Eaton (ETN)

Eaton ETN 0.00%↑ offers a wide range of power management products and software. From the product list below, one can see Eaton sells everything from backup power supplies & surge protectors to server racks & enclosures, as well as golf club grips (which reports in the company’s aerospace segment).

Quality (4/5)

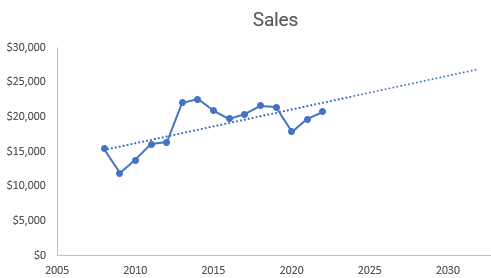

Eaton’s sales have been very lumpy over time due to acquisitions & divestitures, as well as cyclical end markets. The 5-YR sales CAGR ranged from -3% to 5% over the last seven years.

While Eaton is headquartered in Ireland for tax purposes, the company has its 100+ year history rooted in the United States, specifically New Jersey and Ohio. Today, 60% of sales come from the US.

From the Koyfin chart above, Eaton’s sales have many multi-year declines, including in ‘09-10, ‘15-17, and ‘19-21. Despite these declines, free cash flow is moving up and to the right, while the company has paid 15 consecutive increasing dividends at a MSD-HSD growth rate.

Leverage, as measured as Total Assets / Total Equity, is on the low side compared to peers at 2.1X.

Visibility (3/5)

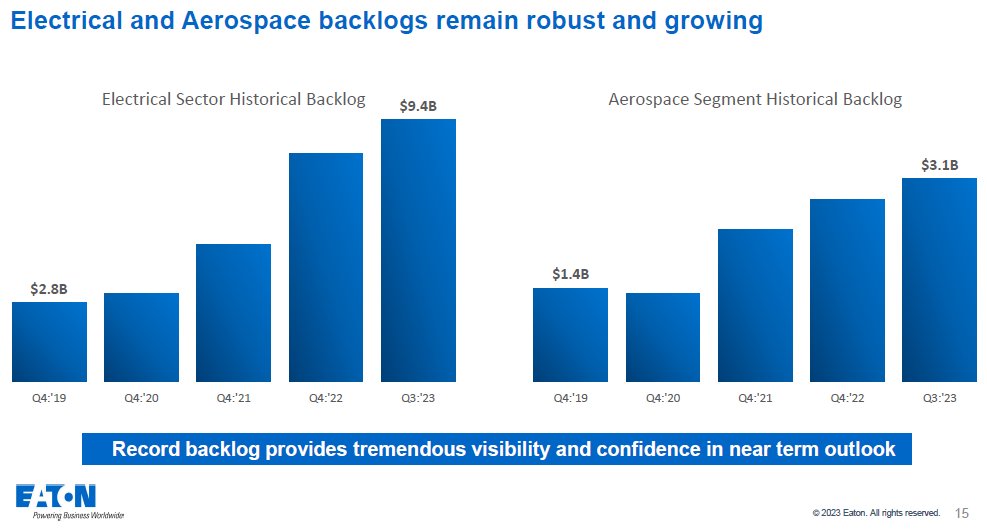

Visibility is improving at Eaton. About 5% of revenue is recurring, compared to only about 2% a few years ago. The company is reporting record backlogs of $9.4B in Electrical and $3.1B in Aerospace.

Eaton is backed by favorable mega-trends in renewable energy, data centers, semiconductors, electric cars, and more. Since the pandemic, Eaton reports $859B in cumulative mega projects across the US and Canada.

Here is how management describes the AI-data center opportunity:

And if you think about the content opportunity for electrical equipment alone in an AI-centric data center, it's 5x the growth, the opportunity when you compare it to a conventional data center. Now having said that, there clearly are some very real constraints in terms of the industry's ability to really deal with the demand that's out in front of us. Huge backlog, huge negotiations. We have historically operated with some 3 years, let's say, of visibility in data center market. We now have more than, in some cases, 5 years of visibility on projects. And so the whole market is just performing extremely well, and we'd expect it to do so for years to come.” (ETN: 2023 Earnings call 3 2023 Transcript, 2023-10-31)

In addition, the utility market opportunity:

Utility market is, historically, as you know, has not been the most exciting end market that we participated in, but we're in a very different world today with respect to climate change, energy transition, you've all seen experiencing some of these global events, whether it's fires or floods. So grid hardening, grid resiliency. There's a lot of dollars today that are being put into the distribution side of the utility market, which is where we play. We're not on the power generation side. For the most part, we're on the distribution side, which is where most of the capital dollars are going. And we're seeing the same thing by the way, in other regions of the world. We're seeing that in Europe. We're seeing that in China as well.” (ETN: 2023 Morgan Stanley’s 11th Annual Laguna Conference Transcript, 2023-9-12)

On the downside, Eaton’s business & financials are complex due to its acquisition & divestiture activity, along with multi-year restructuring programs. Eaton also has legacy obligations through its employee pension plan.

Management (3/5)

Eaton is led by Chairman & CEO Craig Arnold who joined the company in 2000 and has been in the CEO position since 2016. Cumulatively, over the last decade, I calculate that Eaton generated $20B of free cash flow, while spending $12B on acquisitions and $6.5B on share repurchases.

“So our first priority remains investing in each of our businesses to drive organic growth. I strongly believe that if you're in a business, you need to play to win every day. And this means making the resources available to compete effectively and in every business.

Second, we intend to continue to pay an attractive dividend. In fact, we've paid a dividend for the last 98 years.

Third, acquisitions continue to be an important part of our growth and margin expansion strategy. We've done over 70 acquisitions in the last 20 years and see it as an important part of how we continue to transform the company and increase our growth rate.

And lastly, we'll continue to buy back shares, offsetting dilution and being opportunistic as cash builds up.

And turning our attention to financial expectations between now and 2025, here's what we expect. Organic revenue to grow by 5% to 8% a year, up 150 basis points at the midpoint from last year.” (ETN: 2022 Analyst/Investor Eaton Corporation plc Transcript, 2022-3-1)

ROIC, weighed down by acquisitions, is in the HSD-LDD, slightly above my estimated cost of capital. Eaton limits its use of dilutive options. Insiders own 0.5% of shares outstanding. The latest proxy lists adjusted EPS and adjusted OCF as incentives for management. It would be nice to see GAAP EPS, free cash flow, or ROIC as incentives.

Demand Creation (3/5)

Eaton has some ability to create its own demand but it is subject to oil & gas fluctuations, commercial aerospace cycles, and Class 8 truck orders. See the list of markets during the pandemic:

Ignore the Hydraulics segment since that is gone now (acquired by Danfoss), but one can see the evidence of some demand creation in the core Electrical segments. I believe this is due to Eaton’s 100+ years of branding, heritage, and deep domain expertise. Eaton is able to scale this electrical knowledge & technology across industries. Management calls this their “company culture” that leads to a competitive advantage over peers. For example, in power supplies, customers can trust the Eaton brand to keep systems operational during power outages, avoiding large unforeseen costs. There would be a high switching cost to use another, untrusted brand. Management provided this example at its investor day:

“And then Brightlayer, which we've talked about, is driving recurring revenue with Data-as-a-Service. So here's an example. We were engaged by a leading U.S. telecom provider that was experiencing equipment failures and outages. And this led to reduced customer satisfaction and higher annual costs. And outage cost them almost $7 million in losses per year. So our Brightlayer data center suite was deployed to help their network operations center monitor their 1,600 sites and 30,000 pieces of equipment. And our solution helps them predict outages before they occur, by monitoring voltage and frequency usage. So how do we do this? Really, it's our rich history of third-party device integration due to Brightlayer's interoperable architecture and our ability to handle large amounts of data with a scalable database, and that really allowed us to deliver. Providing this Data-as-a-Service, our customer, in this case, experienced a 90% reduction in outages, and we have a multiyear contract with recurring revenue.” (ETN: 2022 Analyst/Investor Eaton Corporation plc Transcript, 2022-3-1)

Pricing & Valuation (2/5)

Attached below is my discounted cash flow (DCF) analysis:

As always, feel free to download the spreadsheet and enter in your own assumptions.

I entered in LDD revenue growth over the next few years to account for the large backlog and strong mega-trends. EBIT margin shows steady improvement from 18.5% today to 20% by the tenth year. Reinvestment in early years is higher to match the higher expected growth. I end up with an estimated value per share of $141, which is 41% below today’s price of $239. I could be too conservative on the growth rates because of Eaton’s low-growth history. I also could be underestimating Eaton’s competitive advantages over time.

For pricing, we see in the Koyfin chart at the beginning of this post that Eaton’s current P/E of 24.5X is well-above the mean of 15X. Eaton’s stock is also getting a premium multiple compared to the SPY ETF, which it has not historically.

Above is Eaton’s percentile ranks compared to itself, US industrials, and the US as a whole. One could make a case that Eaton still looks reasonable compared to the US as a whole. We have looked at many stocks on this blog getting 30, 40, or even 50X multiples in recent years. Say Eaton moves up into LDD or mid-teens growth territory and its mega-project story continues to catch on, could we see Eaton trade for 30X? Maybe. I know I have always just looked at Eaton as a no-growth, market multiple company, so there are probably other doubters out there today.

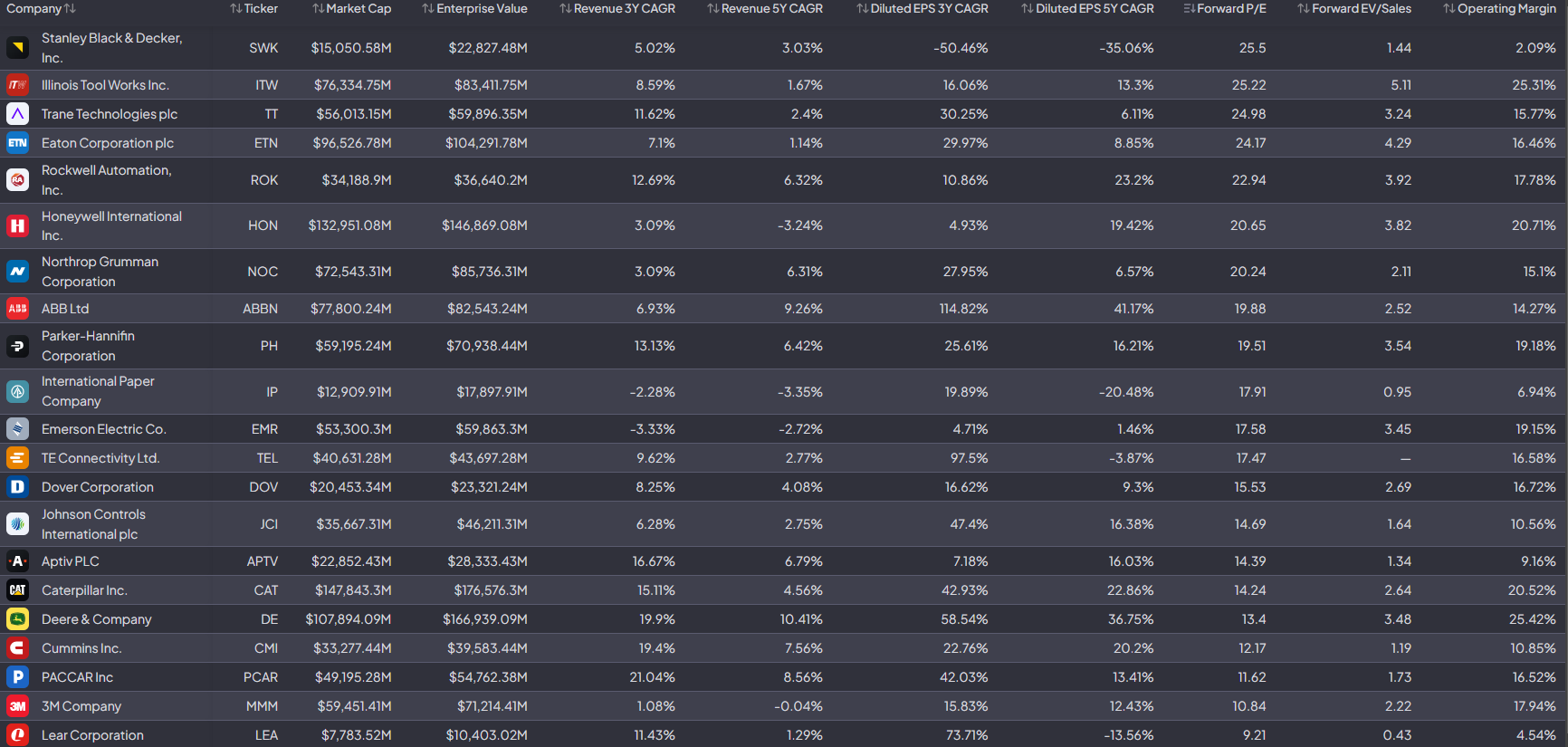

Here is Eaton compared to peers:

Eaton is near the top, in terms of P/E ratio. I think we can take Stanley out of there due to its unusually depressed earnings. Illinois Tool Works, I believe, has always been seen as the premier industrial with high ROIC & margins, so it makes sense to have the highest multiple. The case of a 30X multiple for Eaton weakens here because there are no other large industrials trading at that kind of a multiple today. One would have to go down to the small- or mid-cap pure-plays to find higher multiples.

This is probably too conservative, but I am going with 19X on $10.00 of EPS for a $190/share pricing. Combining my valuation and pricing, I get a target buy-below price of $166, which is 31% below today’s price.

Risks

My risks include too much reliance on the mega-trend story. What if the pandemic growth wears off and the story does not come to fruition? Also, the acquisition & divestiture strategy creates risk of distraction, complexity, and opens the door for financial trickery. Sometimes I like to look at a 3YR GAAP EPS compared to the forecasted adjusted numbers. Eaton’s average 3YR GAAP EPS is $4.99, while forecasts are looking at $10.00+ adjusted. That is a bit concerning to me but maybe earnings will grow so much that even GAAP EPS will look good in a few years. I should mention at this point that management followed the trend of moving the company to Ireland in the early 2010s for tax purposes.

Finally, Eaton is historically very cyclical. I know management reduced this cyclicality in recent years, but it worries me to pay a record multiple when everything looks so good for the company. What if end markets slow down and the excuses come back? We will see!

To conclude, Eaton scores a 15/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below.

Disclosure:

I do not own ETN stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.