CoStar Group (CSGP)

CoStar Group CSGP 0.00%↑ sells commercial real estate information software built on its proprietary data set and operates multiple real estate websites.

Quality (4/5)

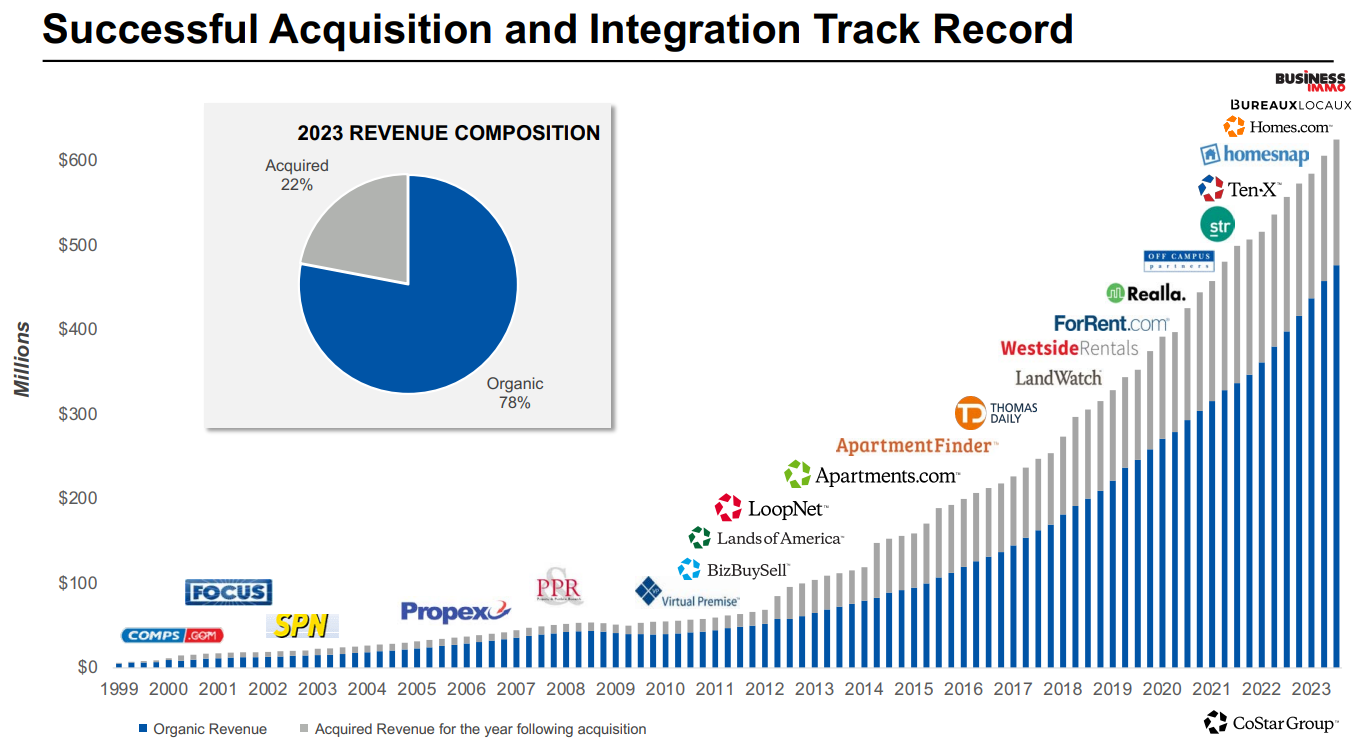

CoStar’s revenue is on pace to be $2.5B in 2023 compared to only $441M ten years ago. The nearly 20% CAGR is a bit high for my liking because it is usually difficult for companies to sustain this level of growth for a long time. While growth rates recently dropped to 12%, CoStar is adding more dollars of revenue year-on-year than it had in total as a company before 2011 (~$200M).

As seen in the Koyfin historical chart, CoStar has an impressive track record for growth, with only one period of decline in the last twenty years. CoStar is on 50 straight quarters of double-digit sales growth despite the ups and downs of commercial real estate.

CoStar gets 97% of its revenue in North America. CoStar used to list its clients in its 10-Ks where we could see customers including CBRE, JLL, Re/Max, Bank of America, JP Morgan Chase, BlackRock, KPMG, 7-Eleven, City of Chicago, Duke Realty, Comcast, Verizon, and many more. Given its high renewal rates over the years, I would imagine most of these companies are still clients today. So, it is a diverse client base, and no single customer makes up over 2% of revenue.

CoStar does not pay a dividend, and it has over $5B of cash on its balance sheet earning about 5% interest. Its use of leverage has always been low, around 1.2X (total assets / total equity).

Visibility (4/5)

A few years ago, I think the Visibility category would have scored a 5/5. With subscriptions accounting for 95% of revenue and >90% renewal rates, CoStar has a fantastic recurring revenue stream. Forecasting was reasonable as 80% of revenue came from annual contracts.

However, today, the real estate market has changed dramatically since the pandemic, and CoStar decided to strongly pursue residential real estate, reducing visibility. Commercial real estate is adjusting to a new mix of employees working at home or on hybrid schedules, changing the office space needs for many tenants.

Then, with CoStar’s residential push, it has been very difficult forecasting expenses each year. For a few quarters, CoStar’s spending on residential was much higher than expected, then for a few quarters it was lower, and now it is back to being higher again. The constant changing of expectations resulted in many aggressive up and down moves in CoStar’s stock. Overall, it ended with the stock going nowhere for the last four years.

After reaching management’s 40% EBITDA margin target exiting 2018, the latest quarter saw margins hit 14%. Yikes!

I have a public Tableau dashboard that tracks CoStar’s quarterly metrics.

On the plus side, CoStar’s diverse set of businesses help reduce cyclicality. For example, when the market slows and clients lose tenants, they are willing to spend to replace the vacancy.

Downturns are good too because we bought some amazing companies in the downturn. And we are not terribly cyclical as a company. We typically are able to grow through downturns. And there is actually both a cyclical advantage to strengthen the apartment industry for us. As people are building a lot of new developments, they are ready to invest in getting faster lease up on those new buildings. Conversely when the wheels come off and vacancy rates drop what they spend on, lead generation with Apartments.com is peanuts or any other call for term you want to use compared to the amount of money at risk in these communities. So when someone's spending $1,100, $1,200 a month on getting the majority of their leads to keep their $250 million property leased and solvent they don't cut back on that $1,100 a month. So, I think that's one of the nice things about our business is we are pretty -- we benefit in the up cycle and we're very resilient on the down cycle” (CSGP: 2019 Earnings call Q1 2019 Transcript, 2019-4-24)

Lastly, in Visibility, CoStar has heavy use of non-GAAP adjustments with NG/GAAP earnings around 2X. Stock-based compensation is the largest adjustment.

Management (4/5)

Andy Florance is the founder, CEO, and president of CoStar. The Chairman of the Board since the company’s founding in 1987 is Michael Klein, a lawyer who helped Andy early on and was an original investor in his company. It is nice to see the CEO and Chairman roles independent of each other. Scott Wheeler has been CFO since 2016, previously working at Experian.

Over the last decade, management generated $2.7B of free cash flow (FCF) cumulatively, while spending $2.3B on acquisitions. I calculate a median return on invested capital (ROIC) of 14% over this time.

Stock-based compensation is about 4% of total revenue. Shares outstanding have increased greatly over time due to dilution and stock splits. There are over 408M shares outstanding today compared to ~200M a decade ago. Insiders own 1.6% of shares out, according to the latest proxy. Andy and Michael own 4.5M shares combined.

Management’s incentives include EBITDA, revenue, net income, and stock price. I would prefer to see metrics like free cash flow or ROIC.

Andy’s total compensation in 2022 was $19.4M. We will see how much he made in 2023 despite the company’s stock being flat now for so long. Andy ran up a $267,387 bill in 2022 using the company’s aircraft for personal use.

Demand Creation (5/5)

I think CoStar is one of the best demand creation companies of any company out there. It has a near monopoly on mission-critical commercial real estate data software.

CoStar has a 30+ year history collecting and updating real estate data, making it almost impossible for a competitor to try to catch up and match. CoStar uses thousands of drones, hundreds of cars, an airplane, analysts, researchers, software developers, and more to acquire its information and build its products.

At one point, a company called Xceligent attempted to compete with CoStar by stealing CoStar’s copyrighted content. Xceligent invested millions for 20 years, never turned a profit, got sued by CoStar, and eventually went bankrupt. After the bankruptcy, CoStar raised its monthly price for new brokers, showing tremendous pricing power. Customer do not want to switch data providers at risk of missing out on attractive real estate deals.

In its Marketplaces, CoStar has excellent, intuitive domain names and search engine optimization (SEO) with Apartments.com and Homes.com. Its advertising campaigns have been successful, especially using Jeff Goldblum as the spokesperson for Apartments. It looks like management is going to use the same playbook for Homes.com. During the Super Bowl last weekend, Homes.com had an ad using Lil Wayne and a helicopter flying up to a high-rise, similar to the Apartments.com Super Bowl ad many years ago.

Valuation & Pricing (2/5)

Attached below is my DCF analysis-

I set revenue to grow in the high-teens with EBIT margins eventually improving as Residential spend should hopefully normalize over time. We have seen other data provider peers generate 30%+ EBIT margins, so I might be too conservative with my estimate. Reinvestment is high over the next couple of years for Homes.com growth.

My estimated value/share comes out to $51 vs. today’s price of $83. Setting revenue to grow 20%+ and EBIT margins at 35-40% would result in an $83 estimated value.

For pricing, I think the stock looks reasonable. As I mentioned above, CSGP stock has been flat for four years now. I know the first thing most investors think when they look at CSGP’s stock: “the P/E ratio is too high!!” Despite having a 20-year mean P/E of 60X and returning 2,000% during that time, it has been “so obvious” the last four years that CSGP would do nothing because of its high P/E ratio.

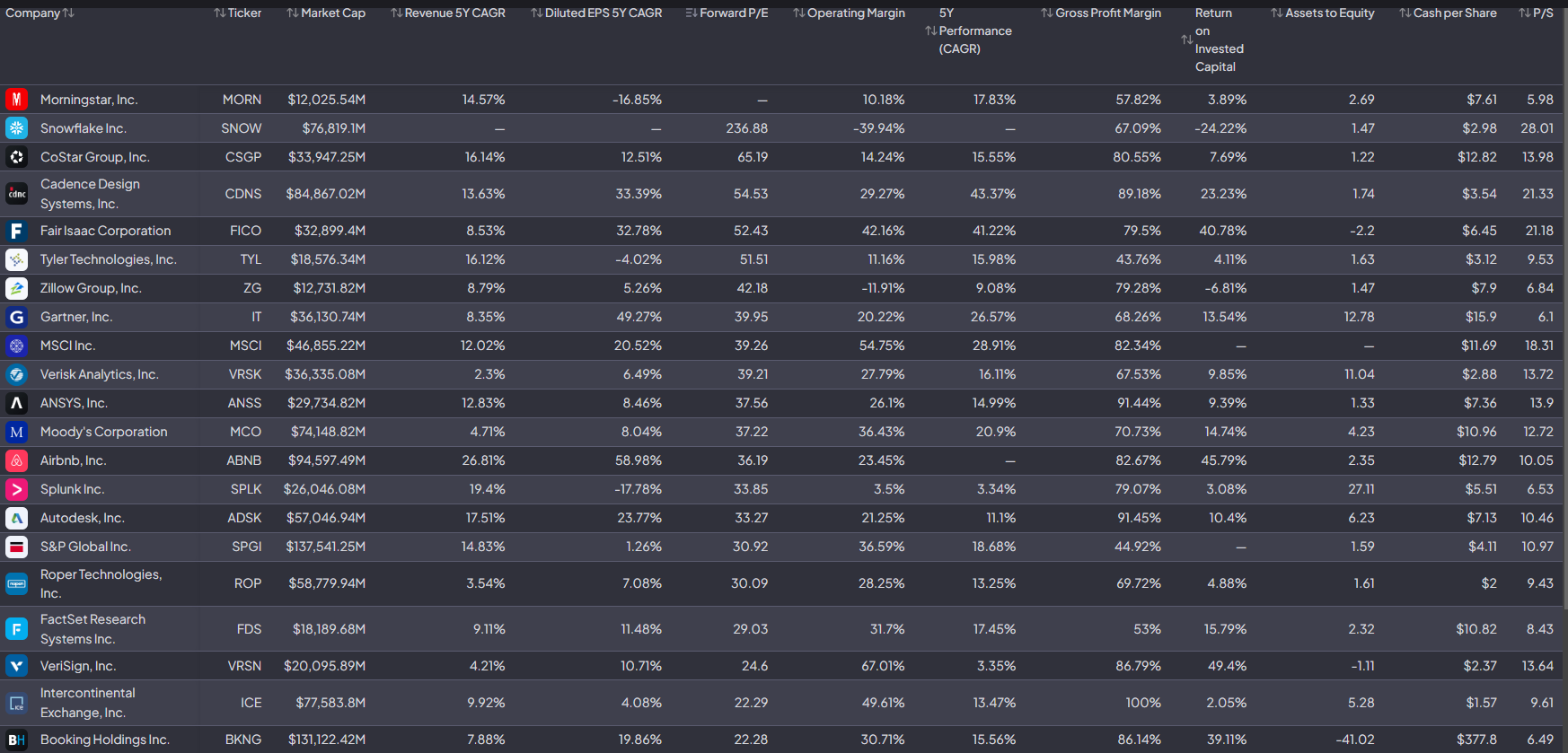

CSGP has one of the highest P/E multiples of all US stocks, according to Koyfin’s percentile rankings. Relative to itself, CSGP is not off-the-charts expensive like most stocks I have looked at on this blog so far.

Compared to my peer group, only Snowflake has a higher P/E right now. I think CoStar is a lot like Tyler Technologies where there is a very long duration of growth possible and a 60X P/E today could look like nothing in 10-15 years.

To be safe, I am going with the 20-year mean P/E of 60X on $1.40 of earnings potentially in the next 12-18 months. This leaves me with a price of $84.

Combining my valuation and pricing, a buy-below price target of $68 looks fair. I already own CSGP stock, but it is only a 2.5% position in my portfolio. I would consider adding more if it got below my target buy price. I bought at $83 and $60 in the past.

Risks

What could possibly go wrong with CoStar? The Residential investment could turn out to be a bust. However, CoStar’s track record would say otherwise. Apartments.com, for example, started with $86M of revenue when acquired, growing 11X to $940M today.

“So we've done this a number of times. This is if you use the analogy of building a building and you're building out first year, you're acquiring the land, design the property second year, you're getting the permits, bidding out the work, third year you're building out, if you're leasing it up. We've built a number of buildings just like this before.” (CSGP: 2023 Earnings call Q4 2022 Transcript, 2023-2-21)

"Entering the apartment marketplace business though clear to us, we're not universally popular at the time when we were in the investment phase they required. We pursue growth investments regardless because we are singularly focused on the enormous value creation we see in meeting the demand for digital information, analytics and marketing of the $300 trillion real estate asset class globally. Digitizing real estate is unlocking major value, and we are absolutely in the earliest innings of this opportunity. I believe that CoStar's group's revenue will grow tenfold again over the next 12 years because of the careful significant calculated investments we're making that optimize our competitive advantages and capabilities. We firmly believe that Homes.com can compete and win in the residential opportunity." - Andy Oct 2023

The building analogy is nice, but what if you build the building in the wrong place? Management thinks this is the right place, which seems like that is becoming more and more true. I was listening to an Odd Lots podcast about a lawsuit related to real estate brokers fixing their own commissions. This seems like it could be a benefit to CoStar’s model.

One argument has been that Zillow and Redfin are lousy businesses, so CoStar is wasting millions of dollars to enter a money-losing market. Andy, himself, noted in the past, “unlike the residential resale market, which involves personal consumption…” and “…the highly competitive and contentious online residential resale space” when explaining why he bought Apartments.com and prefers multifamily to residential. However, as management shows in the chart above, the business model of marketing a property, instead of an agent, leads to significant profits over time.

We will see. So far, Homes.com is off to a good start, achieving 100M+ monthly unique visitors and 1M+ registered agents.

Other issues could arise from Founder & CEO Andy’s key-man risk. He is only 60 years old, so he potentially has many years ahead of him. But, you never know, especially when you see Jeff Bezos, who went to college with Andy, step down in 2021. What would happen to the vision and growth of CoStar without Andy? I am not so sure.

The other part of this risk has been Andy’s aggressive management style, notably since the pandemic. He is obviously biased towards preaching the positives of commercial real estate, so he hates work-from-home or hybrid arrangements. This seemed to dampen employee morale, leading to disgruntled employees making fun of Andy on the internet. There were some real issues this caused with employee turnover and underperforming salespeople.

“While the LoopNet marketplace remains strong and competitively advantaged, LoopNet's sales growth should have been stronger in the second quarter. We believe the lower sales resulted from a combination of factors and that most of these factors are correctable. These factors include a growing and relatively young sales team a training program, which has room for improvement, a large number of account transitions and a poorly conceived commission plan that drove lower activity levels and a weak customer service, which reduced our renewal rates. Does that sound like a CEO that's not happy with something?” (CSGP: 2023 Earnings call Q2 2023 Transcript, 2023-7-25)

Andy’s sarcasm and cockiness could put off some investors. He has always been like that, though. It bothers me a bit when he laughs and jokes around while he is not delivering results at the same time, and then blames factors like work-from-home. In addition, CoStar is doing a $460M expansion to its offices in Richmond. It is possible there is too much on Andy’s plate and he is using jokes to brush it off, which makes me slightly concerned about CoStar being distracted from its steady, high-margin core business.

Note: CoStar reports Q4 FY23 earnings on February 20th.

To conclude, CoStar Group scores a 19/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below.

Disclosure:

I own CSGP stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.

Great read! I'm following them for the last 3-4 months. They seem to have a big advantage in their field. Looking forward to the earnings next week!