Roper Technologies (ROP)

Roper Technologies (ROP)

Here is another “technologies” company, following Tyler Technologies last week. Roper ROP 0.00%↑ describes itself as a business that “compounds cash flow by acquiring and growing niche, market-leading technology businesses”. For a more in-depth discussion of Roper’s business than what I am going to give here, see its investor day from earlier this year.

Roper gets a Mark Score of 19/25.

Starting with Quality, I rate this area a 4/5.

On the plus side, growth over time has been in the mid-single- to high-single-digits range. Management targets double-digit revenue growth with “MSD+” being organic. The rest comes from Roper’s acquisition strategy. About 85% of revenue comes from the United States. Leverage is around 2X.

Next, Visibility is a 4/5.

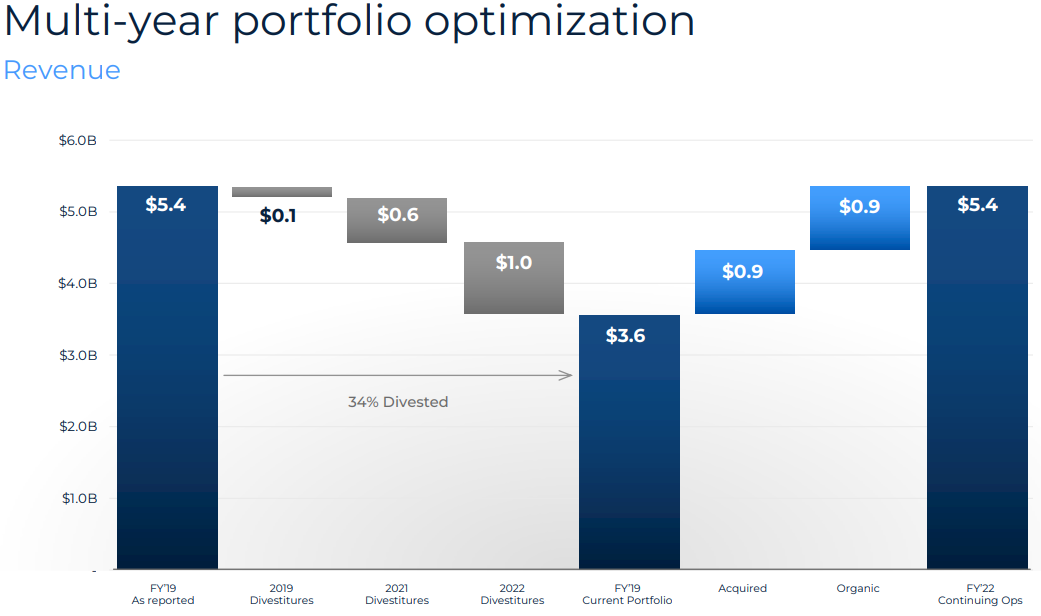

I like the increasing mix of recurring revenue, now in the 60-70% range of total. Roper has demonstrated high earnings certainty over time. Forecasting can be difficult due to the number of acquisitions and divestitures. The company has been undergoing a multi-year acquisition and divestiture spree, ridding itself of nearly $2B of revenue, while adding back about $2B of revenue.

Just recently in August, Roper announced it acquired Syntellis Performance Solutions for $1.25B, adding another $185M of revenue. Overall, Roper’s business seems understandable to me- software for law firms, insurance companies, etc. I take a point off for the use of non-GAAP information and buzzwords found throughout Roper’s reporting and presentations. You will notice they report “DEPS” instead of “EPS”, and use terms like “CRI” aka cash return on investment and “asset-light”.

Moving to the management section, I rate this a 4/5.

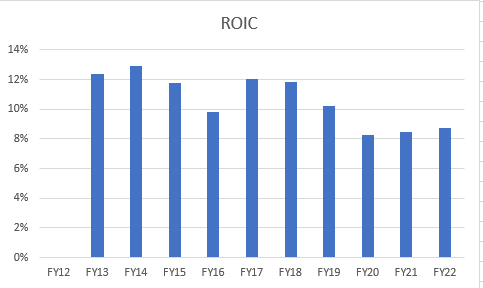

Management has historically been hugely successful operators, but the numbers and the story are not my favorite today. According to data from Stratosphere.io, ROP stock has a CAGR of 19% over 31.5 years, 14% over the last 10 years, and 8% over the last 3 years. A lot of the outperformance came in early years, while now, ROP stock is mostly tracking overall market returns. We have the red flags of a company renaming itself “technologies” from “industries” (in 2015) and we have declining asset turnover and ROIC. Here is my ROIC analysis for Roper:

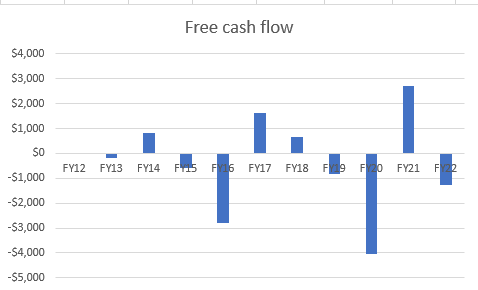

ROIC is declining and below 10% today, while FCF is cumulatively negative over the last ten years. I calculate about $12B of cash flow and nearly $23B spent on acquisitions. For how much management talks about compounding cash flow, I would have liked to see a better result here. Insider ownership is less than 1%, according to the latest proxy filing.

Demand Creation (5/5)

Roper does an excellent job creating demand by acquiring businesses in new niche, oligopolistic markets. Its individual businesses are typically market leading in their respective segments and have high switching costs. Take Aderant, for example, which is mission-critical software for law firms. While Roper may be known historically for selling pumps, Aderant is knowledgeable in legal markets. Attorneys put their very important time reports, billing statements, and calendars on this software. They definitely do not want to spend time switching to some other software and risk losing this information. There are more examples in Roper’s investor day if you are interested.

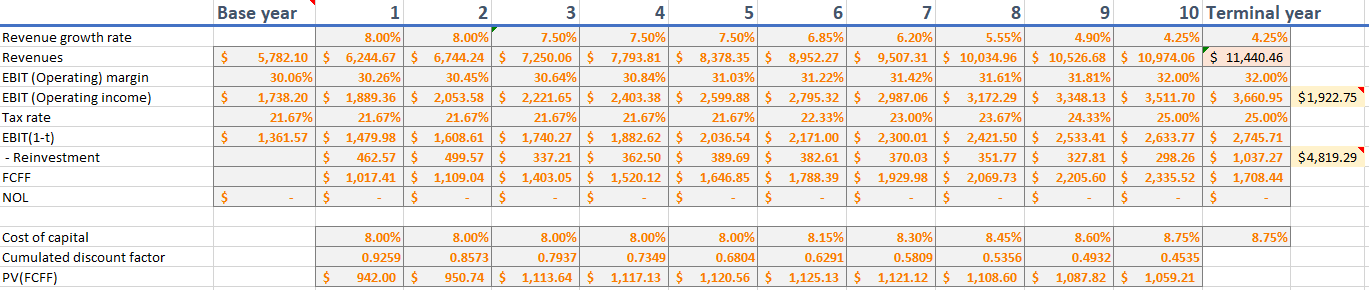

Since we determined that Roper is a good business, the last section of our analysis to cover is pricing/valuation. My DCF analysis yielded a current valuation of only $211/share vs. the current market price of $497.

As always, feel free to download my spreadsheet and make your own changes to match your story.

As mentioned before, I calculate ROIC as only 1 or 2 points higher than the cost of capital. My sales-to-capital ratio is low because Roper has to constantly make acquisitions to grow. In addition, Roper has nearly $7B of debt, leaving less value to equity owners. The dividend is almost an afterthought, yielding only 0.55%.

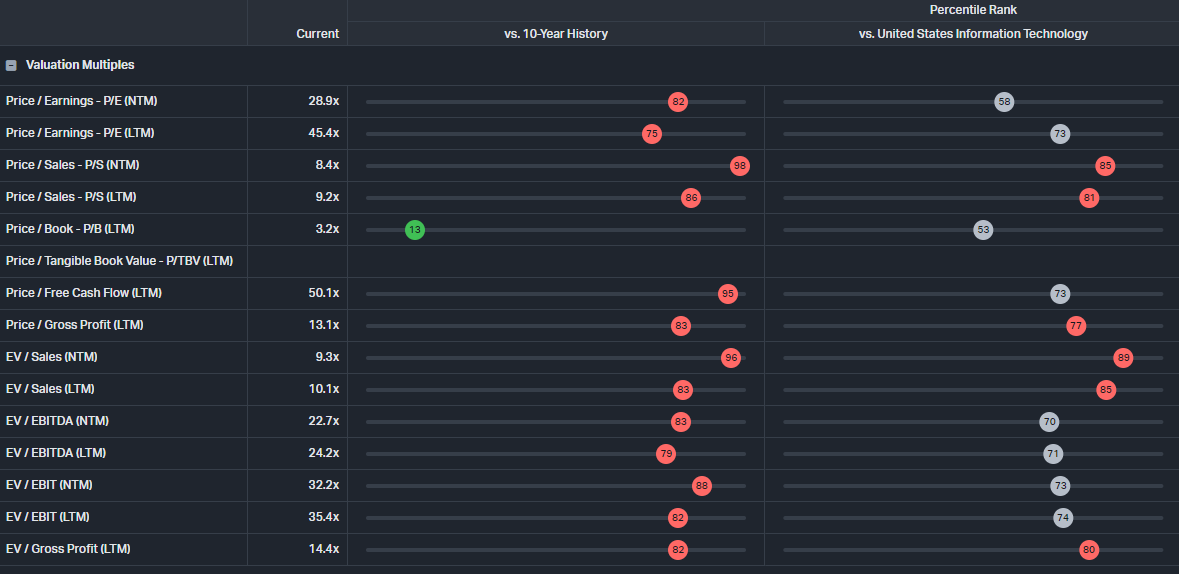

The pricing of the stock does not look much better:

Most pricing ratios are near the 90th percentile vs. the 10-year history. ROP looks slightly more attractive when compared to other technology peers, but still not a bargain by any means. If you only invest on P/E ratios, I think 26X on EPS approaching $20.00 looks fair, leaving a $520 price target. However, combining my valuation and pricing analysis, I am looking for a buy below price of $366, which is 25% lower than the current price. That seems low, but ROP stock was actually trading at that price briefly as recently as late 2022.

What could possibly go wrong? My main concern is the acquisition model. Declining asset turnover could lead to future write downs. The slim margin of ROIC over WACC leaves little room for error. Increasingly high multiples also heightens the chance of error. In addition, higher interest rates could be either good or bad for Roper. On one hand, they can probably get more deals done than private equity now (management recently noted having $4B of firepower for deals). On the other, management might not able to secure the super cheap debt that they got in the past.

At the Jefferies Software Conference in 2023, CEO Neil Hunn described the one thing most misunderstood about Roper. He said,

“I think misunderstood or maybe underappreciated by our newer software investors is the power of the compounding nature of our model. We're very much a risk-off model.

We have these clear leaders in these small markets that are wildly protected, but they grow nicely, not outrageously, but very solidly within a tight band of outcome. And then when you take all that free cash flow and have the freedom to deploy it to the very best use for us versus a suboptimal use across each one of the businesses individually. Then it gives you this year in, year out, very consistent low risk, mid-teens cash flow compounding, but it's a combination of the organic and inorganic piece.”

Hunn also described the difference between Roper and Constellation, one of fintwit’s favorite software companies:

“So we've certainly studied them. They've had great returns.

We have a lot of respect what Mark and his team have done. We're very different in the fact that there, we tend to do larger deals. They tend to do very high volume of very small deals. They tend to -- we focus on growing assets that we can improve. They're just -- I think Mark most just recently said he's focused on more growthy type assets. Historically, that hasn't been their playbook. They've been more of, as I understand, more of an NPV pure financial buyer. They also tend to -- they incent and provide their feel to do capital deployment. We're very centralized.

And so yes, we are software aggregators or compounders, but the methods are quite different.

We have a lot of respect for what they've done.”

To wrap things up, I scored Roper a 19/25, two points lower (and entirely due to Value/Pricing) than my last time I reviewed the company. This puts it with ServiceNow and Analog Devices in the tech sector on my score sheet, now on Tableau!

Thank you for reading. Please share any thoughts or correct any errors you noticed.

Disclosure:

I do not own ROP stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.