ESAB Corporation (ESAB)

ESAB (Electric Welding) ESAB 0.00%↑ sells welding filler metals and equipment globally. Oscar Kjellberg invented welding and founded ESAB in 1904. Colfax acquired ESAB in 2012 before spinning it off in 2022.

Quality (3/5)

Including its time as a part of Colfax, ESAB has a 3-year revenue CAGR of 13% (pandemic starting point) and 5-year CAGR of 5%. While ESAB is headquartered in the United States, only 22% of sales are within the U.S., with the remaining split between APAC and EMEA regions.

The track record for growth is limited as a standalone company. ESAB was a slow-growth, low-margin business operating in the mature welding market when Colfax bought it. Colfax management was able to improve ESAB’s sales to MSD growth and double EBIT margins to about 15% during its ownership.

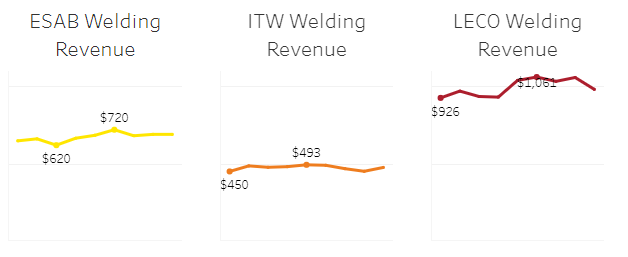

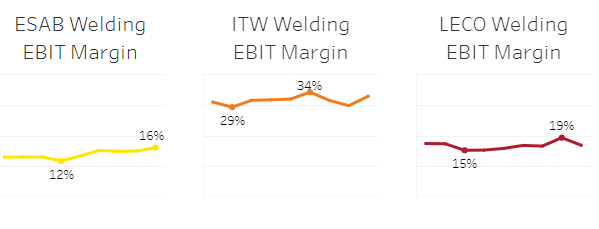

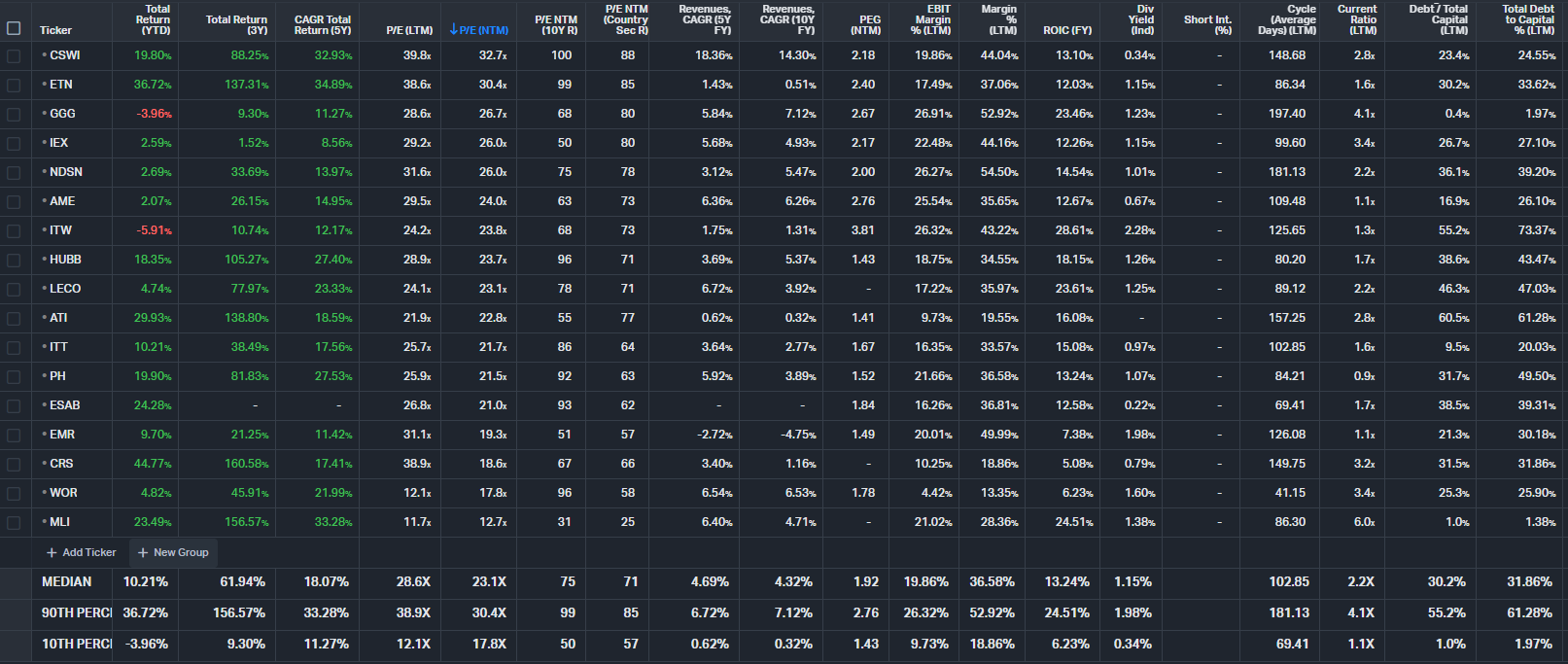

Here is how ESAB compares to its competition:

ESAB looks like the second largest welding company by revenue, behind Lincoln Electric. Lincoln has a higher sales mix to the Americas region compared to ESAB, which carries a higher EBIT margin (19% for Americas vs. 14% for International). ITW Welding is a business segment within the much larger ITW, which could help explain the higher EBIT margins, compared to ESAB and Lincoln that are pure-plays on welding.

Financial leverage (total assets over total equity) is 2.3X, which is not excessive, but it is above the industrial machinery peer median of 1.9X. Welding peers Lincoln Electric and Illinois Tool Works are at 2.6X and 5.2X, respectively.

Visibility (3/5)

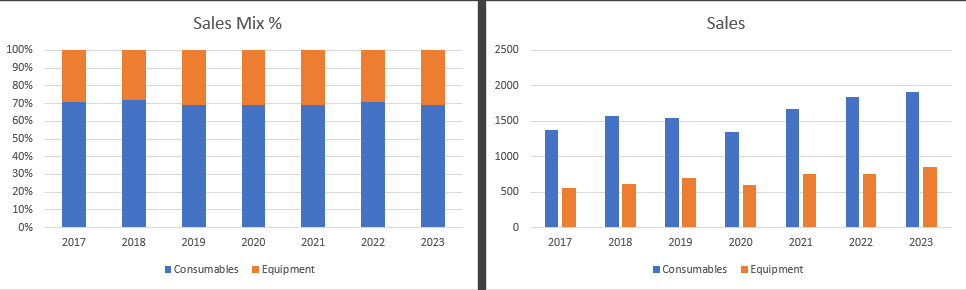

ESAB’s sales mix consists of 69% consumables and 31% equipment. Consumables are fairly stable and predictable, while equipment is expected to continue having higher growth due to new product launches.

ESAB launched software offerings in 2018 that could lead to recurring subscription revenue in the future. It is unclear to me what percentage of total sales are digital subscription sales today.

Forecasting is reasonable due to the welding industry being in a mature stage. ESAB should benefit from many megatrends, including reindustrialization and infrastructure investment in North America. In the long-term, the difficulty will be forecasting manufacturing recessions that are out of ESAB’s control. Near-term, there is some trouble with visibility into weather trends in specific regions.

“But I think we did have weather in the Scandinavian region of Europe and also North America that was a bit severe, we've also had the Chinese New Year falls squarely in February, then we expect Easter to land completely in the first quarter of this year as well.” (ESAB: 2024 Earnings call 4 2023 Transcript, 2024-2-29)

In addition, fluctuations of input costs for raw materials may be difficult to predict in the short-term. ESAB primarily uses steel, iron, copper, and aluminum as inputs.

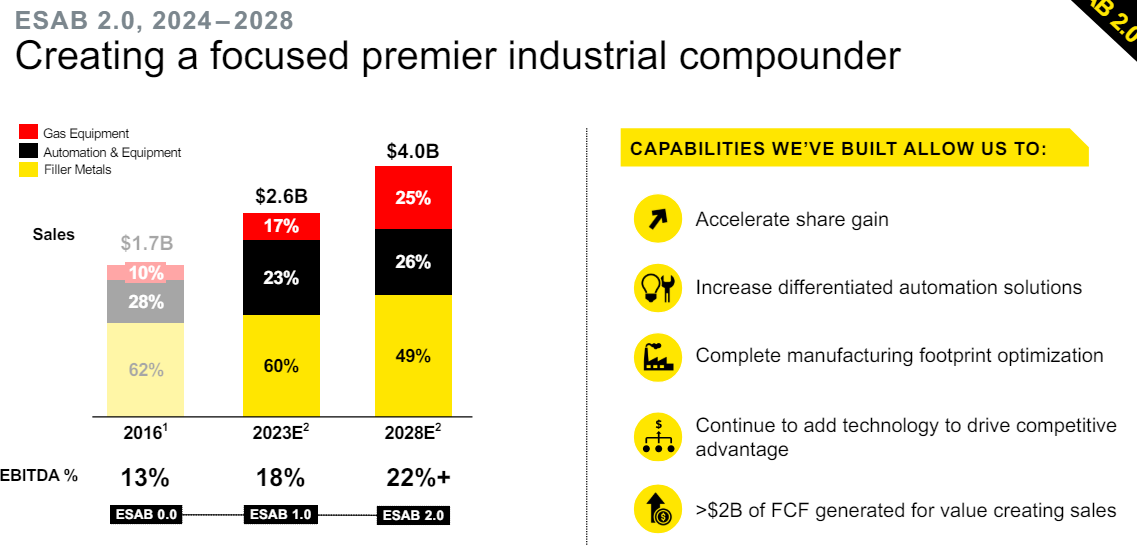

ESAB has financial targets of $4.0B of revenue and 22% EBITDA margin set for 2028:

Welding is not a very flashy business, although, Netflix picked up one season of a welding competition show in 2021 called “Metal Shop Masters” featuring ESAB products.

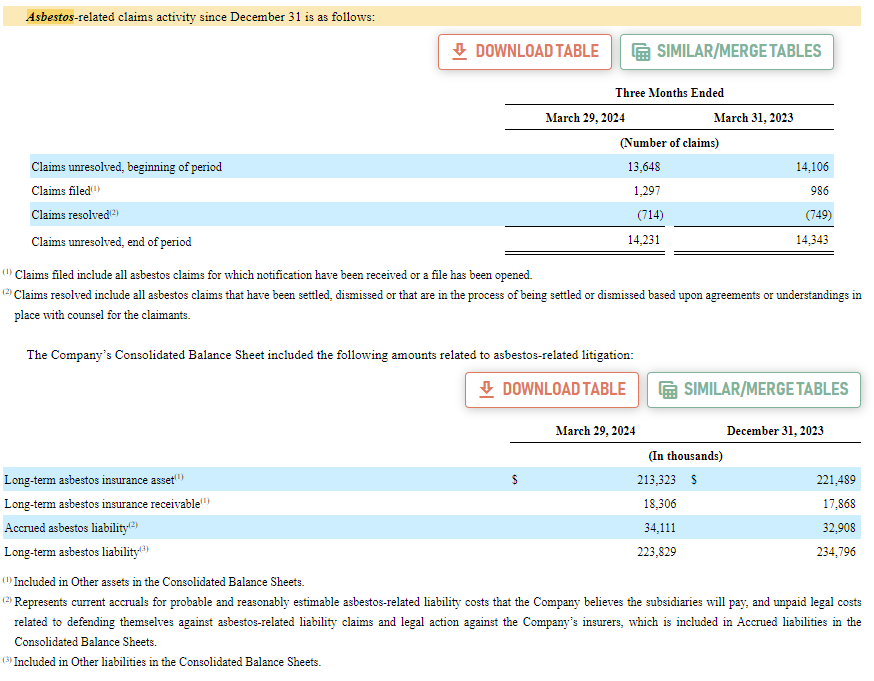

There are some complexities to ESAB’s reporting due to its global reach and non-GAAP adjustments that include restructuring, discrete tax items, and Russian operations. ESAB appears to be still operating in Russia despite saying it would stop after the war broke out.

“For the year ended December 31, 2023, our operations in Russia represented approximately 6% of our total revenue, and approximately $12 million in Net income. Russia also had approximately 4% of our total net assets as of December 31, 2023.”

ESAB NG/GAAP earnings ratio is 1.3X.

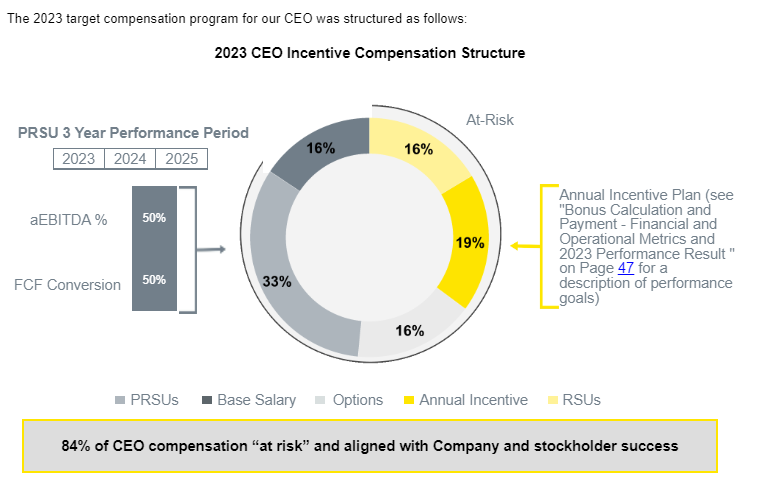

Management (5/5)

Management has been led by CEO Shyam Kambeyanda since 2016. Prior to ESAB, Shyam was at Eaton since 1995. The CFO, Kevin Johnson, started in the role in 2019 after joining Cofax in 2017.

CEO Shyam is incentivized by adjusted EBITDA and free cash flow conversion metrics. Shyam’s total compensation was $7.9M, or 192X the median ESAB employee.

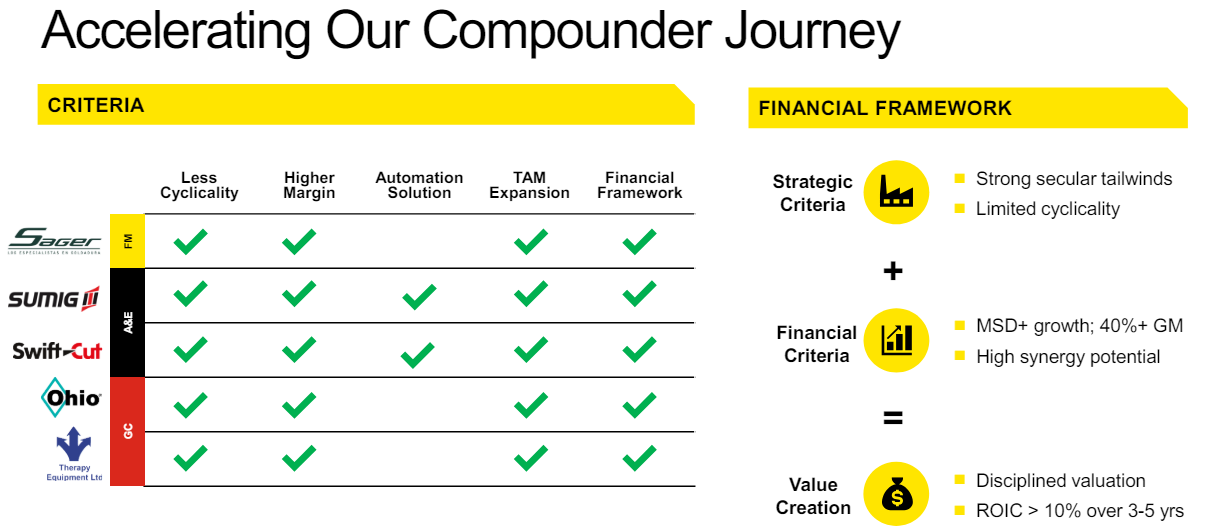

In terms of capital allocation, ESAB is mainly focused on bolt-on acquisitions:

ESAB pays a small dividend, yielding 0.22% currently. Management has not repurchased any shares yet since becoming a standalone company.

I calculate that ESAB generated $1.2B of free cash flow (FCF) cumulatively over the last five years, with a return on invested capital (ROIC) in the low-to-mid teens. SBC is less than 1% of total revenue, and insiders own 7.2% of shares outstanding, according to the latest proxy.

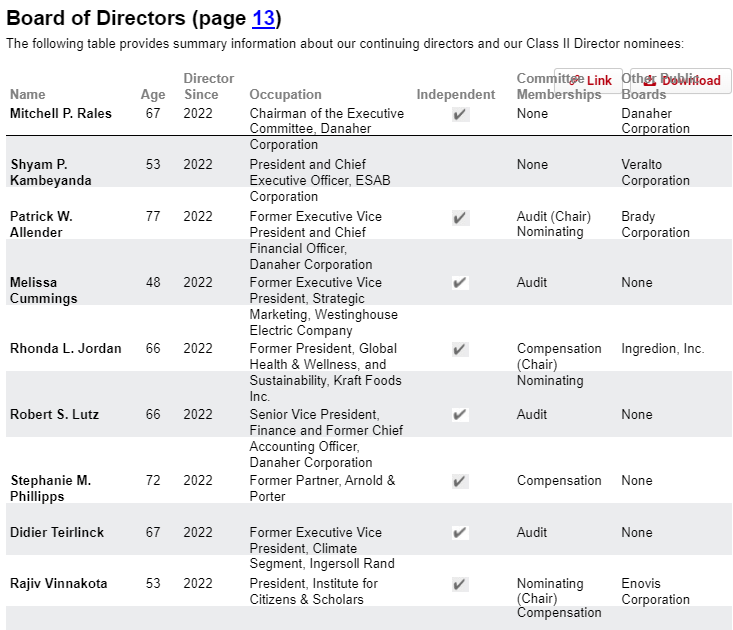

Danaher co-founder Mitchell Rales owns 6.0% of shares out. Another Danaher exec, Patrick Allender, is also on the board of directors.

Demand Creation (4/5)

Demand for ESAB’s products largely comes from capital spending in manufacturing and other industrial end markets. However, I believe ESAB is beginning to show some additional demand creation ability through its more complete “solutions” offerings.

“What I told you before, we were considered a filler metal company. But today, we have a portfolio that we can provide a full workflow solution to our customers. We can provide the equipment, the automation solutions, the robotic torches and the filler metal needed.” (ESAB: 2023 Analyst/Investor ESAB Corporation Transcript, 2023-12-5)

These customized solutions are created in collaboration with customers and could lead to stickier demand.

“Our strategy was to refresh our equipment portfolio, fill product gaps and extend our leadership in gas control equipment while protecting our consumables franchise. I'm proud to say we have made great progress on our equipment offering and have successfully filled our product gaps. Last month, we showcased products like the Volt, the digitally enabled Warrior Edge, and our newly digitally connected Cobot at FABTECH and Essen trade shows, generating significant interest and excitement. We're making substantial investments in marketing, advertising and sales training to leverage our new product offering. These innovations are beginning to bear fruit with equipment and our automation sales seeing high single-digit growth, Cobot sales increasing by triple digits compared to last year.” (ESAB: 2023 Earnings call 3 2023 Transcript, 2023-11-1)

ESAB has a 120-year old, globally recognized brand which many welders learned how to use and trust. Certain welders will be reluctant to switch from their preferred brand. ESAB has a size and scale advantage globally, competing mainly with Lincoln Electric LECO 0.00%↑ and Illinois Tool Works ITW 0.00%↑ , along with smaller local competitors.

“We have a phenomenal emerging market business. We are 4x the size of any of our local competitors in those particular markets. We are also a leader in Europe and we're gaining strength in North America. We win because of our best brands, our strong local teams, and we also have a network of dedicated partners and channel partners. We also have global scale that we can provide to our local customers.” (ESAB: 2023 Analyst/Investor ESAB Corporation Transcript, 2023-12-5)

Customers appear to like being able to get equipment and filler metal from a one-stop shop like ESAB.

Valuation & Pricing (3/5)

Attached below is my discounted cash flow (DCF) analysis

I set revenue to continue on its MSD-HSD growth path which assumes organic growth of LSD at Filler Metals, MSD-HSD at Automation & Equipment, and MSD at Gas Equipment. ESAB is likely to continue acquiring bolt-on companies to enhance growth. EBIT margins are trending higher and could reach 20%, which is the median margin in the peer group today. My estimated value comes out to $87/share compared to today’s price of $107.

For pricing, ESAB has limited trading history, so I had to look at what peers are priced at. ESAB currently trades for 21X NTM P/E compared to the peer median of 23X. With a less cyclical, higher margin sales mix, I could see ESAB closing the pricing gap between it and its peers. The pricing of this stock reminds me of another spin-off, Carrier (CARR), which we reviewed recently. ESAB also started trading in a lousy stock market environment and traded at 9X earnings. As with Carrier, it seems unlikely to me that ESAB will trade at a multiple like that again soon unless there is a massive global recession. In addition, I believe another 200% return in the stock price (for both ESAB and CARR) over the next 18-24 months is unlikely.

With EPS approaching $5.40, a 23X multiple would equate to $124/share. Combining my valuation and pricing, I am setting a buy-below price of $106 which is $1 less than the current price. Between the decent business score and reasonable pricing, ESAB moves high up on my watchlist!

Risks

Risks include the acquisition strategy, cyclical end markets, and product related liabilities. With the acquisition strategy, there is always a worry that management will overpay for acquisitions to chase growth. We will have to keep an eye on metrics like asset turnover to be sure ESAB’s acquisitions are performing well. Next, if a recession occurs, or if the reindustrialization wave does not form, my earnings estimate at $5.40 would be in jeopardy and the stock could trade significantly lower. Lastly, product liabilities may be a future risk. I see large liabilities on the balance sheet today related to asbestos.

If any further liabilities arise, it could lower the value of ESAB.

To conclude, ESAB scores a 18/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below.

Additional notes:

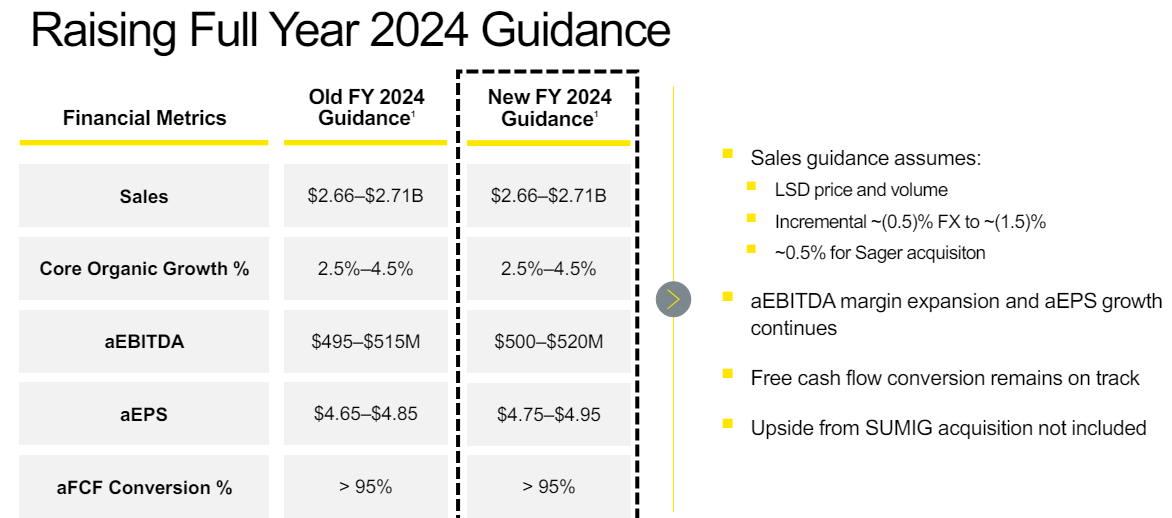

In ESAB’s latest earnings report, management raised guidance for FY24:

Here are some key points of the earnings call using EdmundSEC’s awesome new AI summarizer:

Management Discussion

First Quarter 2024 Highlights

ESAB is progressing towards becoming a premier industrial compounder with higher margins and stronger cash flow.

The company raised its full-year adjusted EBITDA and EPS guidance based on Q1 performance.

ESAB's Future Fabricators program highlights its commitment to community engagement and industry leadership.

Financial Performance

Q1 2024 saw record sales of $656 million and a record adjusted EBITDA of 18.8%, marking 200 basis points of organic sales growth.

Equipment and automation product lines, particularly welding cobots, significantly contributed to growth.

Strong demand in the gas control business, particularly on the industrial side due to energy transition trends.

Question and Answer

ESAB's Use of AI

Question

What are the specific ways in which ESAB is utilizing AI technology and what are the expected benefits?

Answer

ESAB sees AI playing a crucial role in both commercial growth and operational excellence.

The company is focusing on AI applications in material and production planning to drive cost advantages and enhance sales personnel efficiency.

Factors Driving Growth

Question

What are the key factors contributing to ESAB's consistent outgrowth compared to its peers, particularly in the Americas, EMEA, and APAC regions?

Answer

The growth is attributed to the successful expansion of ESAB's equipment portfolio over the past seven years, leading to increased customer and channel partner adoption.

Strong execution and the implementation of standardized processes, such as EBX and sales planning, have also played a significant role in driving growth.

Disclosure:

I did not own ESAB stock at time of writing but I now own it as of June 2024. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.