Brown-Forman (BF/B)

Brown-Forman sells alcoholic beverages, including the brands Jack Daniel’s, Old Forester, Woodford Reserve, and more.

Quality (4/5)

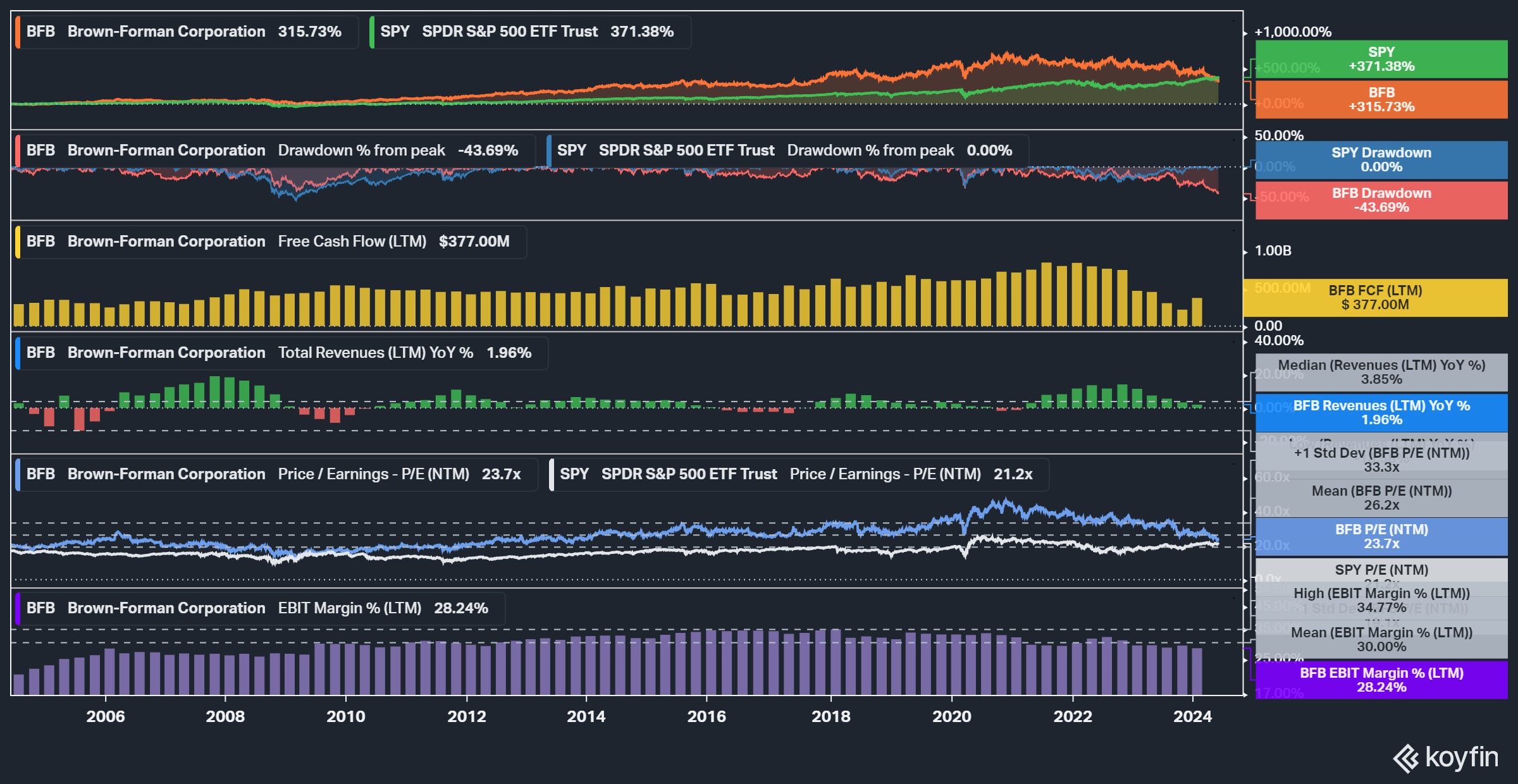

Brown-Forman has consistently posted an organic sales CAGR of 5% over 5-, 10-, and 20-year periods. FY24 organic sales were down -1%, normalizing from pandemic-fueled double-digit growth.

As a member of the S&P 500 Dividend Aristocrats, Brown-Forman has paid a quarterly cash dividend for 80 consecutive years and has increased the dividend for 40 straight years. Its dividend yields almost 2% today, nearly the highest yield in the last 20 years. In addition, the Board has paid out special dividends, with the most recent one in 2022.

Leverage, measured as total assets over total equity, is not excessive at 2.5X today (the beverage peer median is 2X), and is down from 3.5X five years ago.

Visibility (4/5)

Visibility for Brown-Forman has weakened in recent years due to foreign exchange headwinds, wood & agave cost increases, tariffs, and supply chain disruptions. Gross margin is around 60% today, down from 70% ten years ago.

As an example of lower visibility, for FY24, management guided organic sales growth of 5 to 7% with organic EBIT growth of 6 to 8%. Actual FY24 results showed an organic sales decline of 1% and an organic EBIT decline of 2%. The guidance for FY25 again sees growth, with both organic sales and EBIT expected to be up 2 to 4%.

The company has some sales concentration with two large customers accounting for 14% and 12% of net sales, respectively.

Management (4/5)

Management is led by CEO Lawson Whiting (since 2019), who began his career at Brown-Forman in 1997 in the corporate development group. Joining him is CFO Leanne Cunningham, who has been with Brown-Forman since 1995. A great-great grandson of Brown-Forman’s founder, Campbell Brown is the Chair of the Board.

Cumulatively, over the last decade, the company generated almost $6 billion of free cash flow (FCF), while spending $1.5 billion on acquisitions ($1.2 billion of that was spent in 2023). Recent portfolio moves include:

“During the third quarter of fiscal 2023, we acquired Gin Mare Brand, S.L.U. and Mareliquid Vantguard, S.L.U., which owned the Gin Mare brand (Gin Mare).

During the third quarter of fiscal 2023, we acquired (a) International Rum and Spirits Distributors Unipessoal, Lda., (b) Diplomático Branding Unipessoal Lda., (c) International Bottling Services, S.A., (d) International Rum & Spirits Marketing Solutions, S.L., and (e) certain assets of Destilerias Unidas Corp., which collectively own the Diplomático Rum brand and related assets (Diplomático).

During the third quarter of fiscal 2024, we sold our Finlandia vodka business, which resulted in a pre-tax gain of $92 million, and entered into a related transition services agreement (TSA) for this business.

During the fourth quarter of fiscal 2024, we sold our Sonoma-Cutrer wine business in exchange for an ownership percentage of 21.4% in The Duckhorn Portfolio Inc. (Duckhorn) along with $50 million cash and entered into a related TSA for this business. This transaction resulted in a pre-tax gain of $175 million.”

I calculate a median return on invested capital (ROIC) of 20% vs. a cost of capital around 8%.

Stock-based compensation is less than 1% of total revenue.

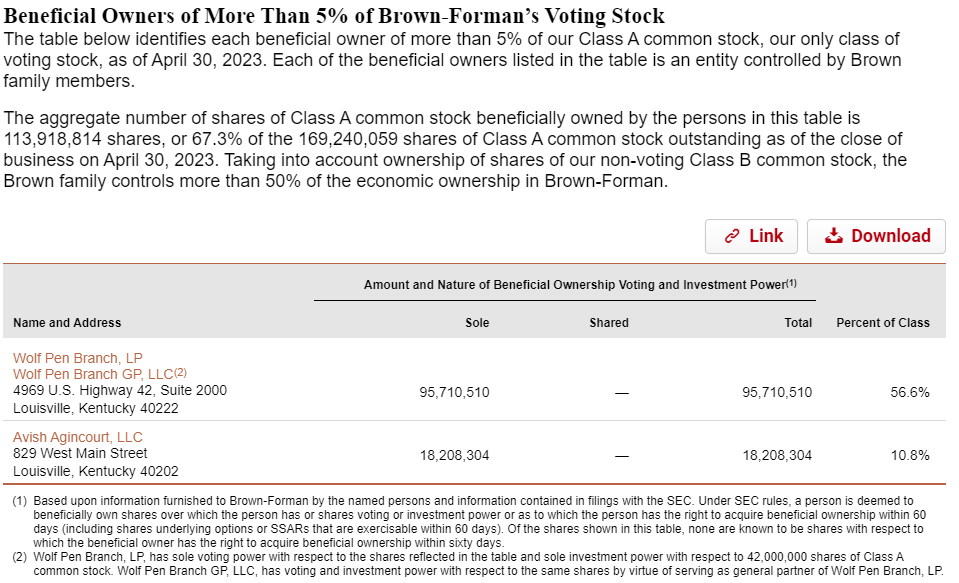

The Brown family controls over 50% of the economic interest and voting power of the company through Class A shares.

Demand Creation (4/5)

Brown-Forman uses its strong brand assets to create demand through product launches that span the price spectrum.

For over 150 years, Brown-Forman has built a reputation for quality and flavor that is difficult to match. Its top brand, Jack Daniel’s, is ranked at the top for best selling whiskey brands in the world. Interbrand ranks Jack Daniel’s as the 85th best overall brand globally.

The company has a size & scale advantage when it comes to procuring raw materials, spending on advertising, and distributing its beverages.

Switching costs would be high for suppliers if they chose not to sell to Brown-Forman given its #1 market share in the U.S. whiskey category. I would imagine bars or stores could potentially lose customers if they were to switch to a competitor brand and not carry Brown-Forman’s beverages.

However, with any consumer brand today, it can be more difficult to maintain brand loyalty as people are inundated with influencers pushing exciting new drink brands 24/7 on Instagram, YouTube, and TikTok.

Valuation & Pricing (3/5)

Attached below is my discounted cash flow analysis (DCF)

I set revenue to stay in the MSD growth range now that we are past the pandemic-fueled growth and subsequent normalization. Management shared at its investor day that EBIT should double by 2032. I have EBIT missing the mark, but not by much. My estimated value comes out to $31/share compared to the current price of $43. To get to $43/share, revenue would have to be consistently in the HSD-LDD range with EBIT exceeding the double target by 2032.

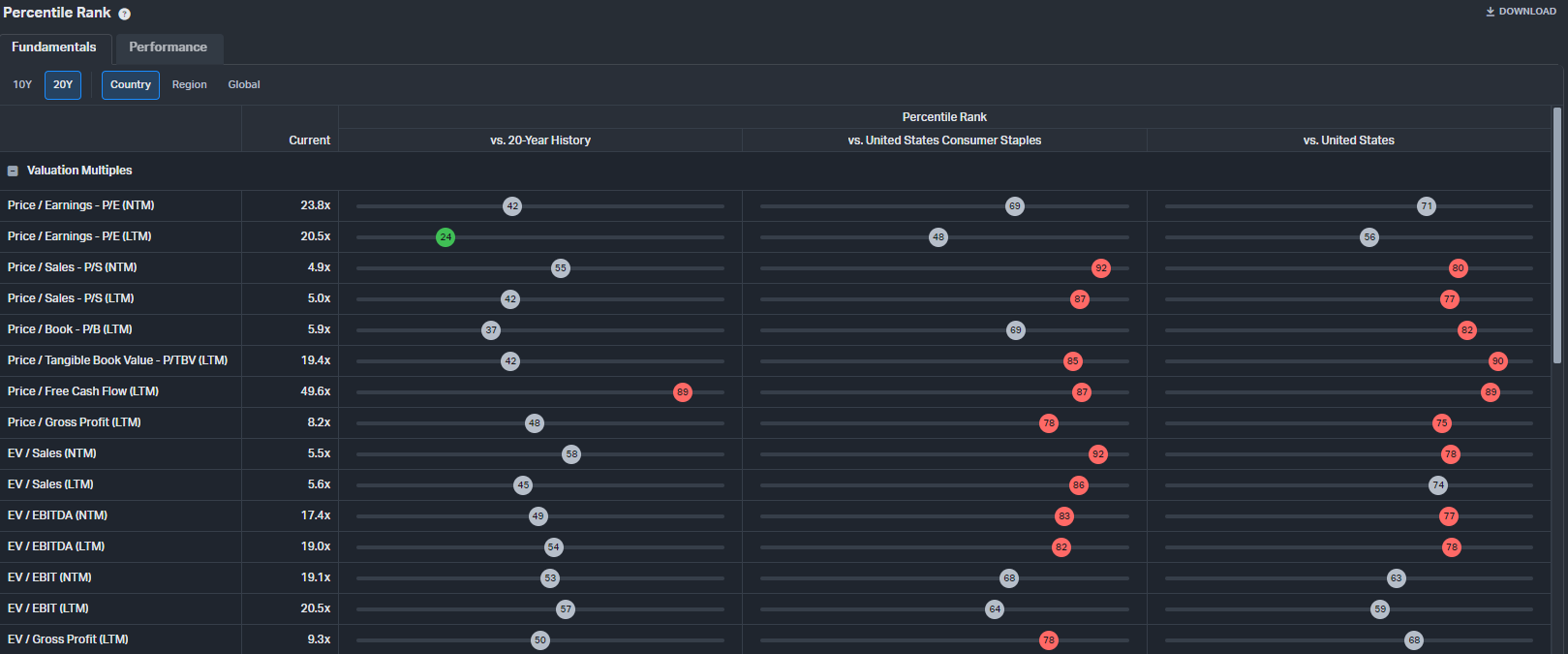

For pricing, Brown-Forman looks attractive relative to itself on most metrics. P/E (NTM) is in the 42nd percentile using the last 20 years.

It is not all good news, though, as we mentioned before, margins are near the lowest that they have been.

Margins are still strong compared to other Consumer Staples and the US market as whole.

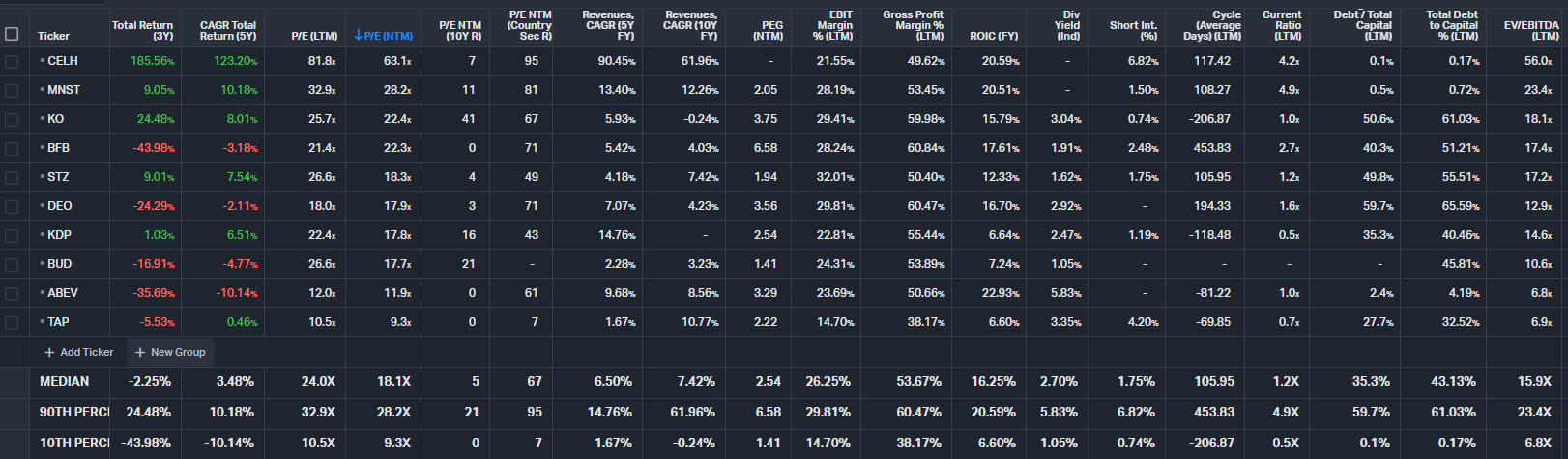

Here is how Brown-Forman is priced compared to peers:

Besides Celsius, this is one of the worst performing peer groups that I have seen lately. Brown-Forman has a -3% 5-year CAGR for its total return. The stock is getting a 22X multiple on NTM EPS, which is higher than the peer median 18X. This makes sense given BF’s leading profitability and reasonable leverage. I think a 26X multiple would be fair, especially if growth picks up after normalizing last year. EPS could get near $2.10 over the next 12-18 months, leading to a $55/share pricing.

Combining my valuation and pricing, my target buy-below price is $43/share, which happens to be equal to the current price. Another good one that moves up to the top of my watchlist!

Risks

One risk is that Gen Z does not drink as much alcohol as prior generations. According to Provi,

“Gen Z is reported to drink less alcohol compared to Millennials and previous generations. A World Finance report shows that Gen Zers drink on average 20 percent less than millennials, who also drink less than older generations.

The increased awareness of the dangers and effects of alcohol and the rise of conscious consumption as a lifestyle is the primary driver of this trend. That same study states that 86 percent of Gen Z consumers believe that their mental health is as significant as their physical health when considering drinking alcohol.”

What may be a positive for Brown-Forman is that the Gen Z’ers drinking alcohol are drinking more premium spirits, which is more inline with BF’s product portfolio:

But not all Gen Zers abstain from consuming alcohol. So what are they drinking? When it comes to what variety of alcohol Gen Zers prefer, spirits have the largest consumption volume. A Statista consumer goods report shows that 25% of the market share for spirit-based seltzers is attributed to consumers aged 21 to 34, more than any other age group. Within the category, tequila and other clear spirits are the preferred choice. Consumers aged 25 to 34 (a mix of older Gen Z and younger Millennials) represented the largest share of tequila drinkers in the United States in 2021 according to the report.

“It is worth noting that it is very early days for Gen Z drinkers in the beverage alcohol market and close monitoring of their behavior over time will be required to see how their tastes evolve,” said Richard Halstead, COO of Consumer Research, IWSR in a report on how Gen Z approaches beverage alcohol. “However, some of their behaviors — reduction in alcohol quantity consumed, preference for cocktails and premium beverages — is also apparent in the preceding generation known as Millennials (aged from their late 20s to early 40s).”

Another risk is that cannabis is being used as an alternative to alcohol. According to CNN,

The use of weed to replace alcohol is a growing trend in the United States. In fact, a recent study found — for the first time ever — the daily use of cannabis of any kind among Americans surpassed the daily use of alcohol.

In sheer numbers, of course, many more people still drink alcohol on occasion than use marijuana, which is now legal for recreational use in 24 states and Washington, DC, and for medical use in 38 states and DC.

Again, this is worth keeping an eye on, but, on its own, I do not think this spells the end for Brown-Forman’s portfolio.

Next, weight-loss drugs may be pressuring the alcohol industry. According to NPR,

"There's really been a large number of clinical and anecdotal reports coming in suggesting that people's drinking behaviors are changing and in some instances pretty substantially while taking [Ozempic or Wegovy]," says Christian Hendershot, a psychologist and addiction researcher at the University of North Carolina.

And once again, it is not all bad news for Brown-Forman’s products:

Ozempic may not work against alcohol for everyone, including people who don't have obesity.

So far, there has only been only one small randomized controlled study, looking at whether another GLP-1 drug could treat alcohol use disorder in people in general, as compared to cognitive behavioral therapy. This drug, called exenatide, isn't as potent as semaglutide (Ozempic) at inducing weight-loss or penetrating inside the brain. In the study, the drug reduced drinking in people with obesity, but it actually increased drinking in people who don't have obesity.

While each risk item may not individually spell the end of Brown-Forman (exaggerating), when combined, they could eat at the margin of Brown-Forman’s sales over the next decade. I would hate to jump into a stock that has good historical fundamentals but is about to be in decline for the next decade. It reminds me a bit of the cigarette stocks Altria and PM.

However, this could also be a case where the market is too negative on the beverage industry, with Brown-Forman as collateral damage, and things turn out not as bad as expected, resulting in a decent return for the stock from here. The industry may simply be digesting a huge increase during the pandemic while investors are coming up with scary bearish narratives that are projected into the foreseeable future. Maybe it will be like the auto-retail industry that we discussed in my latest post about AutoZone.

To conclude, Brown-Forman scores a 19/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below. In addition, please like and share this newsletter if you found it helpful. Your support means a lot and will lead to me being able to continue providing stock research in the future. I also opened up paid subscriptions if you would like to support my work that way.

Disclosure:

I do not own BF.A or BF.B stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.

If Americans ever develop proper taste might Jack Daniels (BF) be toast and the stock never result in attractive returns from here? Especially when I see JD at $100+ a bottle I believe there are much much better alternatives.

Disc.: I never invested in sbux and many other things because of my (bad) personal taste

Pernod Ricard is cheaper, but I have BF/A and BF/B on my watch list. Someone took a run at Brown and Forman a few years back. I may have been Constellation, but I am probably wrong. Given the share structure and large ownership they were able to fend it off. I would own it at a lower P/E, preferably under 20X.