Casey's General Stores (CASY)

After mentioning Casey’s CASY 0.00%↑ in my Murphy USA post last week, I decided to revisit the gas station & convenience store operator that I said I would prefer to own (and have owned in the past).

Quality (5/5)

Casey’s has grown sales at a high-single digit (HSD) rate over time, with inside same-store sales (SSS) growing in the mid-single digits (MSD). Revenue is 100% U.S.-based with the vast majority coming from the Midwest. There is a great Business Breakdowns podcast on Casey’s if you are interested in a deeper dive than what I will do here today.

Revenue declined in ‘09-10, ‘15-16, and 2020 due to declines in retail fuel. However, when looking at inside-SSS, that has grown for 22 consecutive years, a major differentiator for Casey’s. In addition, the company is on 24 consecutive years of dividend growth.

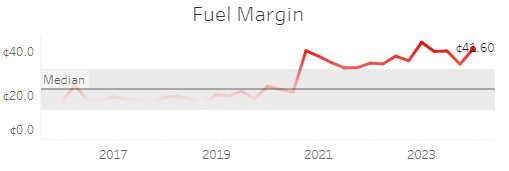

I made a Tableau dashboard with recent quarterly segment trends. Check out how fuel margins exploded higher after the pandemic:

Lastly, unlike Murphy USA MUSA 0.00%↑ , Casey’s does not use excessive leverage. Total assets / total equity is only around 2.2X.

Visibility (3/5)

Casey’s successfully rolled out a rewards program and mobile app (built on SAP, Salesforce, and MuleSoft) that today has 6.4M members. This gives some resemblance of recurring revenue because rewards members visit stores 15% more frequently than non-rewards and spend 12% more per transaction, according to the company. While selling gas, pizza, and cigarettes in rural areas sounds boring, there are some complexities to the business. Retail fuel, traffic trends, and competitor promotions can be very difficult to forecast. Management has also struggled to meet SSS guidance in the past, blaming the farm economy, the price spread between food at home and food away from home, and weather. I even recall management blaming leap year on a SSS miss.

Management (3/5)

There is an entirely new management team since 2019, none of which have experience at Casey’s before. It is quite a switch from when Terry Handley was CEO and Bill Walljasper was CFO, both of who were executive officers at the company for close to 15 years.

CEO Rebelez had roles at IHOP and 7-Eleven before joining Casey’s. Between the two management teams, Casey’s generated about $1.3B of free cash flow (FCF) cumulatively over the last decade, while spending an equal amount of $1.3B on acquisitions.

Management does not use share buybacks often. Over the last 15 years, there was a $300M buyback between 2017-2019 and a $500M buyback in 2011. I calculate return on invested capital (ROIC) of around 12% compared to a cost of capital around 6%. Stock-based compensation is less than 1% of total revenue. Insiders own less than 1% of shares outstanding. It would be nice to see more insider ownership!

Demand Creation (4/5)

While I do not see any demand creation ability when it comes to selling fuel, I see some signs of it with Casey’s inside sales, especially its fresh food offerings. The company has been successful with targeting small town with a lack of shopping options for staples. Over 900 units were built or acquired over the last decade, and 50% of stores are in town with 5K people or fewer. I saw how it was nice to have a Casey’s when I lived in DeKalb, IL. Many retailers ignore smaller towns or farm towns, so it is very convenient to have a Casey’s nearby for fresh food and fuel. Business Breakdowns gives the example of a parent driving the travel baseball team around, needing a reliable place to fill up the car and hungry stomachs. Casey’s saves time and provides great value for this.

It is interesting now, when I am in the Chicago suburbs, Casey’s are showing up in more populated areas after they acquired Bucky’s. I am not so sure yet that they have the same demand creation ability in these areas. The other thing I would note is that on road trips to geographies newer to Casey’s, its stores, in my experience, were lower quality than the ones I was used to in Illinois. Pilot Flying J still has the cleanest, best stops along the interstate.

Casey’s has a size and scale advantage now that they are the third largest convenience chain and fifth largest pizza chain in the U.S. They benefit from cost advantages when sourcing fuel, ingredients, and merchandise, or when building new stores. The company has effectively marketed its brand and provided superior services, as customers see Casey’s as consistent and convenient, while being a good value for money.

Pricing & Value (2/5)

Attached below is my discounted cash flow (DCF) analysis:

Feel free to download the spreadsheet and enter in your own assumptions. It looks like revenue will decline due to lower retail fuel prices this year before bouncing back in the following year. Since it is difficult to predict, I set revenue to be flat in two years. After that, I modeled MSD growth, ending with ~$22B in revenue compared to $14.5B today. I projected small margin improvements. I estimated Casey’s cost of capital at around 6% due to its consumer staple nature and 100% U.S. exposure. In addition, the ten-year treasury rate declined quite a bit in the last month. I end up with an estimated value per share of $196.

In terms of pricing, Casey’s mean P/E ratio is about 20X. The company can have dramatic swings in earnings per share (EPS). Over the last decade, we have seen a 22% and 34% YoY decline, along with increases of 29%, 31%, and 86% YoY. Maybe taking a 3-year average EPS would be helpful.

Right now, the trailing three-year average is around $10.00. EPS this year and next is expected to be $11-12.00, so a forward EPS estimate could be $11.00. Using the mean P/E of 20X, this results in a $220 price. This makes sense too when comparing to peers.

Given Casey’s consumer staple-like business, it should trade at a higher multiple than companies that rely more on fuel and the oil & gas market. However, I do not think Casey’s is as high-quality as Costco.

Combining my valuation and pricing, I target a buy-below price of $208, compared to today’s price of $275. I would definitely like to own this one again!

Risks

I see similar risks as mentioned in the Murphy USA post. Casey’s does sell gas and cigarettes which could make it a quick “no” for certain investors. The risk of electric vehicles applies to Casey’s as well, although, it seems management is more interested in this area compared to Murphy. In June 2023, management stated,

We're not reliant on fuel to drive traffic to our stores as approximately 75% of our transactions do not even include a fuel purchase.

As we noted, fuel demand is changing, as fuel efficiency, CAFE standards and driving behaviors have all played a role. We're also actively monitoring electric vehicles, although there's very limited penetration in our geography. We're actively engaged with the states in our footprint for funding and we have 29 stores with 138 chargers supporting EV charging, and we rely on outside funding for these sites at the present time.

In addition,

I'm not sure there's a day that goes by we don't hear something about electric vehicle growth across the industry. But as we heard from Darren earlier, we've actually been quietly building out an EV portfolio ourselves.

And so as we sit here today, we have 29 locations with chargers, 138 chargers at those locations. What we're seeing from a transaction base is about 4% of total transactions are from EV transactions locally at those locations.

And so as we look at where we should go from here, one of the metrics we really, really focus on is EV registrations as a percent of total vehicle registrations. And so in our footprint, that number is only about 0.6%.

So a pretty small number for us. Despite that absolute lower number for growth, it's hard to deny we're seeing a lot of funds enter this space, a lot of capital enter this space. And so that's coming from both, public and private funds.

And so we've really taken a step back over the last year, evaluated the broader EV market and feel like we have a really good plan to be able to grow at the right pace, at the right locations and of course, make sure we're leveraging the third-party funds that are available.

I noted that Murphy is spending billions on share buybacks, making me worry they could miss the potential EV boat. I do not have that same worry with Casey’s at this point.

The thing I am more interested in is acquisitions like Bucky’s that puts Casey’s in highly populated areas. Does the demand creation ability hold up at those locations? Are they more profitable or less or the same? One can see the changes occurring at Casey’s: the fresh, new management team with no prior Casey’s experience, the new logo, the new messaging in presentations, etc. To me, it is losing its small-town feel a bit, but that could potentially lead to some big-time profits!

To conclude, Casey’s General Stores scores a 17/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below.

Disclosure:

I do not own CASY stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.

Podcast on breakdown Casey

https://podcasts.apple.com/be/podcast/business-breakdowns/id1559120677?i=1000625360615