Carrier (CARR)

Carrier CARR 0.00%↑ sells air conditioners, heating systems, and heat pumps in over 160 countries.

Willis Carrier was the American engineer who invented the electrical air conditioner in 1902 and founded Carrier in 1915. Air conditioning was quickly accepted by people seeking better working conditions and more comfortable living in their homes. Carrier innovated with large central air equipment for multistory buildings, compact units for individual homes, and refrigeration for transporting food. United Technologies acquired Carrier in 1979 and spun Carrier off in 2020.

Quality (3/5)

There is limited history for Carrier as a standalone company since it was spun off so recently, but so far it has a 5-YR revenue CAGR of 3% and double-digit dividend growth.

Most of Carrier’s stock price outperformance came within a year or two of the spin-off. The stock was undervalued and mispriced due to it being the beginning of the pandemic and Carrier’s large debt load that it took from UTX. Since then, Carrier has performed similar to the market but with larger drawdowns.

With revenue declines in 2020 (pandemic) and 2022 (North America residential destocking), it appears Carrier is a cyclical business that could potentially grow topline slightly higher than GDP through the cycle. Carrier is a global business with 58% of sales in the Americas and the rest split between Asia Pacific and EMEA.

Carrier has relatively high financial leverage at 3.7X (total assets / total equity). It reduced net debt significantly after the spin-off, reaching $5B in 2022, down from $10B in April 2020. Carrier then issued $5.6B of debt for the Viessmann acquisition, but expects to receive $5.5B of net proceeds from its three major divestitures. There are a lot of moving parts, however, management is targeting a 2X leverage ratio when the portfolio transformation settles.

Visibility (3/5)

Carrier’s focus on Aftermarket sales helps reduce its reliance on one-time product sales and cyclical end market exposure. Aftermarket sales make up a quarter of total sales and are growing at a HSD-LDD pace.

Carrier's growing Digital business is led by the Abound (optimizes building performance) and Lynx (real-time visibility into the cold chain) cloud-based platforms. While these are not large revenue producers today, it gives Carrier upfront recurring revenue, aftermarket revenue, and better customer loyalty.

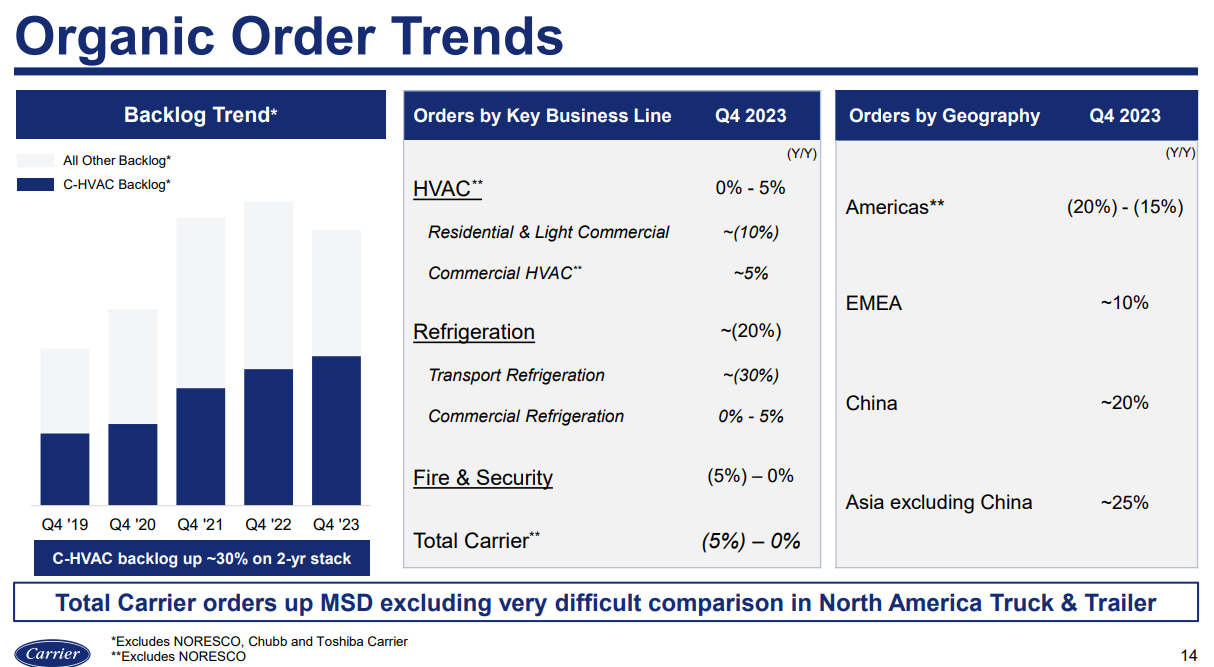

Residential and light-commercial sales are shorter-cycle and more difficult to forecast. As of Q4 2023, those orders were down 10%. Commercial HVAC (C-HVAC) is longer-cycle and typically more predictable. C-HVAC orders were up 5%. We can see management highlighted C-HVAC steady order trend in the slide below compared to the other, more volatile segments.

Is Carrier simple, boring, and understandable? While HVAC systems can be complex, the idea of wanting clean, comfortable indoor air is understandable and a trend that should last at least another 100 years. The near-term is not simple or boring for Carrier as it goes through its portfolio transformation.

Just in the last two years, Carrier acquired Viessmann (for $12B), Toshiba Carrier, Giwee, Nlyte, BrokerBay, and Cavius, while divesting Chubb, the security business (to Honeywell for $5B), the commercial refrigeration business (to Haier for $0.8B), the industrial fire business (to Sentinel Capital for $1.4B), its stake in Beijer, and12 JVs.

“We announced the exit of about $4 billion of our existing revenues, Fire & Security business, Commercial Refrigeration businesses, all good businesses, well positioned in their space, but we no longer believe we're the best owner of these businesses. The outcome of that is a company that is more focused on HVAC, climate, electrification, energy transition. It's a company that is simpler to run, simpler to understand, much fewer competing priorities and, frankly, a company that has a higher growth profile as well. And as we'll talk about within the middle of that transition, as we talked about now, we've actually made attractive progress so far.” (CARR: 2024 BofA Securities Global Industrials Conference 2024 Transcript, 2024-3-21)

Visibility should improve once Carrier completes this transformation and becomes a pure-play HVAC company.

Management (3/5)

Carrier’s management team is led by Chairman and CEO David Gitlin, who joined UTX in 1997. Gitlin was the President & COO of Collins Aerospace Systems from 2018-2019 and the President of UTC Aerospace Systems prior to that. So, before the UTX spin-off and the Carrier transformation, he was involved with the $30B Rockwell Collins acquisition at UTX. He has had a lot on his plate the last seven years. Gitlin’s aftermarket aerospace experience provides a unique background for Carrier’s goal to increase aftermarket mix, whereas previously the company was focused on one-time product sales.

Management is incentivized by sales, adjusted operating profit, and free cash flow (FCF). Since the spin-off, Carrier has a strong $6.8B of cumulative FCF. I calculate return on invested capital (ROIC) in the LDD, around 10-11%. ROIC is only just above the cost of capital and is the lowest in the proxy’s peer group. It would be nice to see management incentivize a higher ROIC in the future.

Stock-based compensation is less than 1% of total sales. Carrier started buying back shares after it reduced its net debt, however, it issued about 60M shares to the Viessmann family as part of the acquisition. Management expects to buy back an equivalent amount of shares in the future once leverage is lower again.

Insiders own less than 1% of shares outstanding, according to the latest proxy. It would be preferable to see higher insider ownership.

Demand Creation (3/5)

I believe Carrier has little-to-no demand creation ability and is more dependent on new construction, replacement cycles, or regulatory changes. On the plus side, Carrier is a trusted HVAC brand with over 100 years of providing (for the most part) reliable, high-performance, and energy efficient products. This has led to a massive installed-base of Carrier systems that require service and replacement. Management noted in the past that Carrier had 330K commercial HVAC systems, 2M light commercial HVAC and 33M residential HVAC units in the field. The switching costs are high, especially for the larger HVAC units. It would be extremely disruptive and expensive to switch out an entire HVAC system for a competitor brand. In addition, HVAC systems are mission critical and will be fixed or replaced as soon as possible if they break down.

On the flip side, for smaller systems, it would be less prohibitive to switch to a another brand and likely more competitive on price. Looking at HVAC forums online, there does not appear to be an overall go-to brand. Some say Carrier has the best performance, while others say Rheem has the quietest units, or Lennox has the best prices. I see certain Carrier products have had poor evaporator coils, while Lennox has had to do recalls over leaking issues. The most important factor cited is not the brand itself but the servicer who does the installation properly. Overall, this seems less compelling to me than AAON, which we looked at earlier, that is able to sell customized units for premium prices.

Carrier’s management makes the macroeconomic case that climate change, energy efficiency, electrification, and more will push demand higher. They believe Carrier can get above-market, 6-8% organic revenue growth (aftermarket growth, higher-priced, more-efficient HVAC units) and 50 bps of margin expansion per year, leading to double-digit adjusted EPS growth through the cycle.

Valuation & Pricing (3/5)

Attached below is my discounted cash flow (DCF) analysis of Carrier:

It was a bit challenging to make estimates given the portfolio transformation. I set revenue to grow 9% the next two years before dropping to 7.5%. EBIT margin increases over time to 15% given higher aftermarket sales mix, which carries higher margins. I used 898M for the share count but management says it could be >900M in 2024. My estimated value per share is $41 compared to today’s price of $58. Carrier does not appear to be as great of a value today as it was at the spin-off date.

For pricing, Carrier’s stock has limited trading history, but so far, it is mostly tracking a market multiple. Carrier has a F12M P/E of 20X today and a mean of 19X.

Compared to peers, Carrier’s P/E is right below the median of 21X, but it has well-below-median EBIT margins and ROIC, with much higher debt. It might be challenging for Carrier to get a higher multiple in the next 12-18 months as it goes through the portfolio transformation and pays down debt. I could see an above-median multiple in 2-3 years as Carrier has less leverage and is more of a pure-play company. For now, though, I am going with a 21X multiple on $3.10 of EPS, for a pricing of $65.

Combining my valuation and pricing, I get a target buy-below price of $53, which is 9% lower than today’s price. I currently have a 3.5% position in Carrier. While the stock is not overly expensive, the company fails to score highly in my criteria, which puts it on the sell or swap-out list for me, especially if the stock gets more expensive in the near-term. I also would not be against keeping a smaller position, maybe 1-2%, because I could see Carrier being a higher-multiple, higher-Mark score stock in a few years.

Risks

What could possibly go wrong? My top risk is the portfolio transformation complexities that could lead to distractions and/or disruptions for the business and management team. It may come in the form of product delays or “synergies” that reduce product quality or ERP system disruptions (Carrier has 50 ERP systems). This seems like a capable management team, but it would be preferable to see a finished transformation with a focused, pure-play Carrier as the result.

In addition, with acquisitions, Carrier paid a large price of $12B for Viessmann and needs to deliver on its outlook. Viessmann will likely be heavily scrutinized my investors over the next few quarters to make sure it is hitting its targets. It already appears like there is a slowdown of orders in Europe (somewhat due to new legislation in Germany and other countries).

“That being said, of course, they're not immune to what's happening in the market. What we have said for Viessmann for this year, which is embedded in our guide for -- that we provided in February is mid-single-digits revenue growth overall for Viessmann for the full year, first half flattish to slightly down. And we are expecting a pickup in orders that we expect to see late this quarter into Q2 that would help us with better performance in the second half of the year, knowing, of course, that the comps get easier in the second half of the year. If I look at our performance in Q1 for Viessmann Climate Solutions, I expect our profitability to be pretty much in line with what we expected, even though the sales might be a little lighter.” (CARR: 2024 BofA Securities Global Industrials Conference 2024 Transcript, 2024-3-21)

Next, the commercial HVAC market worries me due to the expected collapse of office real estate from hybrid work arrangements. Less offices, less activity, less restaurants and shops around the offices, less population, and less spending would be bad news for HVAC providers. However, there will be more need for HVAC systems (cooling, specifically) for data center and technology markets. Maybe that could offset any decline in offices. In addition, it is worth noting that U.S. commercial real estate is only 10% of Carrier’s commercial business. Data centers and education are much higher portions of sales.

Continuing, I was previously worried about product litigation regarding PFAS and asbestos. There was an update last year on Kidde-Fenwal, which mainly had the PFAS issue:

“Kidde-Fenwal, Inc. (“KFI”) is a separate Delaware corporation with a 35-year history as an independent company. Carrier Global Corporation (the “Company”) inherited the stock of KFI in the Company’s 2020 spin-off from Raytheon Technologies (formerly known as United Technologies Corporation). KFI operates a range of industrial fire suppression and detection businesses with annual sales of more than $200 million in 2022. KFI may have contingent liabilities relating to the manufacture and sale by National Foam of Aqueous Film-Forming Foam (“AFFF”). KFI disputes these liabilities.”

According to Carrier’s 10-K, there were over 6,000 lawsuits filed against Carrier and Kidde-Fenwal. Management provided another update at its latest investor conference:

“Our expectation is that all the proceeds associated with that transaction will be used to satisfy any potential claims associated with AFFF. The Chapter 11 process is still, of course, ongoing, even though the sale is imminent. With remediation, then what we've said is we feel very strongly in the corporate veil that we have. And that if -- to the extent there are any liabilities, they reside within KFI.” (CARR: 2024 BofA Securities Global Industrials Conference 2024 Transcript, 2024-3-21)

This is something to continue to keep an eye on and hopefully avoid a scenario like 3M.

“What differentiates you from your peers is that all the activity was always contained within KFI. And it is a real difference between you and your peers.” (CARR: 2024 BofA Securities Global Industrials Conference 2024 Transcript, 2024-3-21)

Lastly, Carrier’s relatively high financial leverage is a concern. Carrier will be less likely to offset a slowdown due to its higher fixed cost base than other companies in my portfolio. I would prefer to see less leverage used at Carrier.

To conclude, Carrier scores a 15/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below.

Disclosure:

I own CARR stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.