Hubbell (HUBB)

Hubbell, founded in 1888, makes electrical and utility products, specializing in the power transmission infrastructure.

Quality (4/5)

Hubbell typically grows revenue by a mid-single-digit percentage (MSD). The company has a strong track record for growth in sales, earnings, cash flow, and dividends, as seen in the Koyfin historical chart below:

Over 90% of revenue comes from the United States. Hubbell has 17 consecutive annual dividend increases at a MSD-HSD rate. Leverage is not excessive at 2.1X (measured as total assets / total equity).

Sales declined in 2009-2010 and 2019-2021 on a trailing 12-month basis. Hubbell runs an acquisition strategy, so some of the larger increases in sales are due to acquired sales. EBIT margin recently increased greatly after a 5+ year decline.

Visibility (3/5)

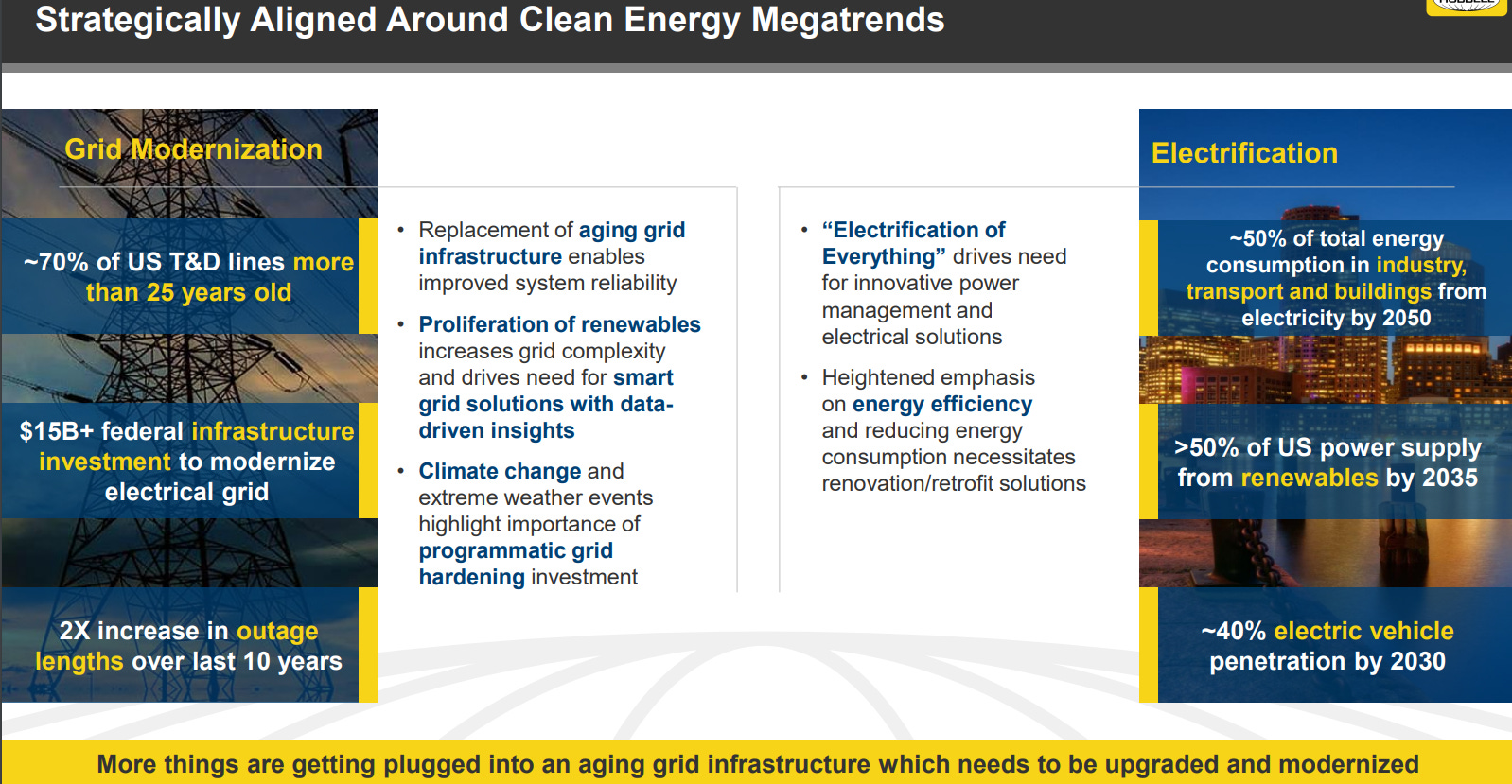

Hubbell has increasing visibility as management reduces its cyclical exposure and simplifies its Electrical segment reporting structure. In the early 2010s, Hubbell’s main talking points were around oil & gas markets and non-residential construction. Today, the focus is on clean energy megatrends, as seen below:

Hubbell transformed from a “holding company” to an “operating company”, leading to improved alignment, collaboration, and functional expertise leading to more consistent and predictable performance.

Hubbell has very little software and subscription sales today because utilities are slow to adopt SaaS solutions. However, there is a replacement cycle for infrastructure and hardware in which customers prefer to replace items like-for-like, leading to repeat sales for Hubbell. Backlogs are elevated today due to strong demand in grid modernization, electrification, and U.S. reshoring projects.

Management (4/5)

The management team saw many new faces right before the pandemic including a new VP of Global Operations, Chief Technology Officer, Chief Information Officer, multiple Group Presidents, and more. Current CEO Gerben Bakker took over the role in 2020. He is also the Chairman and President. The separation of the Chairman and CEO roles would be preferable. CEO Gerben is highly experienced, beginning his career at Hubbell in 1988 as an engineer.

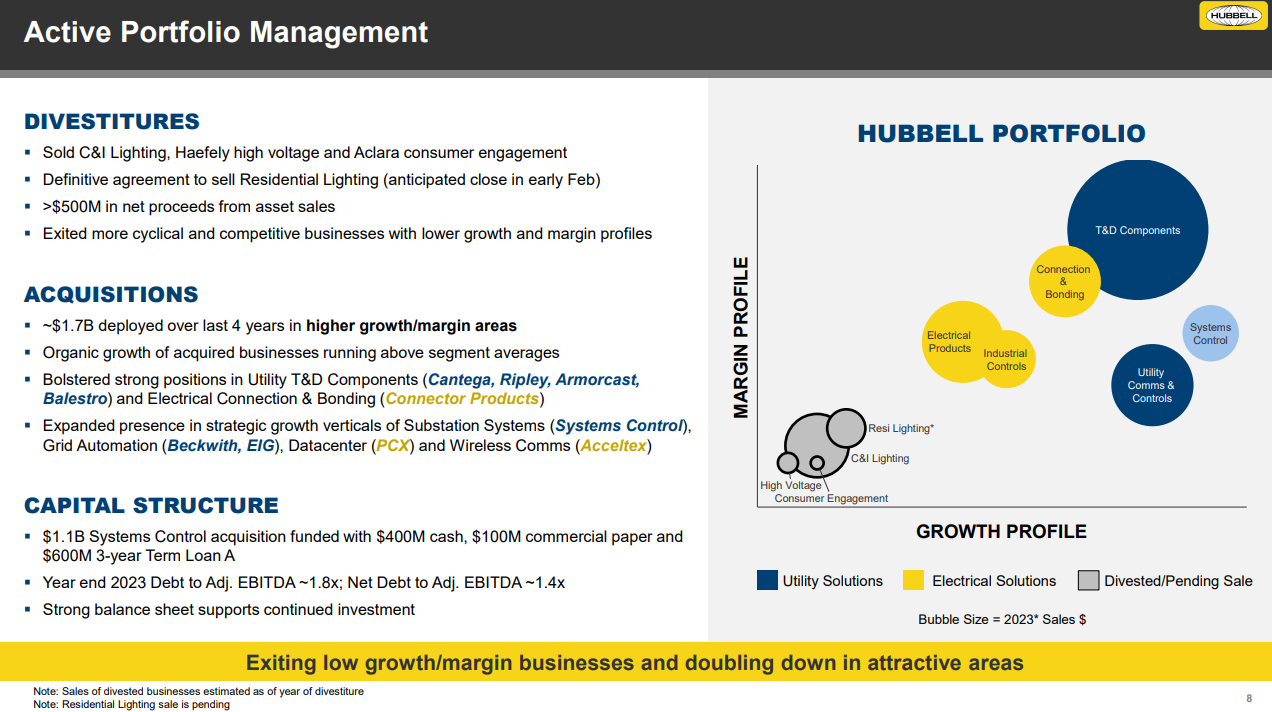

Hubbell has long run an acquisition strategy, highlighted in the slides below:

Management is focused on high-growth areas like data centers, utilities, and telecommunications. Abundant opportunities exist due to fragmented markets and companies seeking better platforms.

Over the last decade, Hubbell spent $2.2B on acquisitions (the chart above just covers “bolt-on” acquisitions), while generating $3.9B in FCF. About $0.9B was spent on share repurchases. Management generated a low-to-mid-teens ROIC on average over the last ten years.

Stock-based compensation is low at <1% of total revenue. Insiders own <1% of shares outstanding. It would be nice to see higher insider ownership.

Demand Creation (4/5)

As mentioned in the Visibility section above, I believe Hubbell has higher demand creation ability today than ten years ago. While it still relies on some cyclical end markets, management positioned the company to take advantage of mega-trends. For example, Hubbell is in a good spot to sell to utilities that need to upgrade aging grids. As more electric vehicles (EVs) and data centers that require high electrical loads are added to the grid, this will expose infrastructure that is due for upgrades. Customers typically prefer to replace components like-for-like, so they will turn to Hubbell. Hubbell has the size and scale to meet these large, demanding projects.

With 100+ years of history and domain expertise, the Hubbell brand is recognized by customers for providing quality and reliable products. Hubbell generally sells small components to higher-costing utility grid projects. It is a low relative cost for customers, but there is a high cost of failure, allowing solid margins for Hubbell.

I have some concerns about demand creation ability in segments like residential lighting.* How advantaged is Hubbell here? I need to buy new fans and lights for my house, so I will find out soon myself. If Hubbell disappeared tomorrow, that would likely be a big problem for the utilities operating the electrical grid, but I could probably find another company to buy ceiling fans from.

Valuation & Pricing (3/5)

Attached below is my discounted cash flow (DCF) analysis:

Feel free to download it and enter in your own assumptions! I am curious what other investors think.

I modeled in growth slightly higher than historical at 9%, declining to 6% in years 3-5. Hubbell could see a nice ramp up as it clears its backlogs and continues to benefit from these clean energy trends. I set EBIT margin to tick up to 22% over time. I am concerned to set it much more than that with the starting point being so high already (double the EBIT margins of the electrical equipment industry). My estimated value/share comes out to $298 vs. the current price of $331 which is actually quite reasonable compared to most of my valuations over the last few months.

Pricing does not look so bad either:

Hubbell is in the middle of the pack at about 20X forward earnings. See how this compares historically:

It is relatively expensive compared to its historical pricing (usually a market multiple with market growth), but not bad compared to US industrials and the US as a whole. With EPS approaching $16.30, a 20X multiple results in $326/share.

Combining my valuation and pricing, my target buy-below price would $312/share, which is only 5% below today’s price. With a solid Mark Score of 18/25, Hubbell rises near the top of my watchlist!

Risks

I am concerned about customer concentration, as Hubbell’s top ten customers make up 43% of total sales. The high switching costs reduce this risk since its customers would lose access to Hubbell’s portfolio of quality brands, thousands of custom SKUs, simplified central billing and sales support, and reasonable prices. Next, as with any company with an acquisition strategy, I worry about integration risks and write-downs. Asset turnover was in decline (from >1X to around 0.6X) but it is now improving, reducing my worry. Finally, Hubbell still has cyclical end markets despite its repositioning, so any declines in industrial markets due to macroeconomic factors could negatively impact results and make my assumptions wrong. Increasing software sales with recurring revenue could offset these declines in the future.

To conclude, Hubbell scores a 18/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below.

*Since writing this, Hubbell released Q4 2023 earnings and its outlook for 2024.

Included in the release was an update on acquisitions and divestitures:

“During the fourth quarter, the Company acquired Northern Star Holdings, Inc. (commercially known as Systems Control), a manufacturer of substation control and relay panels, for approximately $1.1 billion, using cash and cash equivalents and the proceeds from a $600 million term loan.

The Company also entered into an agreement during the quarter to sell its residential lighting business for a cash purchase price of $131 million. The residential lighting sale is subject to customary closing conditions, including regulatory approvals, and is expected to close in the first quarter of 2024.” (HUBB: 2024 8-K, 2024-1-30)

This portfolio activity will help in my Demand Creation score. I am going to leave it at a 4/5 for now. If Hubbell continues to deliver volume growth in addition to its pricing gains, this could increase to a 5/5 in the category.

In Q4 2023, Hubbell saw 8% organic growth and 2% growth from acquisitions, noting volume growth in both Utilities and Electrical.

Here is the outlook for 2024:

Management sees MSD organic growth, plus 5% net growth from acquisitions & divestitures. Adjusted EPS is expected to be between $16.00 and $16.50, which is in-line with my estimate above.

Disclosure:

I do not own HUBB stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.