UnitedHealth Group (UNH)

UnitedHealth Group UNH 0.00%↑ provides health insurance and services to over 152 million people. Founded in 1974 as Charter Med in Minnetonka, Minnesota, UNH is one of the largest companies by revenue in the world today with $372 billion reported in 2023.

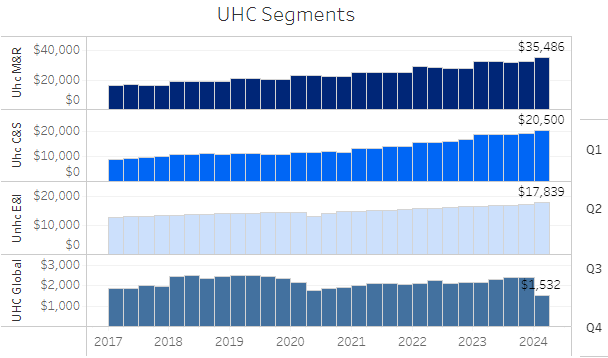

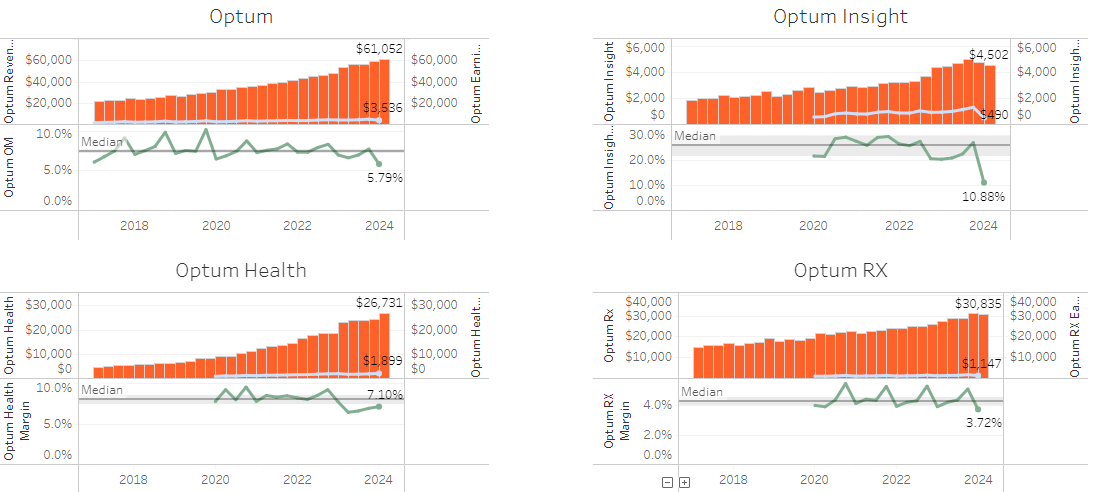

UnitedHealthcare segment includes insurance for Employees & Individuals (working-age), Medicare & Retirement (older adults), and Community & State (economically disadvantaged people), while Optum has Optum RX (pharmacy benefits manager, “PBM”), Optum Health (care delivery), and Optum Insight (analytics). See the latest investor deck for a deeper dive into each business.

Quality (5/5)

UnitedHealth Group (“UNH”) is a high quality company, with a 5-year revenue CAGR of 10% and a 10-year of 12%. Profits are split roughly half and half between its complimentary business segments, UnitedHealthcare and Optum. About 97% of sales come from the United States.

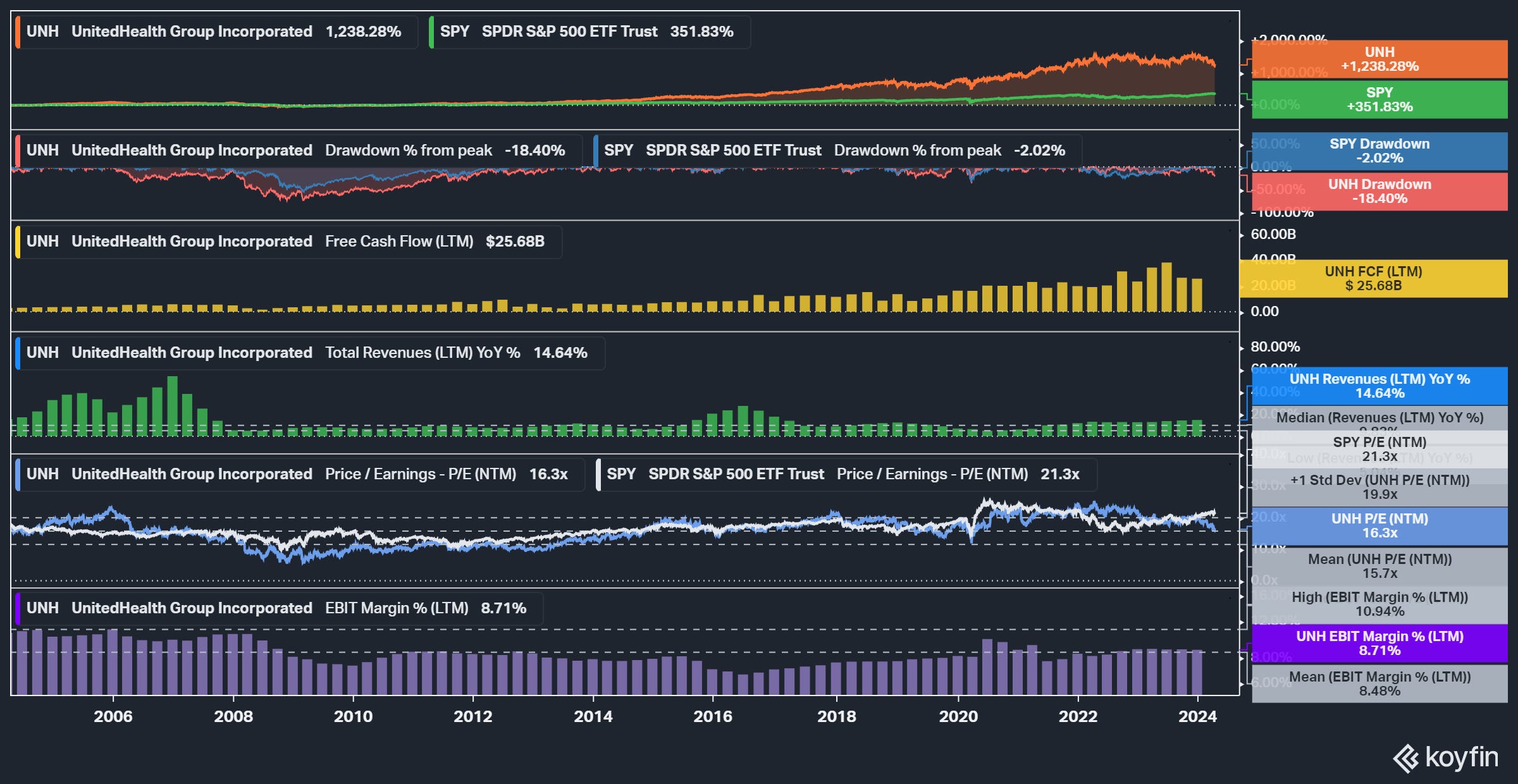

As shown in the Koyfin chart below, UNH has no revenue declines on a trailing twelve month basis over the last twenty years.

UNH is on 15 consecutives years of dividend increases, growing around 15% annualized. Shareholders, including Lee Cooperman, pushed UNH to pay a dividend fifteen years ago.

Financial leverage, measured as total assets over total equity, is at 2.8X today.

Visibility (3/5)

UNH collects recurring revenue through monthly premiums that typically rise every year. Along with Optum Insight’s growing backlog (currently $35 billion), these provide a solid foundation for forecasting revenue over time. Optum RX typically has multi-year contracts with retention rates over 90%.

There is more difficulty when it comes to trying to predict health care trends and the resulting costs & pricing. The U.S. health care market is very complex and constantly under political pressure. Medical costs have been rising, causing a headwind to profits. However, in Q1 2024, management said they have a much better handle on costs going forward. In addition, UNH has some self-inflicted issues regarding its Global business and its Change Healthcare acquisition.

I have a public Tableau dashboard for UNH where you can see recent quarterly trends.

The UHC segments are growing nicely, except for Global. The only segment that one can see a dip in revenue during the pandemic was in E&I. Global was a growth story in 2017-2018, but it never really materialized and management deemphasized it since then. Management just announced the sale of the Brazil subsidiary in Q1 2024.

Optum has similar steady growth in revenue for all segments. However, earnings have dipped recently in both Optum Insight and Health due to the cyberattack and acquisitions.

UNH typically uses minimal non-GAAP metrics, only adjusting out amortization of acquired intangibles, which is OK. However, in Q1 2024, UNH used substantial non-GAAP adjustments for the cyberattack on Change Healthcare and the loss on the sale of its Brazil subsidiary. GAAP earnings were -$1.53 per share and non-GAAP earnings were $6.91.

Management (5/5)

UNH is led by CEO Andrew Witty (since 2021) and CFO John Rex (since 2016). Witty was the CEO at Optum prior to becoming CEO of the whole company, and was CEO of GSK prior to that. Rex was the CFO at Optum prior to becoming CFO of the entire company, and was a managing director at JP Morgan prior to that (he used to be the one asking questions on earnings calls).

Over the last ten years, the company generated $154 billion in free cash flow (FCF) while spending $80 billion on acquisitions. Some of the larger acquisitions include, Brazil Amil (2012 - $4.9B), Catamaran RX (2015), Rally Health (2015), DaVita Medical (2019 - $4.3B), Equian (2019 - $3.2B), LHC Group (2022 - $5.4B), and Change (2022 - $8B). I found a great article on Substack showing UNH’s acquisition history.

I calculate a median return on invested capital (ROIC) of ~11% over the last decade, nicely above its cost of capital. Stock-based compensation is <1% of total revenue. Management spent $42 billion repurchasing stock cumulatively in the last ten years, reducing the share count from 986M to 938M today.

Insiders own 0.35% of shares outstanding, according to the latest proxy. Chairman and former-CEO (2006-2017) Stephen Hemsley owns half of those shares.

Demand Creation (4/5)

I believe UNH has some demand creation ability. Its superior integration of insurance and services leads to lower costs and more benefits, which leads to more customers, resulting in more acceptance by healthcare providers. It is a very positive cycle for UNH and is being copied by other companies in the industry. In 2018, CVS bought Aetna, while Cigna bought Express Scripts.

However, it may be difficult to create demand during an economic recession, especially with employee-based insurance. If unemployment rises, that would be less insurance demand from employers. Some states require healthcare coverage, or else there is a tax penalty. Otherwise, I suppose unemployed people could bypass healthcare coverage if they really wanted to.

The switching costs can be high for both providers and patients. Providers could potentially lose patients if they do not accept UnitedHealth, while patients could lose their preferred providers if they switch to a plan that is not accepted. Looking at the healthcare plan portal, there are definitely some cheaper options than UnitedHealth, but they do not offer the same bundled services or are not accepted by my doctor. It is almost like UnitedHealth is the Amazon Prime of health insurance.

Barriers to entry are high. The most recent example of this was Haven, a healthcare company founded by Amazon, Berkshire-Hathaway, and JP Morgan. Here is a brief article on Haven’s failure.

When Amazon, Berkshire Hathaway, and JPMorgan Chase joined forces in early 2018 to form a new venture, their goal was to use their U.S employee base of 1.2 million people, tech savvy, and wealth to transform U.S. health care. They failed for three main reasons: inadequate market power, the perverse incentives of the U.S. health care system, and the pandemic.

Even when three massive companies came together with deep pockets and over 1 million employees, they could not get providers to budge on prices.

Valuation & Pricing (5/5)

Attached below is my discounted cash flow (DCF) analysis. I did this before earnings on April 16th, so all numbers are based off the 2023 10-K. My estimated value would not likely change dramatically with Q1 numbers entered in.

I set revenue to grow 8-9% over the next few years. Q1 FY24 revenue was actually up 9%, so that looks to be in-line with what UNH can deliver. I gave UNH modest margin expansion, up to 10% from 9.1% today as Optum continues to grow. My estimated value is $584/share, about 31% higher than the price at the time of my valuation.

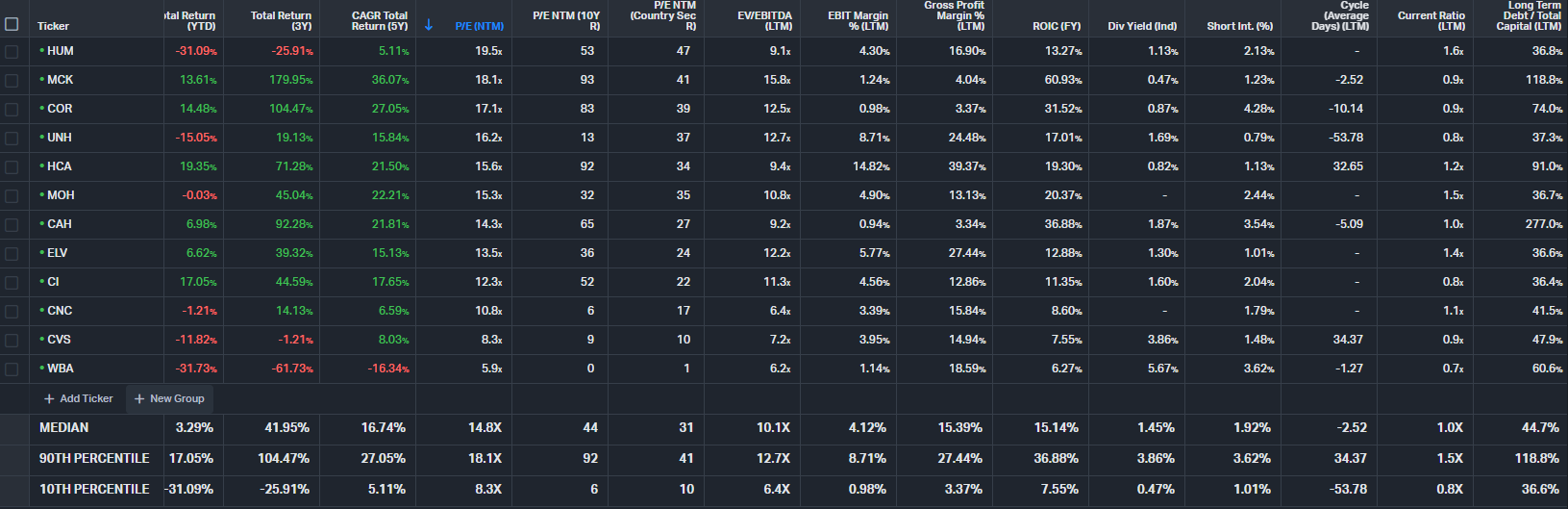

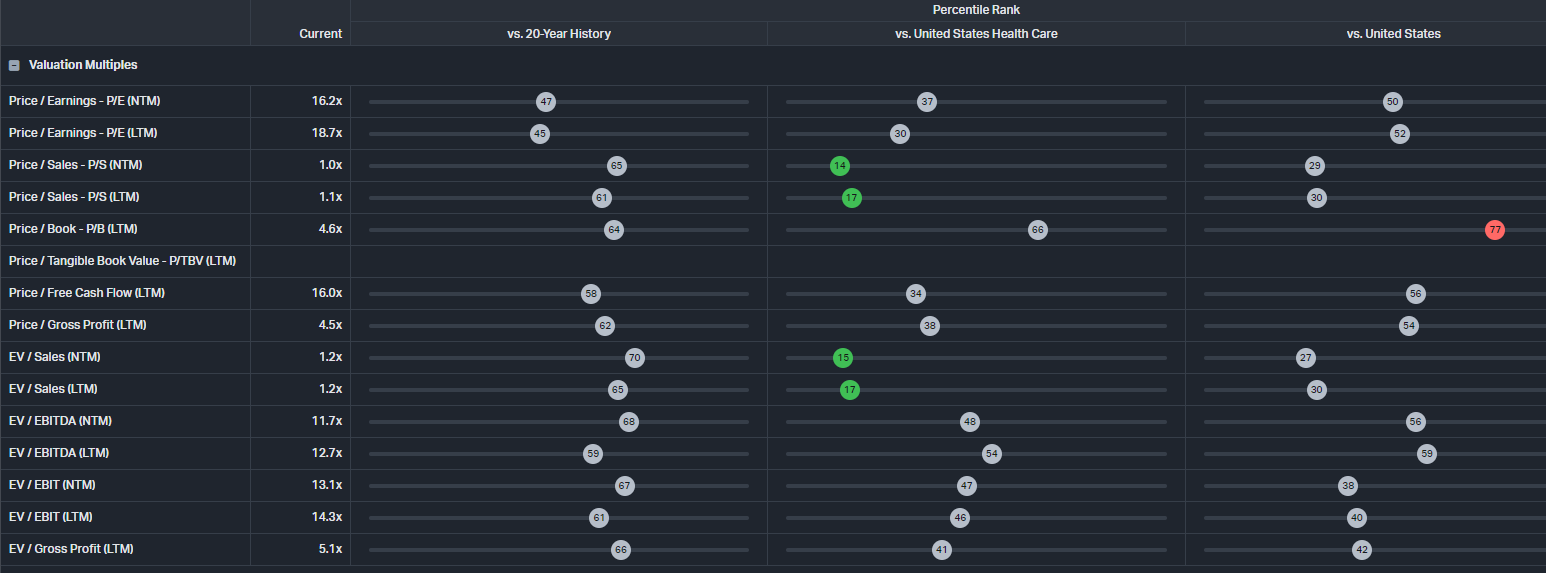

For pricing, compared to peers, UNH (16X) is just above the median P/E multiple (15X). However, it looks very cheap compared to itself on a 10-year and 20-year basis. In the peer chart, we can see UNH is in the 13th percentile (10-year) vs. the median of 44. Below, the 20-year chart shows UNH to be inexpensive relative to itself, the US healthcare industry, and the US as a whole.

Overall, UNH’s current pricing seems very inexpensive, especially given its high-quality growth profile.

Combining my valuation and pricing, I calculate a target buy-below price of $571, compared to $445 when I did my analysis. It looks like the stock will be 5-10% higher after Q1 FY24 earnings, but that would still result in solid upside. I have owned UNH for many years, but reduced my position size in 2022, so it is a smaller weight in my portfolio today. I am thinking about adding more in the coming weeks.

Risks

The top risk of owning UNH is the political pressure on the healthcare and PBM industries, especially in election years. In 2020, politicians debated a policy called Medicare for All, attempting to eliminate private insurance. Eliminating private health insurance would basically mean eliminating UNH, resulting in the stock probably being a $0. However, eliminating private health insurance seems like a 0% chance at this point. In addition, it would be preferable to have a health system that rewards preventing disease instead of profiting off treating it. This type of system could also impact UNH’s profits.

Next, UNH’s acquisition strategy could cause issues. The latest example was the Change Healthcare acquisition which led to a large cybersecurity breach. In Q1 FY24, the company reported $279M of disrupted revenue and $593M of direct response costs related to the cyberattack. Management expects $1.35-$1.6 billion in total cyberattack costs for the year. UNH had to loan over $6 billion out to healthcare providers to support them during the attack. It is not clear if the attack has been fully contained. This article claims another group is selling Change’s data on the dark web. We could also see customers of Change reduce reliance on Change in the future due to the disruption and loss of trust, leading to lower sales. UNH’s asset turnover has been in decline for the last decade, with a 1.3X ratio today vs. a median of 1.5X.

Finally, UNH’s large size could be a risk to future growth. It will be more difficult to find growth opportunities that can move the needle as revenue approached $400 billion annually.

To conclude, UnitedHealth Group scores a 22/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below.

A few extra Q1 2024 notes:

UNH lost a Medicaid contract in Florida

COO Dirk McMahon retired after 20 years

Share buybacks were $3B compared to $2B last year in Q1

There was not the usual boost to full-year EPS guidance in Q1. However, there was no change to FY24 EPS even when incorporating $0.30-0.40 of cyberattack impact. I guess that is technically a boost to full-year guidance.

Disclosure:

I own UNH stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.

Great post! I like the idea of creating a dashboard. I didn't know that was possible.