Watsco (WSO)

Watsco WSO 0.00%↑ is the largest distribution network for heating and air conditioning (HVAC) products in the United States. See Watsco’s latest investor deck here.

Quality (4/5)

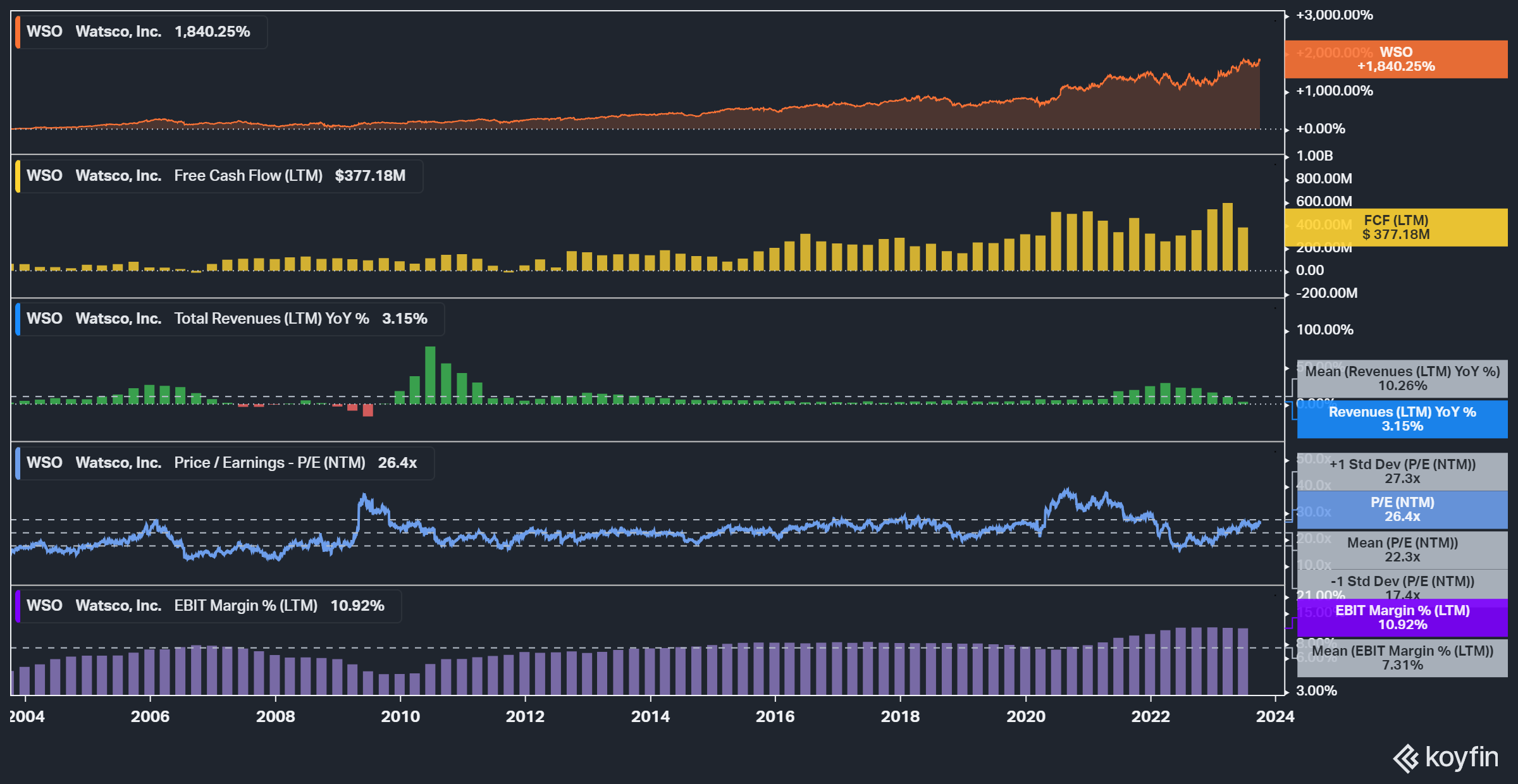

Long-term revenue growth appears sustainable in the high-single-digits to low-double-digits range. Growth comes from an equal mix of organic and acquisition-driven growth. The 20%+ growth after the pandemic is unlikely to sustain. Year-to-date in 2023, sales decreased 3% and EPS decreased 7% YoY.

Watsco has a strong track record for growth. During the last 20 years, the only time revenue declined was during the housing crisis of 2007-2009, in which Watsco’s sales declined low-single-digits and earnings declined between 10-30% YoY.

The United States accounts for 90% of total revenue. Leverage on the balance sheet is generally below 2.0X.

Visibility (5/5)

A predictable percentage of the growing HVAC installed-base breaks each year and needs replacing, giving Watsco a recurring revenue profile. Forecasting is reasonable because only about 15% of shipments are tied to residential new construction, which can be a difficult market to predict. Even if people cannot afford to replace their HVAC units, they will at least need repair. Since the pandemic, people seem to be upgrading their HVAC equipment even before it is broken or worn out because they want better indoor air quality. It is uncertain how long this trend will last. I find Watsco’s business model to be one of the most boring and understandable models of any company. There is some complexity involved with its three joint ventures with Carrier. These JVs give Watsco exclusive distribution rights for Carrier products in certain U.S. regions and are about 60% of revenue. Lastly, I like the lack of non-GAAP adjustments in its financial reporting.

Management (5/5)

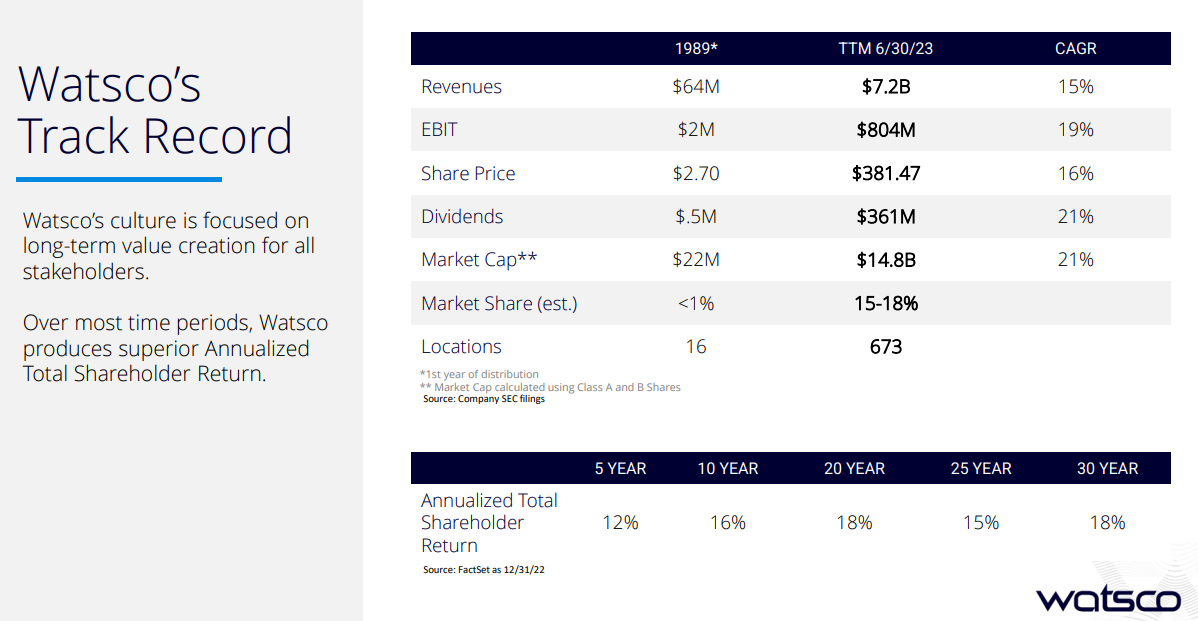

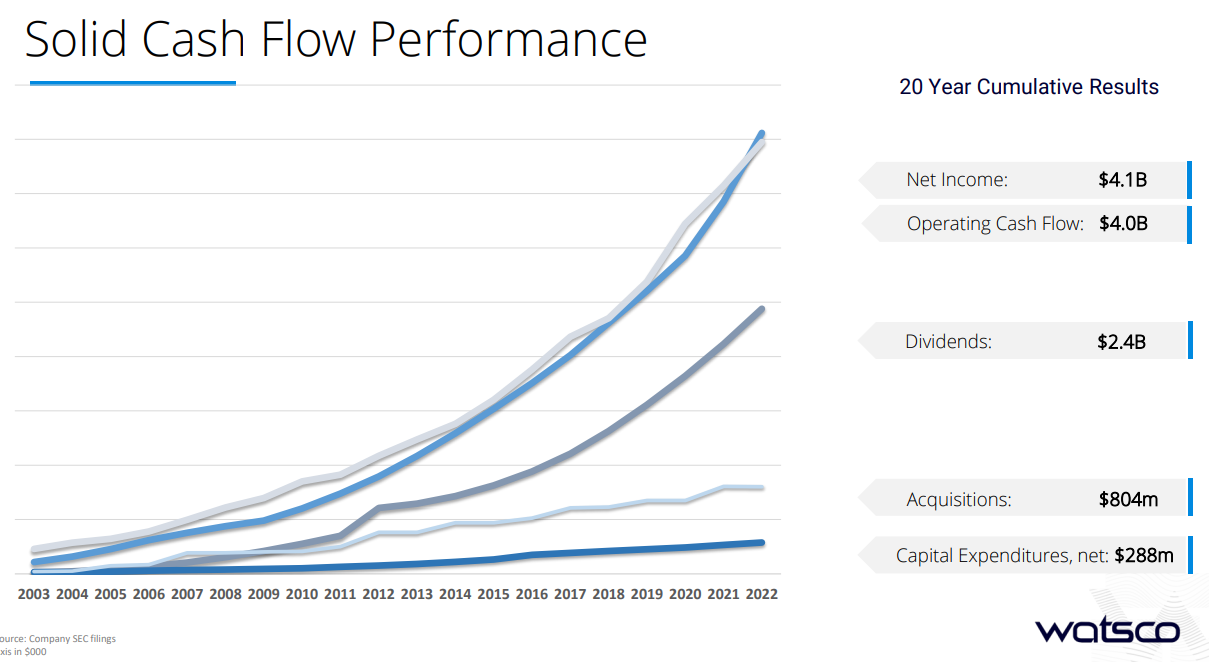

CEO Nahmad is 82 years old with 51 years spent at Watsco. He acquired the company from founder William Wagner. The President of Watsco is the CEO’s son. I calculate that management generated $3B of FCF cumulatively over the last decade, with business acquisitions of $0.4B. (Here is a link to my ROIC dashboard)

Management goes a step further, providing a 20-year cumulative results slide:

Watsco’s median ROIC over the last ten years is 20%, nicely above my estimated cost of capital. SBC is less than 1% of total revenue, and the Nahmad family owns >50% of the combined voting power through Class B stock.

Here is a good post on Watsco’s acquisitions and JV with Carrier:

Overall, Watsco has completed 68 acquisitions since 1989. The latest acquisition was Gateway Supply Company, which had $180M of sales across 16 locations.

In the latest proxy filing, listed incentives include: improvement of inventory turns, run-rate for e-commerce sales of 40%, sales growth of 15% for parts and supplies, operating income growth of 10%, gross margin growth of 2%, EPS growth, and common stock price growth.

Demand Creation (4/5)

Underlying demand comes from household formation and the increasing installed base, while near-term demand is linked to changes in weather and the housing market. Watsco boosts demand using its acquisition strategy, purchasing smaller competitors in its fragmented market. Watsco has 689 locations across North America, which is difficult for its competitors to match and beneficial to service contractors who need to find the right part quickly and locally.

Due to Watsco’s size and scale, it can acquire inventory at the best price with high volume purchases. If customers try to switch to a competitor, they could risk product availability.

In its quarterly earnings press release, Watsco lists multiple industry catalyst and trends, including regulatory changes, electrification of heating systems, growth of ductless HVAC systems, product & geographic diversity, and network investment & expansion.

Regulatory Changes. To address and stem the impacts of climate change, the federal government and various states have enacted laws and regulations to incentivize the replacement of aging HVAC systems in favor of more energy-efficient and environmentally friendly systems. New standards became effective January 1, 2023 that raise the minimum required efficiency for HVAC systems nationwide. New regulations are also in effect that mandate a phase down of existing refrigerants that contain high global warming properties used in older HVAC systems and a transition to new refrigerants beginning in 2025. The demand for higher-efficiency systems and heat pumps is also expected to benefit over time from the passage of the Inflation Reduction Act of 2022. - Watsco’s Second Quarter Earnings Press Release

Summaries of the other catalyst and trends can be found here in the press release.

Pricing & Valuation (2/5)

As seen in the Koyfin history chart at the top of this blog post, WSO’s P/E ratio tends to jump before periods of high growth. After both the housing crisis and pandemic, WSO’s P/E increased to almost 40X. As growth settled, the P/E ratio also settled to around 20-24X.

When compared to peers, WSO carries a premium multiple, which makes sense given its higher ROIC and lower debt. A 24X multiple on EPS approaching $15.00 leaves a price target of $360/share.

Below is my discounted cash flow analysis:

I model revenue growth of only 2% for the next two years due to the tough pandemic comparables. I set EBIT margin to expand to 12% vs. 11% today. This EBIT margin is above the historical mean of 8% but below management’s target of 15%. I might be too conservative here. We have seen other distributors, Fastenal, Grainger, and Pool, for example, get 15%+ EBIT margins. I put reinvestment to be lower in these upcoming lower growth years before increasing to a more normal reinvestment rate. ROIC is around 20-21%. My estimated value per share is $300. If I set the EBIT margin to management’s 15% target, I get an estimated value of $380/share, which happens to be the price that WSO is trading at today.

Combining my pricing and valuation, I get a target buy below price of $308/share, or 19% lower than today’s price of $380.

Risks

One of the biggest risks could be OEMs pushing to cut out the middleman, Watsco. Historically, this has not been successful, so I see this as a low probability. Carrier tried unsuccessfully decades ago. The other big risk comes from a potential slowing housing market. I am not an expert on the housing market, I prefer to read Calculated Risk’s analysis. From my understanding of his posts, it sounds like the housing market can slow without it becoming another crisis like 2007-2009.

To conclude, Watsco scores a 20/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below.

Disclosure:

I do not own WSO stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.

Enhorabuena por el análisis. Llevo $WSO (compradas a 275$) y estoy decidiendo si mantengo o no porque creo que están por encima del precio objetivo. Tu análisis me ha ayudado mucho. Gracias y un saludo desde España!