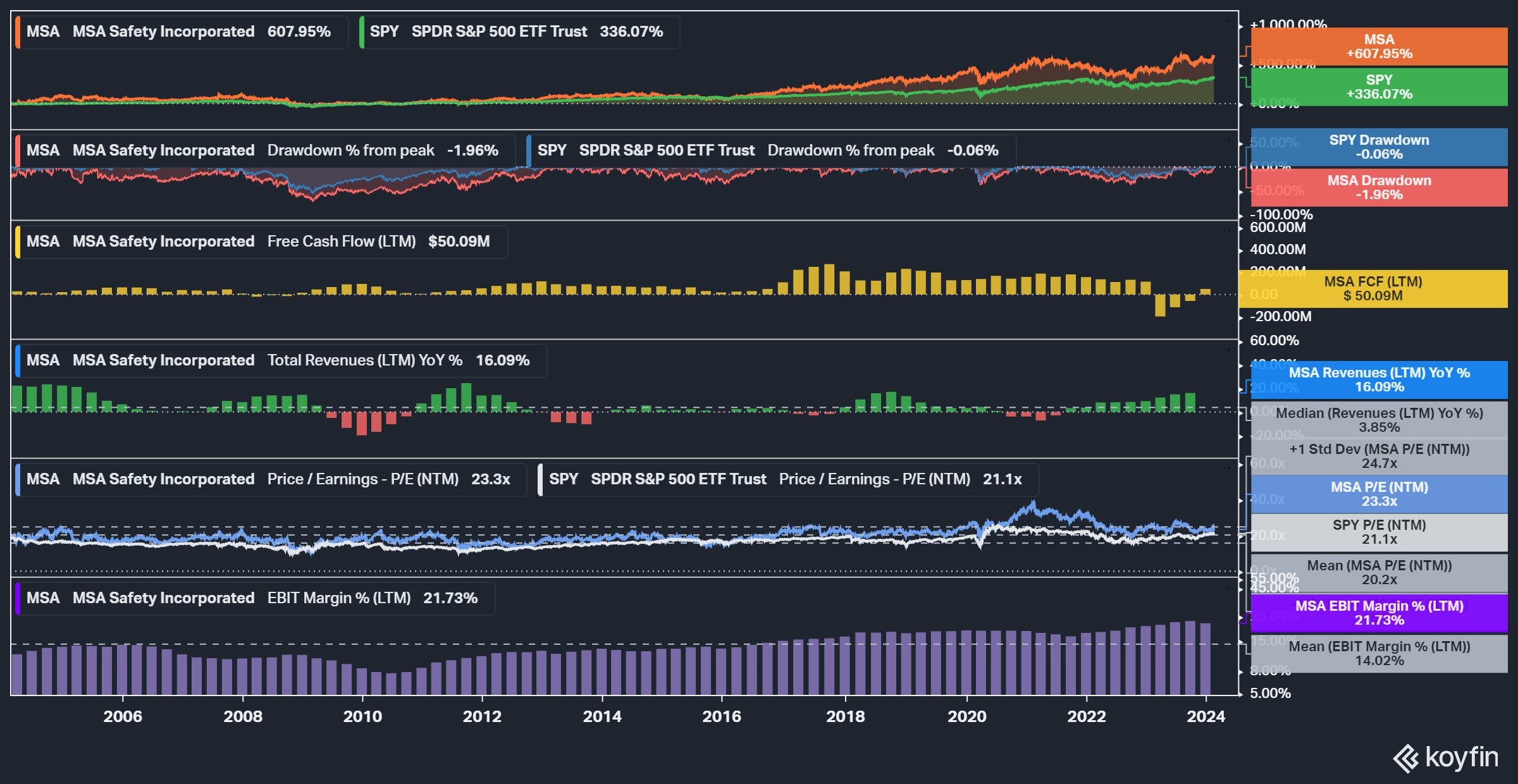

MSA historically grows revenue in the low-single to mid-single-digits range (LSD-MSD). Full year 2023 net sales grew 17%, which included 16% organic growth (positive pricing and volume) and 1% from currency.

There have been numerous sales declines for MSA over the last twenty years in 2009-2010, 2013, 2017, and 2020-2021. This looks like a cyclical business, to me, that can continue to grow LSD-MSD through the cycle.

MSA has paid increasing dividends for 54 consecutive years.

About 68% of sales are to the Americas.

Leverage, measured as total assets / total equity, is relatively high in the 2.2-2.5X range compared to peers that are mostly at 2X or below. The amount of leverage does not seem to be excessive, though, and management is committed to reducing it in the near-term.

Visibility (3/5)

Management says that 20-30% of revenue is recurring.

Within the detection business, we had the fixed detection business, which is attached to a building. So a lot of recurring revenue that comes to that business. You attach that to a building. There's a 10-year-plus cycle. So again, no matter what's going on in the economy, you still got to protect in these critical safety environments we're in. (MSA: 2023 2023 Baird's Global Industrial Conference Transcript, 2023-11-8)

Nish talks a lot about the technology and the software that we're launching. The other thing that we've always enjoyed is replacement parts and sensors and things of that nature. And so, for example, in fixed gas and flame detection, it might sit on a rig or a refinery for 10 or 15 years. But over that time period, what happens is you're replacing parts, you're replacing sensors. So -- and that recurring revenue has a very attractive margin profile to it, and that represents maybe 20% to 30% of our overall business is that replacement parts. But what's exciting is what Nish alludes to is all the exciting things that are coming with respect to the connected worker, not only on the portable gas side, but we enjoy such a strong position on the worker that it allows us to leverage and to monetize that position quite nicely.” (MSA: 2022 William Blair’s 42nd Annual Growth Stock Conference 2022 Transcript, 2022-6-6)

While that is a nice chunk of recurring revenue, obviously the other 70-80% is non-recurring and subject to cyclical end markets that make forecasting difficult in the short-term. For example, management noted low visibility in the second half of 2024 in its outlook presented during the latest earnings call.

While the gas detectors and helmets that MSA provides are mission-critical, I find that they are rather boring products relative to the hyped-up AI tech out there today, which is nice. However, less boring are the financial statements, in which management frequently uses non-GAAP (NG) adjustments, as seen below:

It seems strange to adjust out “one-time” restructuring costs that appear to happen every year for at least the last ten years. In FY23, NG/GAAP earnings had a 5x ratio.

Management (5/5)

My initial impressions are positive for MSA’s management team. Nish Vartanian is the Chairman and CEO. According to his LinkedIn, Nish started at MSA in 1985 as a sales manager. That is awesome to see him move up the ranks to CEO. I would prefer the Chairman and CEO roles to be independent, however.

Right before publishing this post, MSA put out a press release announcing a CEO transition.

MSA elected Steve Blanco Chief Executive Officer, to be effective May 10, 2024. The Board has also elected Mr. Blanco as a director of the company, effective immediately. Mr. Blanco, 57, currently serves as MSA's President and Chief Operating Officer. His election is part of a planned management succession and coincides with a decision by MSA Chairman and CEO Nish Vartanian to inform the Board of Directors that he intends to retire as CEO in May of this year. Mr. Vartanian announced his retirement and Steve's election this afternoon at a planned meeting of the company's global leadership team.

Mr. Blanco joined MSA in 2012 as Vice President of Global Operational Excellence. In 2017, he was named President of MSA Americas, responsible for the company's business in the U.S., Canada, and Latin America. Under Mr. Blanco's leadership, from 2018 through 2022, revenue in the company's Americas segment grew by more than 40 percent.

CFO Lee McChesney took over in October 2022 after working at Stanley Black & Decker for 23+ years. It looks like he left as Stanley was struggling in a 67% drawdown post-pandemic.

Management is incentivized by the stock price, total return, revenue growth, net income, adjusted EBITDA margin, net sales, and working capital, according to the latest proxy.

I would prefer seeing metrics like return on invested capital (ROIC) or free cash flow (FCF) here.

Over the last decade, management delivered $1.35B of cumulative FCF while spending $0.8B on acquisitions. I calculate that ROIC has been in the mid-to-high-teens.

Management is trying to transform the company into a “higher growth, higher returns” business. I suppose that is nearly every management team’s goal! But it is good to see the actions listed above, along with the solid growth and margin expansion in recent years.

Stock-based compensation (SBC) is 2% of net sales. Insiders, mainly former CEO John Ryan III, own 6.2% of shares out. Ryan III owns 5.6% of shares.

Demand Creation (3/5)

I see some ability to create demand in MSA’s business. When I went shopping for a portable gas detector, I found distributors that typically had an MSA detector for sale next to a Teledyne, 3M, and/or Honeywell detector. Why would I buy MSA over Teledyne? There were no prices listed, so I suppose one could potentially be less expensive than the other.

Another reason could be that MSA’s software that goes along with its gas detectors may be better. If a customer already has MSA’s software, that would be a good lock-in to buy MSA detectors now and in the future. Switching this mission-critical product over to a competitor could be difficult and expensive, while exposing the safety of workers and infrastructure.

Knowing MSA’s 100+ year history of protecting workers could give customers confidence that its products are the right ones to go with to provide safety. There are numerous laws and requirements for health and safety in the workplace, so having a knowledgeable partner like MSA could prevent costly mistakes.

Management talked about its Fire Service business having 1 out of every 2 wins being a competitive conversion. It sounds like its competition had to leave the market because they did not comply to the latest standards.

“Sure. The competitors that have exited the market have created, obviously, a nice opportunity for us. So -- but it's pretty well split between those players that are still in the market and those who have exited. So we've had a few competitors who no longer have NFPA-compliant breathing apparatus that compete in the marketplace. So we've seen 2 competitors out of 6 fall out of the market. One came out of the market for 3 or 4 years and then came back and finally we got their NFPA approval. So they're back in the space. But for the most part, there are 2 players that have the majority of the business, and that's us and one other competitor.” (MSA: 2023 2023 Baird's Global Industrial Conference Transcript, 2023-11-8)

“So NFPA standards, you typically see those promulgated every 5 years on a 5-year cycle. And municipalities don't like to be more than 2 cycles out on NFPA standard, so they'll buy. And if there are 2 NFPA standards, they'll typically buy before that third standard hit. So that's another piece that drives the replacement cycle of the breathing apparatus. And then also those standards create significant barriers to entry. I talked about other competitors dropping out of the market. The fact of the matter is their share fell to a point and the investment required to meet those standards. It just didn't make sense for them to be in the marketplace so they fell out. So the barriers that come into the space of self-contained breathing apparatus and helmets, quite frankly, the fire helmets -- that's significant. So that's a nice moat around the business for us as you look at that business going forward.” (MSA: 2023 2023 Baird's Global Industrial Conference Transcript, 2023-11-8)

It sounds difficult to enter the market and compete with MSA due to safety requirements which creates a moat around MSA’s business. However, demand creation is not always possible because sales depend on employment and construction. If there is less employment, there are less heads to protect. If there is less construction, there is less fall protection or gas detection needed.

Valuation & Pricing (2/5)

Attached below is my DCF analysis

I set revenue to grow MSD over the next ten years. I think the 17% growth most recently will wear off as it becomes more difficult to raise prices. I know management points to adjusted EBIT margins of over 20% currently, but I am only adding back the amortization of acquired intangibles, which leaves a 14% margin. This might be too conservative, but even if I used the entire adjusted EBIT amount of $398M, my estimated value only increases by $10, so it does not really change my conclusion.

You can see my estimate cost of capital at about 7.7% and ROIC in the mid-teens. I end up with an estimated value per share of $104 vs. the current price of $178. Revenue growth needs to consistently be in the double-digits with margins improving to 30% for the current price to make sense. When looking at peers, those metrics do not seem likely, in my opinion.

For pricing, MSA typically gets a slight premium to the S&P 500 P/E multiple. MSA’s current P/E multiple is in the middle of the pack for its peer group. Maybe if it can continue to reduce debt, increase growth, and improve its ROIC, it could get a 25-30X multiple. But for now, I think 22X is fair on EPS approaching $8.00.

Combining my valuation and pricing, I get a target buy-below price of $140/share. I am pretty interested in this one after my initial look. It is definitely going on the watchlist.

Risks

I think the main risk now is MSA’s dependence on the cyclical construction & industrial markets. Based off recent looks at Hubbell and Eaton, there appears to be no shortage of mega-projects that require construction. But, when listening to CoStar’s latest earnings call, their CEO mentioned slowing construction starts in commercial real estate. That part of the market could be a headwind. For the fire safety business, it appears that fires are becoming more frequent due to climate change, so that should result in more firefighter gear required over time.

A major risk, which was reduced recently, had to do with product liability.

On January 5, 2023, the Company divested Mine Safety Appliances LLC ("MSA LLC") a wholly owned subsidiary that holds legacy product liability claims relating to coal dust, asbestos, silica, and other exposures, to a joint venture between R&Q Insurance Holdings Ltd. and Obra Capital, Inc. In connection with the closing, MSA contributed $341 million in cash and cash equivalents, while R&Q and Obra contributed an additional $35 million. As a result of the transaction, MSA will derecognize all legacy cumulative trauma product liability reserves, related insurance assets, and associated deferred tax assets of the divested subsidiary from its balance sheet in the first quarter of 2023. R&Q and Obra have assumed management of the divested subsidiary, including the management of its claims.

It was good to get some legacy product liabilities off the books. We will have to keep an eye out for any further product liability issues in the future.

Finally, I am also concerned about its M&A integration. Asset turnover is trending down from >1X to 0.7X today. Goodwill & intangibles are 41% of total assets. Further deterioration of asset turnover could indicate write-downs in the future.

To conclude, MSA Safety scores a 17/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below.

Disclosure:

I do not own MSA stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.