CSW Industrials (CSWI)

CSW Industrials CSWI 0.00%↑ is a $3B market cap manufacturer of parts for the HVAC, building products, and plumbing markets. It was founded in 2015 after spinning off from Capital Southwest Corporation CSWC 0.00%↑.

Quality (4/5)

Since CSWI’s inception, its revenues have grown organically at a low-double-digit rate (LDD). With acquisitions included, growth is in the mid-to-high teens. While this high growth rate may be difficult to sustain, CSWI’s smaller size (<$1B of annual revenue) could allow it to continue to outpace the HVAC industry, which is going through a down cycle after a burst of growth during the pandemic.

As seen in the historical chart above, CSWI has a strong track record for growth in sales, earnings, and cash flow. The only revenue declines so far were during 2016 and 2017.

CSWI records 94% of total sales in the Americas and has relatively low leverage on its balance sheet at 1.6X (total assets / total equity).

Visibility (3/5)

CSWI’s management notes having “a lot” of consumable product sales, leading to decent visibility over a 6-12 month timeframe. I could not find an exact percentage of consumable sales. There also does not appear to be any software aspect to the products it sells. This could make it difficult to forecast demand for CSWI beyond 6-12 months. The Engineered Building Solutions segment is a small percentage of total sales, but it has multi-year projects that increase forecasting ability. Higher interest rates or economic uncertainty could cause delays to these projects.

“The repeatable consumption of many of our products that are used either in maintenance, repair and replacement applications or to enhance the reliability, performance and lifespan of mission-critical assets. The products we sell and contract are solutions and specialized reliability solutions, and the value they provide are often nondiscretionary fundamental necessities for both homeowners, businesses and the utility sector.” (CSWI: 2024 Earnings call 3 2024 Transcript, 2024-2-1)

“The only thing I'd add to that, you raised the R word, recession. And that is, we can't predict, but we are absolutely prepared. Diversified in end markets, diversified across our product portfolio, diversified businesses, we have a really strong balance sheet, just real strong cash generation. And we have a lot of consumable type products and non-discretionary. And so, those are the attributes that our business has that makes us more resistant to cycles. And so, certainly, just to add to what James said, I think our business is especially resilient, and so we're prepared, almost regardless of what the economic cycles are.” (CSWI: 2023 Earnings call Q4 2023 Transcript, 2023-5-25)

There is relatively low reliance on fast-moving tech and science, which reduces the worry that growth rates will suddenly drop due to obsolescence or competition.

CSWI is underfollowed by the sell-side with only two analysts covering the earnings calls and no appearances at industry events. The simple and boring nature continues in the company’s financial statements, with limited usage of non-GAAP adjustments (1.1X NG/GAAP earnings) and fancy performance indicators & TLAs.

Management (3/5)

Joe Armes is CSWI’s Chairman, CEO, and President. He has been the Chairman and CEO since inception in 2015. It would be preferable to have the Chairman and CEO roles independent. James Perry is the CFO since 2020, previously working at a railroad company, Trinity Industries.

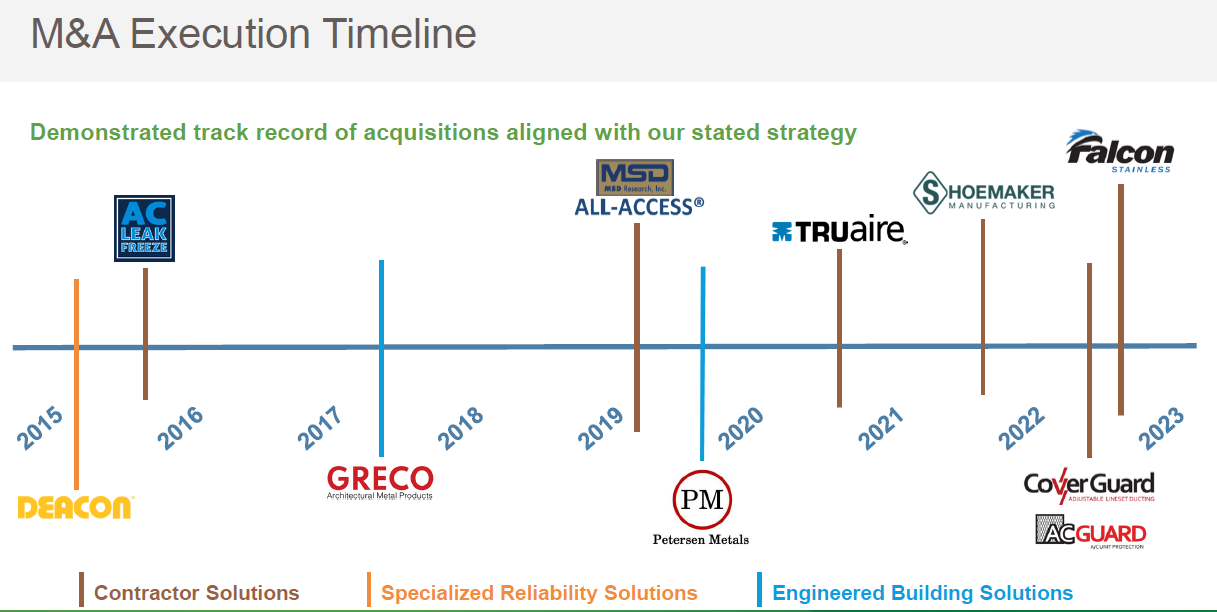

Over the last decade, I calculate cumulative free cash flow (FCF) of $464M with $560M spent on acquisitions.

The largest acquisition was TRUaire:

During the year ended March 31, 2021, we acquired TRUaire for $286.9 million (after working capital adjustment) in cash consideration and stock consideration valued at $97.7 million.

TRUaire, based in Santa Fe Springs, California, is a leading supplier of passive air handling solutions for residential and commercial applications, offering a broad suite of high-quality products including grilles, registers and diffusers (GRD). TRUaire sells through wholesale distribution and retail channels, with HVAC/R technicians and homeowners as primary end users. During calendar year 2019, approximately 86% of TRUaire’s business served residential customers in the HVAC/R end market, while the remainder served commercial customers.

Overall, CSWI’s Return on Invested Capital (ROIC) is in the low-double-digits to mid-teens, nicely above my estimated cost of capital.

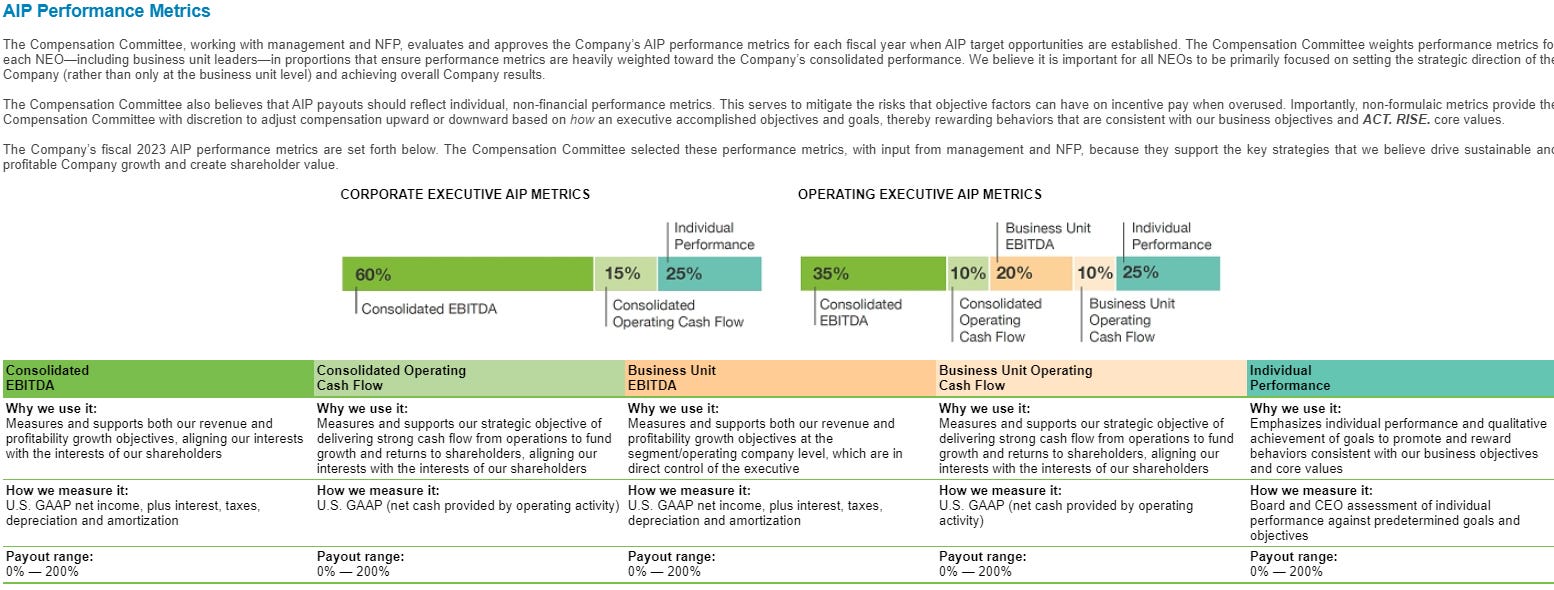

Management is incentivized by EBITDA margins and operating cash flow. I would prefer to see metrics like ROIC or free cash flow, but this is OK.

Stock-based compensation is about 1.5% of total revenue. Insiders own 1.3% of shares outstanding. Again, I would prefer to see higher insider ownership, but overall management seems to be well-aligned with shareholders.

Demand Creation (4/5)

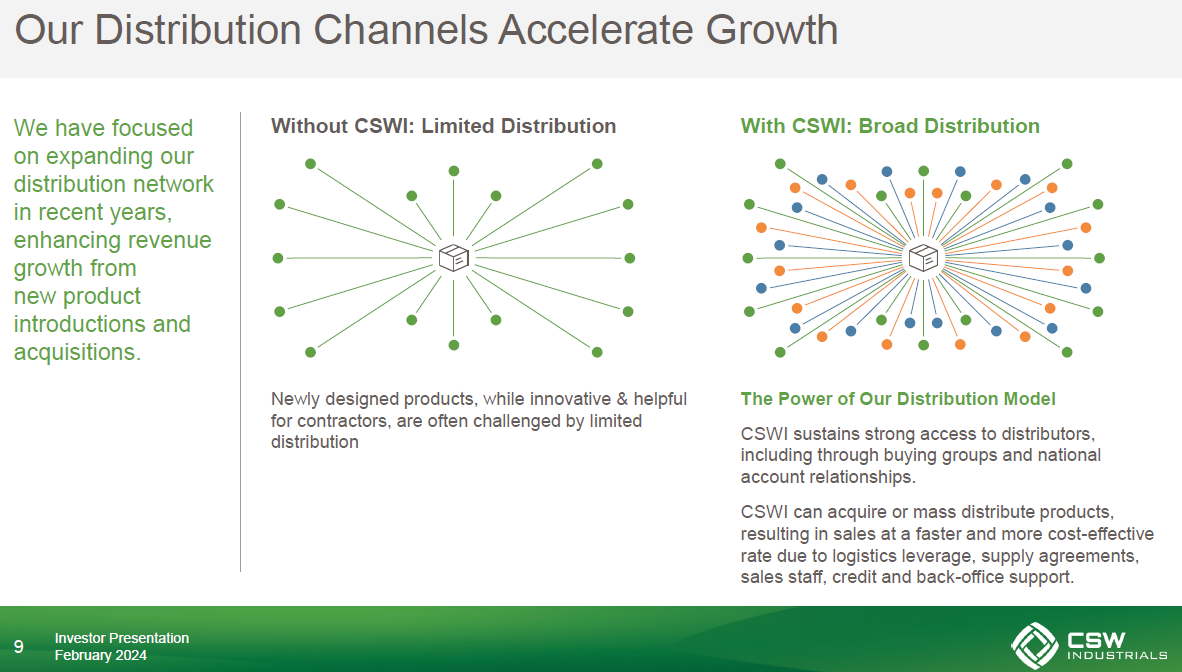

It appears that CSWI can create some demand using its broad distribution model. CSWI’s newly designed products or acquired products can access its relationships with distributors to increase demand that would not be possible otherwise.

“The third quarter is seasonally our slowest quarter of the year for our Contractor Solutions segment, but our team did an excellent job by not only delivering another quarter of market outperformance but also year-over-year growth despite the HVAC/R industry experiencing a decline in residential volumes. Contractor Solutions delivered Q3 net revenue of $115.4 million, an increase of 3% over the prior year period. Our competitive advantage in this segment centers around our distribution channel, introducing innovative, high-value products and focusing on acquisition integration. The power of our distribution model allows CSWI to acquire, integrate, master distribute and accelerate growth on newly designed products. This results in faster and more profitable sales because our strong relationships with wholesalers, our sales network, logistics leverage, credit and back office support, allowing us to focus on serving our customers well.” (CSWI: 2024 Earnings call 3 2024 Transcript, 2024-2-1)

While CSWI was founded in 2015, its portfolio of brands dates back nearly 100 years ago. One of CSWI’s key brands, RectorSeal, was founded in 1937, for example. Customers see this brand and others under the CSWI umbrella as high-quality, reliable products.

As seen in the product slides above, CSWI’s offerings have a relatively low cost to the overall project that its end customer is working on. Many of its products are needed for mission-critical applications, as well. If your HVAC or plumbing system breaks, one typically does not wait long to get them fixed. The repair company will want to use a dependable product with readily available supply, which CSWI’s brands can provide. However, some products like its vents sold at Home Depot, do not seem to have the same level of demand creation ability, in my opinion. How often does a homeowner or building owner replace its vents? I feel like sales of vents would be tied more to home construction trends. In addition, some of those specialty chemical products that CSWI sells tied to oil & gas and mining markets appear to have minimal demand creation ability.

Given CSWI’s smaller overall size, it could face competition from larger companies, like 3M, which offer more products and have more distribution access, along with larger manufacturing size and scale.

Valuation & Pricing (2/5)

Attached below is my discounted cash flow analysis (DCF):

Feel free to download my spreadsheet and enter in your own assumptions. I think CSWI could struggle to maintain the pandemic-fueled growth, so I set revenue to grow only 7% the next couple of years before accelerating back to a LDD growth rate. I also wonder whether CSWI can keep expanding margins? Its 20% EBIT margin is almost double the industry average already, so I put minimal margin expansion in over the next decade. I might be too conservative here if CSWI’s pricing actions or cost reductions accelerate more than expected. You can see my estimated ROIC in the mid-teens, above my cost of capital at about 8.5%. My estimated value per share comes out to $145, which is 30% below the current price.

The pricing story is similar:

CSWI carries one of the highest P/E multiples relative to its peers at 30X. Its metrics are very similar to AAON with near 20% revenue 5YR CAGRs, 20% EBIT margins, and about 1.5X leverage. However, AAON’s ROIC is over 20% compared to CSWI’s mid-teens. CSWI’s stock price has the largest increase over the last five years compared to peers.

In addition, from the Koyfin history chart at the beginning of this post, one standard deviation above CSWI’s mean P/E is 25X. With EPS approaching $7.75, I think $194 is a fair pricing assessment.

Combing my valuation and pricing, I get a target buy-below price of $170/share, 22% below today’s price.

Risks

My main risk right now would be if the HVAC cycle turns down further. The HVAC distribution channel is going through a period of destocking. I attached Carrier’s latest earnings report below which details its view on the HVAC market. North America resi HVAC has been down mid-teens but it appears orders are starting to pick up. Any further housing weakness could potentially impact CSWI’s future results. This is more of a short-term risk, I think. Longer term, there appears to be strong growth drivers:

“We continue to experience rising temperatures, higher homeowner expectations for comfort and a growing installed base, driven in part by a housing shortage. We believe these dynamics provide a backdrop where we can deliver long-term value for our shareholders.” (CSWI: 2024 Earnings call 3 2024 Transcript, 2024-2-1)

The next risk would be supply chain related due to CSWI having its manufacturing plants in Vietnam. This exposes the company to increases in shipping costs like what happened during the pandemic and other events like the Red Sea currently.

“We do have some shipments from our Vietnam facility that will travel through the Suez Canal normally. Those shipments have all been rerouted. So they're all going south around the south tip of Africa, as most shipments are. We have other shipments that go different directions, of course. But those have been rerouted. You have seen an increase in pricing. As you know, pricing was down a couple of thousand dollars a few years ago, got up to $20,000-plus back to a couple of thousand. We're seeing rates out there, call it $4,000 or so. You've seen things pop. We expect that this is rather temporary for now. We'll see. It's only been a few weeks. But number one, our cargo is safe. It's being rerouted. Things take a little longer to get here. This is also the time that we've spent the last couple of weeks -- as a lot of manufacturers have -- been stocking up because you have the Tet holiday when all production shuts down for 10 or 12 days in Asia, us being no exception. That starts, I think, on Saturday, in fact.” (CSWI: 2024 Earnings call 3 2024 Transcript, 2024-2-1)

Finally, as with any company carrying out an acquisition strategy, I am concerned about acquisitions integration risks and write-downs. CSWI’s asset turnover declined from about 1.0X to 0.8X in recent years. That is not particularly concerning but worth keeping an eye on. CSWI’s balance sheet is 55% goodwill and intangible assets. In addition, CSWI has used stock in acquisitions before, leading to the share count getting diluted. Overall, the share count is relatively flat since the company’s inception.

To conclude, CSW Industrials scores a 16/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below.

Q3 2024 Earnings Review

CSWI recently reported Q3 2024 earnings. See its year-to-date results below. I also attached Carrier’s recently reported HVAC results.

We can see how despite the North America resi HVAC struggles, CSWI continues to grow nicely.

Disclosure:

I do not own CSWI stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.