Core & Main (CNM)

Core & Main CNM 0.00%↑ is a distributor of water infrastructure products in the United States. It has 335 branch locations across 48 states, and is one of two national distributors serving the market (Ferguson FERG 0.00%↑ is the other). See CNM’s 2023 investor day presentation for a more in-depth look at their business.

Quality (3/5)

Core & Main scores points in the Quality category for having sustainable mid-single digits (MSD) organic growth and 100% U.S. sales mix.

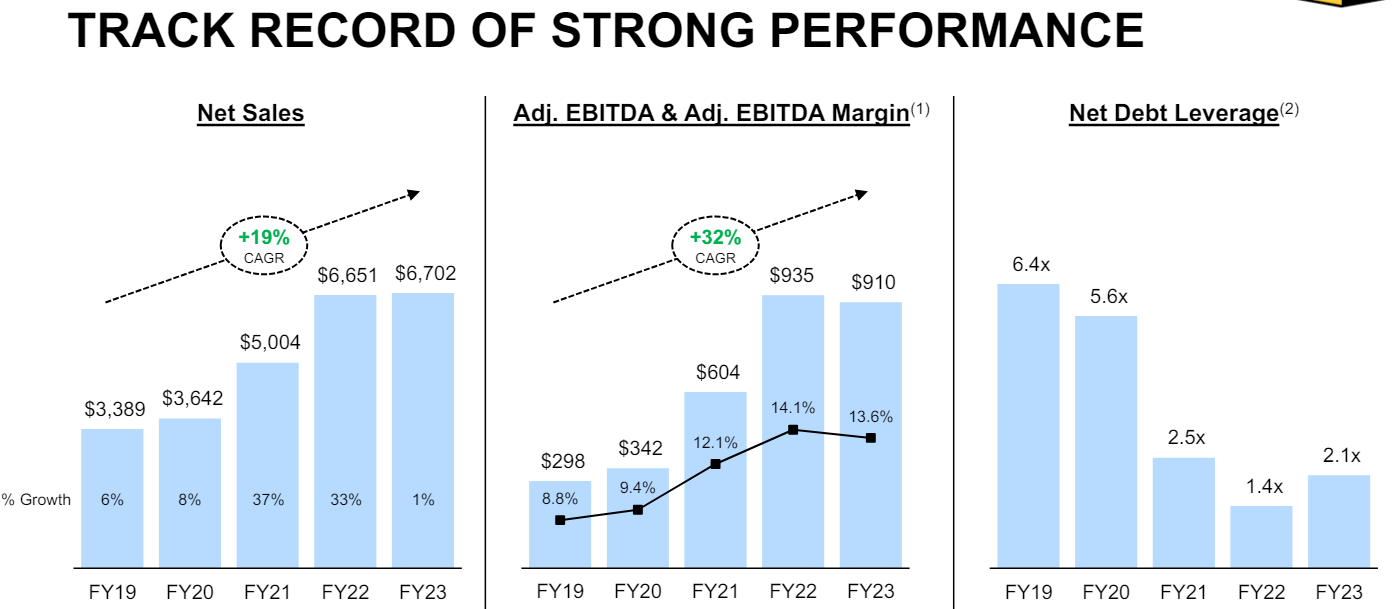

The recent high-teens growth rate may be difficult to maintain in the long-run without several larger inorganic acquisitions and further gains due to price inflation. During the time that CNM’s revenue was growing 30%+, management cited that 3/4th of that growth was due to price inflation, as plastic water pipe prices increased greatly during the pandemic. It seems reasonable to expect HSD total growth through a combination of MSD organic + MSD acquisition over time.

While Core & Main can trace its roots back to 1874, it has limited history as an independently traded public company. Home Depot acquired National Waterworks in 2005, merged it with Hughes Supply, and formed HD Supply Waterworks. In 2017, private equity firm CD&R acquired HD Supply and renamed it Core & Main.

CNM does not currently pay a dividend. As seen in the slide above, leverage has declined significantly. Financial leverage, measured as total assets over total equity, still remains the highest in the peer group at 3.33X. I will have the peer group chart later in the Pricing section of this post. Overall, CNM loses two points for unsustainable price inflation gains, high debt, and low cash balance.

Visibility (4/5)

I like the visibility of CNM’s business with 50% of sales coming from repairs & replacements. When a water pipe breaks, that is hugely disruptive to the municipality, requiring immediate replacement no matter what kind of economic condition the world is currently in. In addition, with the average age of pipe being 45 years old, that is going to require significant repairs and replacements over the next decade.

Above are slides that explain CNM’s solid visibility in the long-run. There is significant underinvestment in water infrastructure and an increasing need for residential & non-residential development to meet low supply. CNM cites the need for $2.2 trillion of spending required for repairs and upgrades over the next 20 years. The Infrastructure Investment & Jobs Act (IIJA) is designed to aid investments in expanding access to clean drinking water, protect against increasingly severe weather, and repair roads & bridges. CNM sees over $17 billion worth of opportunities from these investments.

While that seems like a lot of potential revenue, it is going to take years to tackle those opportunities. According to the latest earnings release (summarized by EdmundSEC),

“The company views IIJA as potential upside but has not included significant contributions in the 2024 guidance, as orders and deliveries are not yet materializing despite signs of opportunities in treatment plant operations.

The company anticipates a minor acceleration in IIJA-related activity this year, with incremental growth expected in the municipal segment over the next several years as funds flow and projects are scoped out.

IIJA is not expected to be a one-time event but rather a long-term driver of demand, as municipalities borrow from state revolving funds and create a regenerative funding source.”

I also give Visibility points to Core & Main for operating in a boring business (it does not get much more boring than water pipes!) and limiting non-GAAP use to adjusted EBITDA. It is not a perfect score here because the other 50% of sales is from New Construction, which can be cyclical and unpredictable.

“As Steve mentioned earlier, we are now beginning to see pockets of softness for new non-residential project starts in select markets. Based on our backlog, bidding activity and order pace, we expect the non-residential market to be down low single-digits for the year.” (CNM: 2023 Earnings call Q2 2023 Transcript, 2023-9-6)

Above is an example of how management discusses headwinds in new construction.

Management (4/5)

Core & Main’s management is led by CEO Steve LeClair since 2021. He was previously the President and COO of HD Supply Waterworks, originally joining the company in 2005. Mark Witkowski is the company’s CFO since 2016, joining CNM in 2007 after working 10 years at PricewaterhouseCoopers.

Here, one can see how management is incentivized by adjusted EBITDA and working capital targets. I would prefer to see additional metrics, like free cash flow (FCF) or return on invested capital (ROIC). In addition, from the proxy, one sees that insiders own 3.5% of combined voting power, while CD&R continues to own the majority of shares.

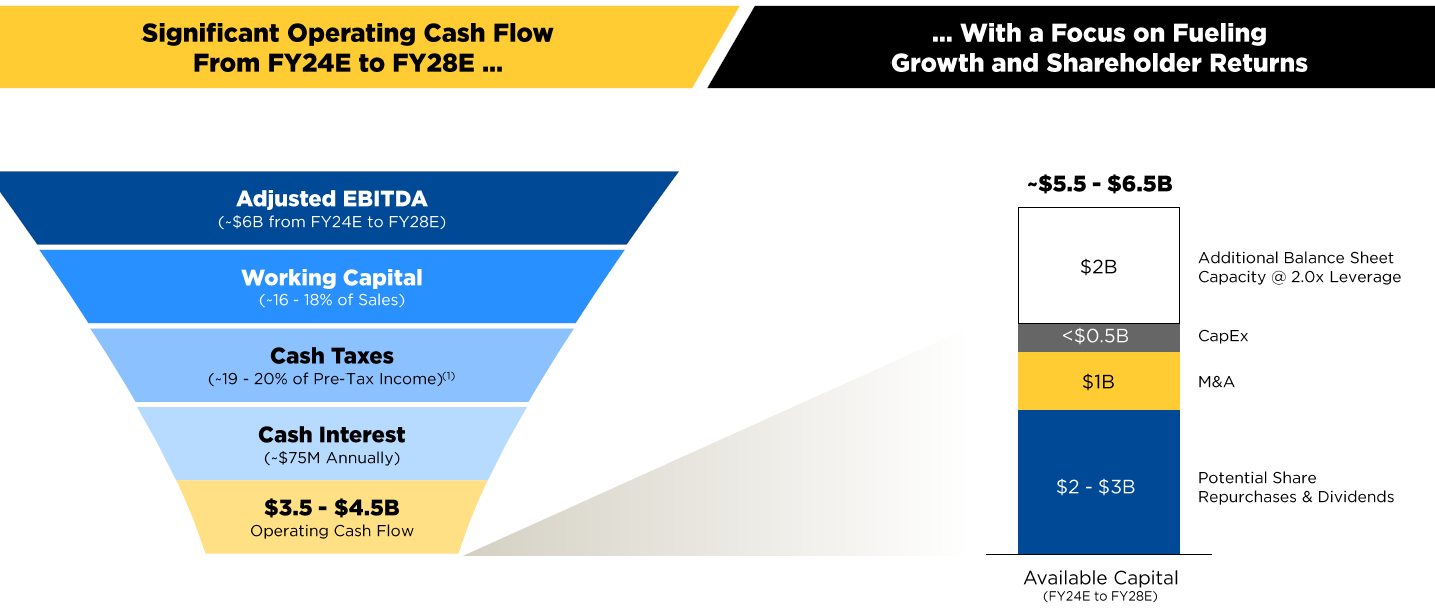

There are six years of financial statements available, where I calculate about $1.8 billion of free cash flow generated cumulatively, with $983 million spent on acquisitions. ROIC is in the mid-teens, nicely above my estimated cost of capital. As shown in the slide above, management plans to deploy $2-3 billion on share repurchases (or a potential dividend), $1 billion on M&A, and less than $500 million on CapEx through FY28.

One of the company’s recent acquisitions was Dana Kepner:

“The Dana Kepner acquisition includes 19 branches with an average size of $300 million in revenue, and it is expected to be slightly accretive to the bottom line. [107]

The size of the deal and the reputation of Dana Kepner as a respected regional player in the industry contributed to a higher multiple. [186]

The company sees great synergies with Dana Kepner, particularly in product categories, customer profiles, and geographic fit, and views the deal as complementary rather than a risk of cannibalization. [187][188][191][192][193]” - summarized by EdmundSEC

Demand Creation (4/5)

The majority of demand creation is coming from much-needed infrastructure investments by municipalities in the U.S. CNM creates additional demand through its acquisition strategy, which increases its size & scale and diversifies its services & product offerings.

CNM competes with Ferguson nationwide (FERG has over 1,500 branch locations) and local players on a smaller scale. Regulations vary by municipality, creating complex specifications that require local knowledge, resulting in high barriers to entry.

“Our customers choose us for our breadth of products and services, extensive industry knowledge, familiarity with local municipal specifications, convenient branch locations and project management capabilities. We utilize our deep supply chain relationships to provide customers with a “one-stop-shop” experience and customized support in their efforts to maintain and construct water, wastewater, storm drainage and fire protection systems. Our scale and geographic footprint allows us to obtain preferred access to products for our customers, even during periods of material shortages. We have the ability to serve both smaller, local customers and larger, national customers with relevant expertise and the right inventory on hand.” - CNM 10-K

An example of CNM’s competitive advantage is observed when a water main breaks, requiring immediate repair and replacement. CNM has extensive industry knowledge and can be relied upon for promptly developing customized solutions.

Valuation & Pricing (3/5)

Attached below is my discounted cash flow (DCF) analysis:

Management guided FY24 revenue to be up LDD, with a target for FY28 of $10 billion. I set revenue to grow between 8-9% over the next five years which gets the topline close to the $10 billion target by FY28. EBIT margin is already strong at 11%, so I set margin to expand to 13% over the next decade. CNM’s private label strategy should help boost margins over time.

“Private label focuses on non-specified products in fire protection and waterworks, with opportunities in areas like valves, hangers, struts, glands, and accessory packs. [147][148]

The Enviroscape acquisition has contributed to the company's private label strategy, particularly in the geosynthetics business. [125]

The company is expanding its private label offerings beyond geosynthetics to include a broad assortment of products and accessories, with a long-term goal of reaching over 10% private label content. [126][127]” - summarized by EdmundSEC

My estimated cost of capital is relatively low given the 100% U.S. exposure and boring industry. My estimated value per share comes out to $51 compared to today’s price of $59. I think the $59 price assumes more-sustainable LDD growth and even more margin expansion than I estimated.

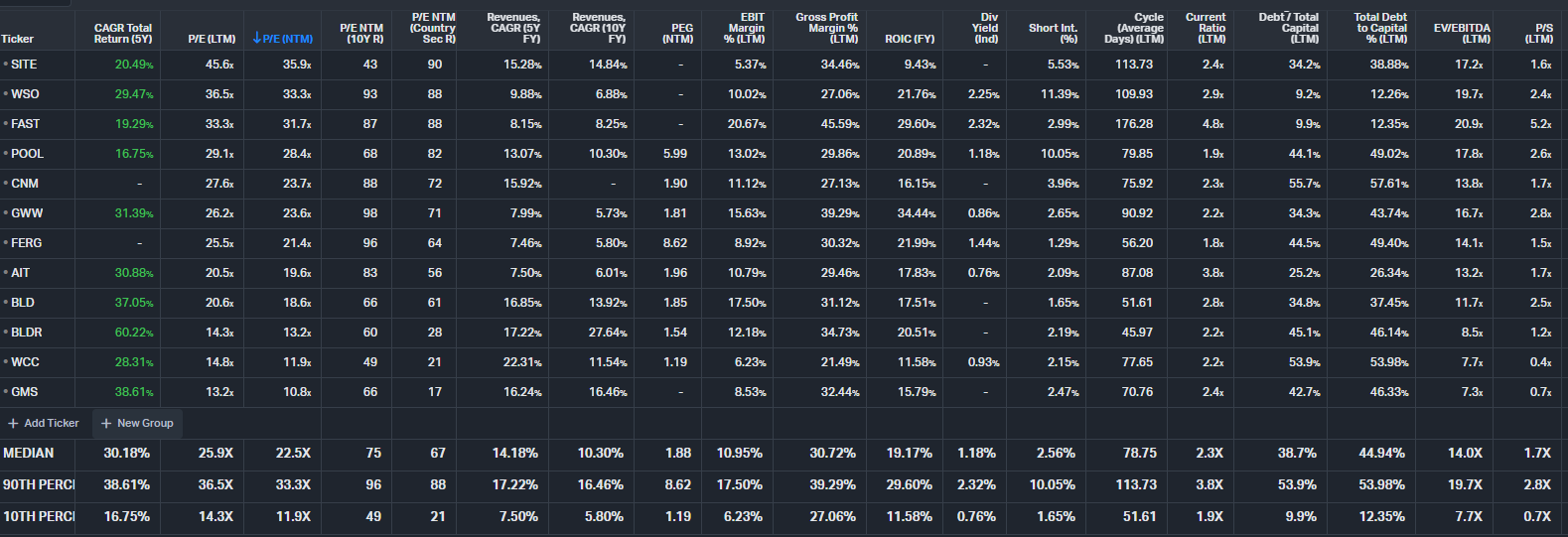

For pricing, given C&M’s limited trading history, I looked at the distributor peer group:

The group’s median P/E (NTM) is 22.5X, so CNM is just above at 23.7X. This is interesting to me given CNM’s median EBIT margin, below-median ROIC, and above-median debt. The higher growth, higher debt companies are getting the lowest multiples right now, except for SiteOne Landscaping (why is that trading at 35.9X?!), so I am not exactly sure why CNM is getting a premium P/E. I could be wrong, but I would not want to pay over 22X, so my pricing comes out to $63 (on $2.85 EPS potential).

Combining my valuation and pricing, my target buy below price is $57, 3% below today’s price. This is another strong business that will move up to a top spot on my watchlist!

Risks

The first risk would be a recession leading to declines in U.S. residential and/or non-residential construction, plus lower municipal spending and/or delays due to budget constraints. The 50% of sales to new construction would be at risk, and obviously, a lot of water infrastructure spending has been kicked down the road for many years, so it could keep getting kicked further if the money is not there. This is why I took a point off in the Demand Creation category.

“Continued interest rate increases or the lack of anticipated interest rate decreases may suppress the U.S. residential and non-residential construction markets that could have a material adverse effect on our business or financial condition.

Economic downturns in any of our markets could reduce municipal tax revenues and the level of infrastructure spending and construction activity and thus our net sales.

Approximately 98% of our net sales volume in fiscal 2023 was facilitated through the extension of credit to our customers whose ability to pay is dependent, in part, upon the economic strength of the industry in the areas in which they operate.” - CNM 10-K

Next, with lofty 2028 targets to reach, management could risk overpaying for acquisitions to meet those sales and adjusted EBITDA incentives in order to receive their bonuses. We will have to keep an eye on metrics like total asset turnover over time to be sure there will not be future write-downs (goodwill and intangibles are nearly 50% of total assets).

Continuing, inflation could dampen CNM’s ability to increase margins over time. Recently, prices of resin, a key input for PVC pipe, increased causing higher product costs and margin headwinds. In addition, CNM operates a fleet of 1,400 trucks. Increasing costs related to repairing and replacing the trucks could impact margins.

Finally, with the nature of CNM’s business installing water pipes, there is product liability risks if the pipes fail or cause health problems.

To conclude, Core & Main scores a 18/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below.

Disclosure:

I do not own CNM stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.