AAON (AAON)

AAON (AAON)

Like Rollins last week, we are looking at another smaller, U.S.-based company today: AAON AAON 0.00%↑ . AAON makes semi-customized HVAC equipment.

AAON gets an 18/25 Mark Score.

Starting with a 4/5 in Quality

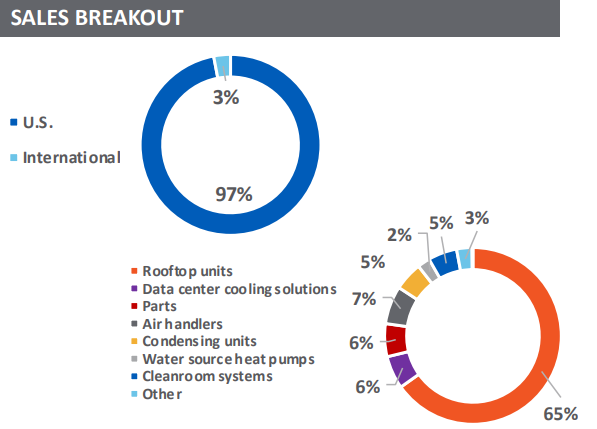

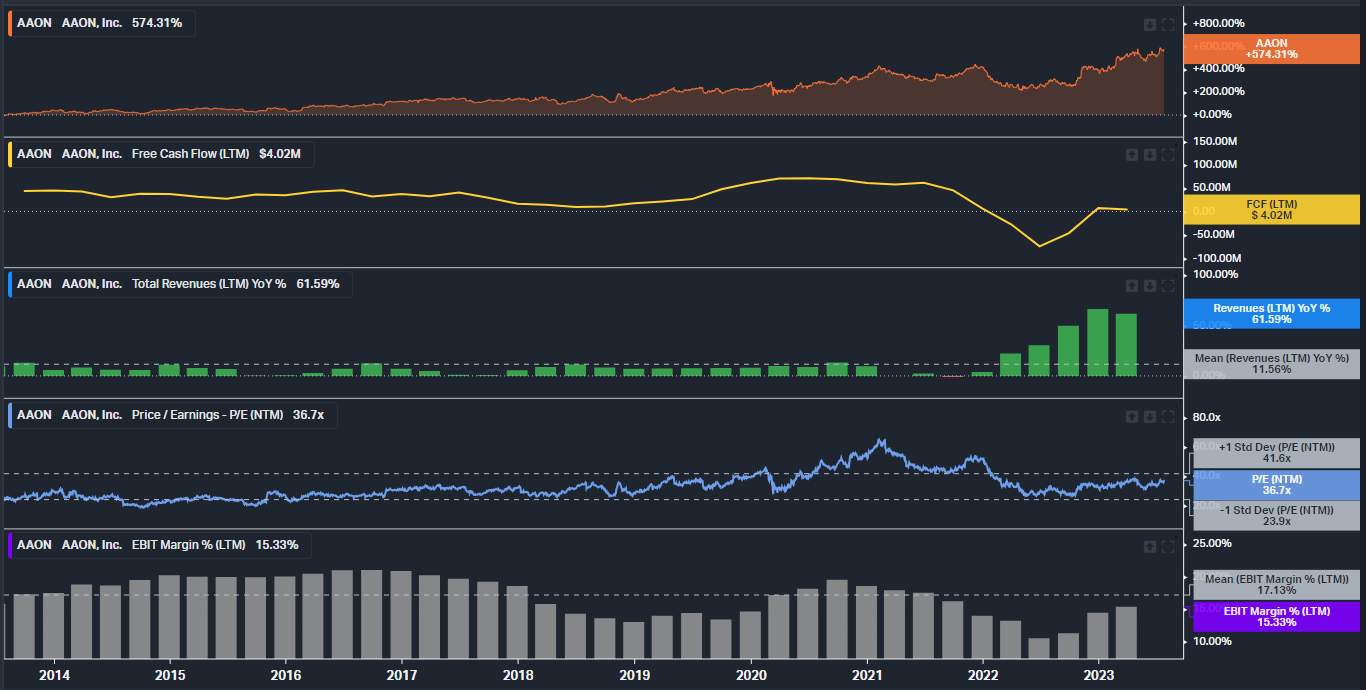

AAON has a strong track record for HSD to LDD growth, however, the recent 60%+ growth is unsustainable. I liked that 100% of revenue came from within the United States but the recent acquisition of BASX will add a low amount of international revenue. The balance sheet does not have a history of excessive leverage.

Visibility is also a 4/5.

AAON gets points for planned replacements making up about 65% of equipment sales, and very little use of non-GAAP accounting adjustments in the financial statements. The company loses a point because it is not exactly earnings certain. Overall, the trend is up and to the right, but due to the large peaks and troughs of the building materials industry, forecasting can be difficult.

Next, another 4/5, this time for Management.

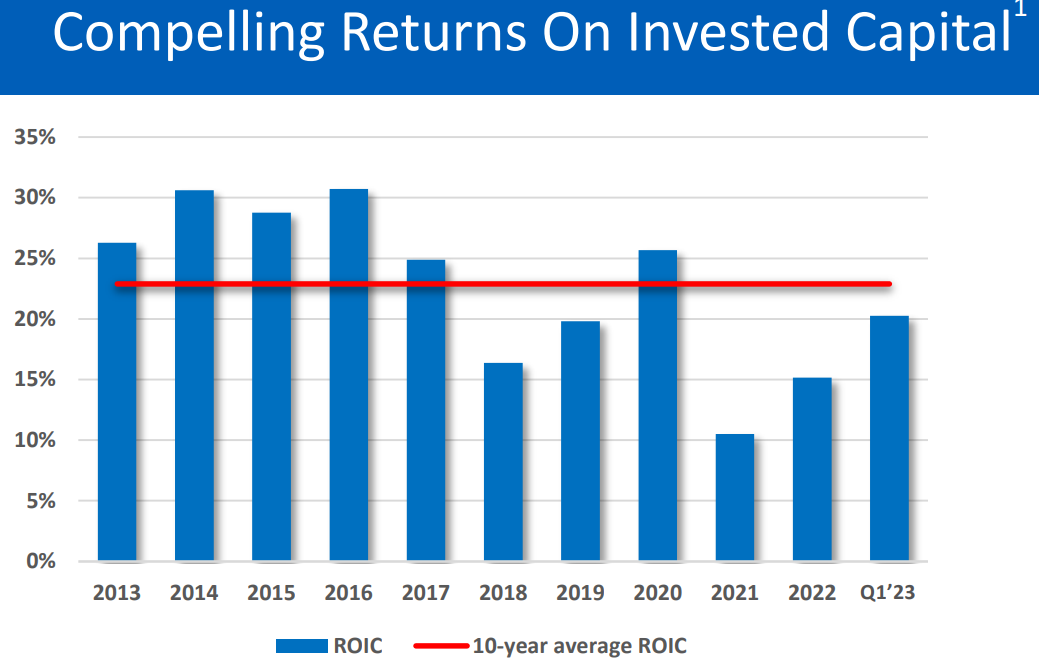

The point off is due to founder Norman Asbjornson stepping down, and AAON’s high, but declining ROIC. Norman was 85 years old, so it is not an indication for poor business performance. He still owns 18% of shares outstanding, according to the latest proxy filing. Gary Fields became the new CEO in 2020 after being President of AAON since 2016. While Gary has not been with AAON for a long time, he has over 35 years of experience in the HVAC industry. On ROIC, I like that management calls out the metric, including this chart in its slide deck:

It would be nice to see ROIC incentivized in the proxy, too. Right now, the incentive bonus is based 2/3rds on Operating Profit and the other third on Net Sales.

Demand Creation (4/5)

Before we look at valuation, let us look at AAON’s Demand Creation score. I give it a 4/5. Along with the inorganic growth from BASX, the 60%+ sales growth likely resulted in some demand pull forward for indoor air quality. This could make it difficult to create more demand in the near term as the pandemic ends and things get back to normal. In addition, in a potential recession, some projects that include AAON units would likely get cancelled. On the plus side, AAON offers custom solutions at a reasonable value, operating in a specialized niche that competitors like Carrier or Lennox are not focused on. AAON has successfully branded itself as the premium offering in the HVAC market.

Operationally, AAON’s experience and scale allows it manufacture its own parts and offer the best performing custom solutions for customers. Also, this operational expertise allowed it shorter lead times during recent periods of high demand. Imagine trying to order a cheaper Lennox rooftop unit for your project but Lennox says, “sorry, it might be 12 months before we have a unit available.” You would then call a channel rep for AAON, get quoted a higher price, but get your unit in a significantly shorter time. Not only have lead times been shorter, it can also make sense economically to pay for the premium HVAC unit. Building owners trying to save money up front on cheaper brands could see themselves having higher repair or replacement costs down the road.

Valuation & Pricing

We have determined that AAON is a solid business, so let us look at the current pricing and valuation of its stock. Below is my DCF analysis spreadsheet. Feel free to download it to review or update with your own assumptions.

I am giving AAON continued double-digit growth on top of the recent strong growth. Some of this growth is from the BASX acquisition. Revenue more than doubles to >$2B over the next ten years. I think EBIT margin stays in the high teens. My initial cost of capital is 9%. Unfortunately, if you want to buy a portion of this wonderful business, like I do, it appears to be overvalued. I get an estimated value per share of $55 compared to the current price of $102. My target price one year out is $60 per share. As with most of my valuations so far, I am probably being too conservative. On the pricing side, the current P/E ratio of 37X is reasonable compared to the historical multiple that AAON received. One standard deviation higher is 42X and one standard deviation lower is 24X. This P/E is on what seems to be peak growth, so I think a 25X P/E on potentially $3.00 of EPS would be fair. Between my $55 valuation and $75 pricing, I think a fair price to buy below would be $65 per share.

Risks

What could possibly go wrong? It seems like there are a few ingredients to set up future disappointment: a declining ROIC, the unsustainable growth rate, the founder/CEO retiring, and the company’s first major acquisition. Management notes that acquisitions are not going to be part of the strategy going forward. In terms of the risk of my valuation being too low, I could be underestimating growth. Management says backlog as of March 31, 2023 is up 706% since the end of 2020, with 657% of that growth being organic. That is over $600M of backlog that the company is going to work through. In addition, government regulation focusing on climate change and the environment could increase demand for AAON products more than I expect.

To wrap up, AAON (AAON) gets a Mark Score of 18/25. That puts it between Nordson (NDSN) and CPKC (CP) in the scores dashboard, now on Tableau!

Thank you for reading. Please share any thoughts or correct any errors you noticed.

Disclosure:

I do not own AAON stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.