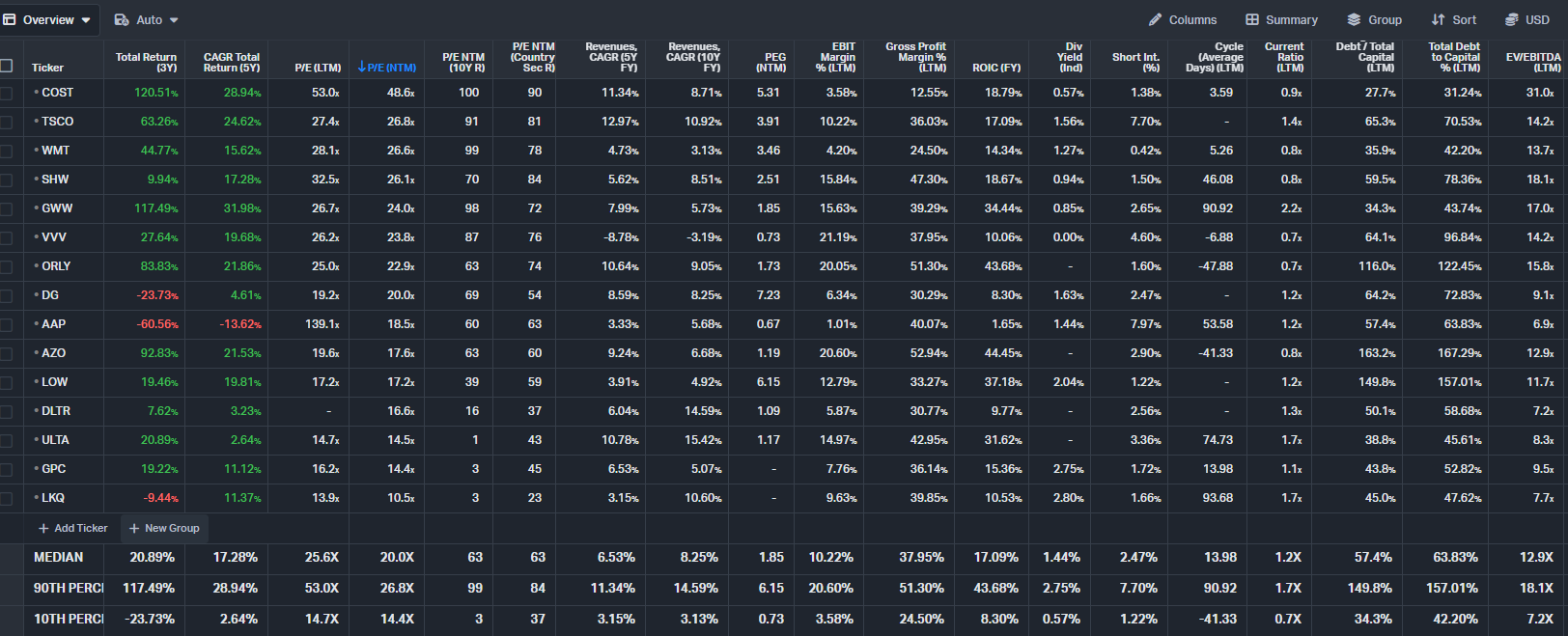

AutoZone (AZO)

AutoZone AZO 0.00%↑ is an auto parts retailer with locations in the United States, Mexico, and Brazil.

Quality (4/5)

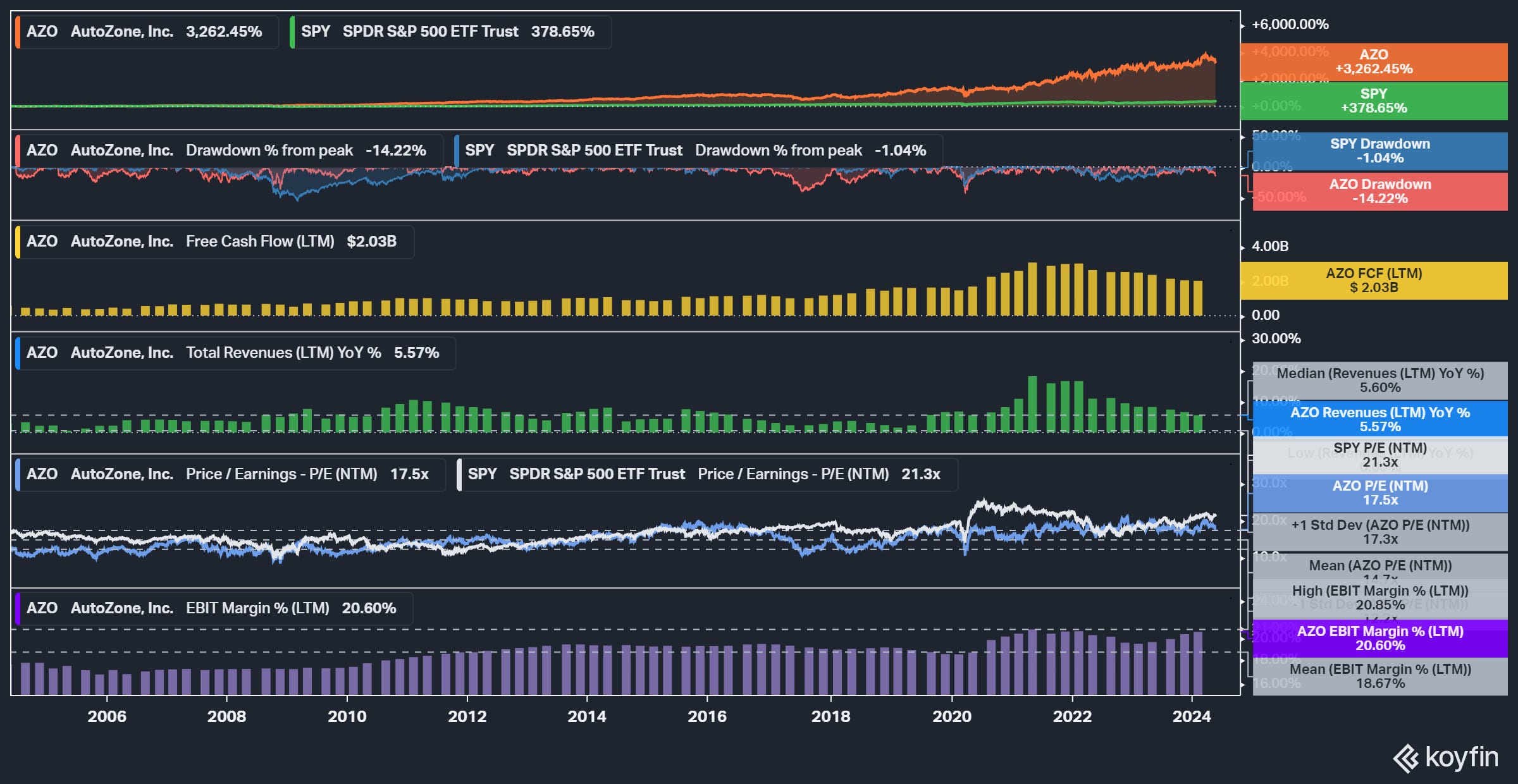

AutoZone, founded in 1979 as Auto Shack, has shown a track record for sustainable growth, emphasizing a long-term, marathon-like approach to success. The company has typically used an organic growth strategy, as opposed to making acquisitions like its peers, leading to a more consistent customer experience. The auto retailer services DIY (do-it-yourself) customers (70% of mix) and DIFM (do-it-for-me) commercial professionals (30%). AutoZone’s revenue CAGR is 9% and 7% over the last five and ten years, respectively.

Visibility (5/5)

Long-term growth is driven by increasing total miles driven and an older car parc. Total miles driven in America is over 3 trillion miles now compared to 2 trillion thirty years ago. The U.S. Energy Information Administration forecasts 4 trillion miles driven twenty years from now (see the CCC Intelligence Report). As cars are increasingly built to higher quality standards, the average age of cars is now 12 years old, making them more prone to broken parts but still worth fixing instead of buying a new car. Parts are becoming more complex, leading to higher price per part.

AutoZone’s integrated IT system helps forecast demand for products and provides visibility to suppliers on necessary parts to ship.

AutoZone is one of the highest sales and earnings certainty companies in the world. There have been no cases of revenue declines on a TTM basis over the last twenty years. Earnings have trended steadily higher despite the Great Recession and Global Pandemic, aided by a large share repurchase program in which shares outstanding have declined from over 80M to 17M during the last twenty years.

Management (5/5)

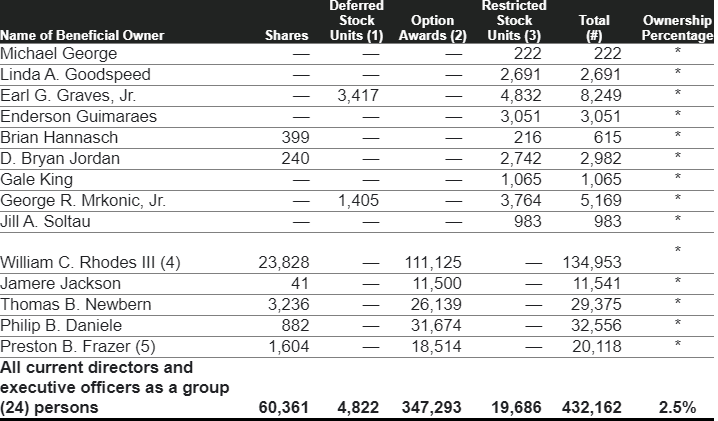

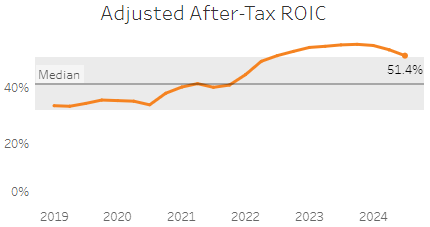

Philip Daniele recently succeeded Bill Rhodes as CEO, bringing 30 years of AutoZone experience to the executive suite. Daniele is joined by CFO Jamere Jackson, who has been in the position since January 2021. Management has preferable long-term incentives, including total shareholder return, EPS, EBIT, and ROIC. Insiders own 2.5% of shares outstanding, according to the latest proxy filing.

In terms of capital allocation, management generated over $17B of FCF cumulatively during the last ten years. Just over $5.5B was spent on Capex, with $500M spent annually on average pre-pandemic, and $700M spent on average post-pandemic. This more aggressive spending pattern is worth keeping an eye on over the next few years.

A cumulative $20B has been spent buying back shares over the last decade, accounting for 84% of operating cash flow. The company does not pay a dividend.

Demand Creation (4/5)

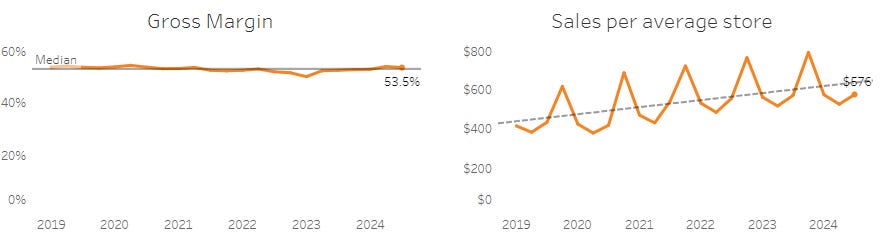

AutoZone’s logistics infrastructure allows for top-notch customer services and availability of parts, leading to gross margin above 50%, sticky customer relationships, and a barrier to new entrants. AutoZone can expand into new geographies, beating local competition with its distribution network and better prices with its size and scale advantage.

Private label sales at AutoZone (including Duralast batteries and SureBilt wrenches) make up about half of total sales, while carrying higher margins due to greater control on pricing and a higher share of profits.

Switching costs can be low in certain situations for DIY customers. For example, I do my own car maintenance and have an AutoZone, O'Reilly, NAPA, and Advance store all the same distance from me to pick from. I shop whichever store has the part in stock or is offering the best deal on the parts I need. In my experience, the Advance store near me had the best customer service, so sometimes I would default to going there, but other times, AutoZone offers me a promotion, so I buy from there. I typically end up at NAPA for more specific parts that the other three retailers do not carry.

In other areas, there may be only one choice or there is one store that is so close, there is no point of going anywhere else. One apartment that I lived at had an AutoZone on the lot adjacent me, so I would shop there every time. One can buy basic car parts at almost any retailer, like Target, Costco, or Walmart, and usually for a cheaper price (I saw Costco had two 5 quarts of full synthetic oil for $38.99 last week vs. AutoZone’s $32.99 for one 5 quart of full synthetic + engine oil filter), but I believe more casual shoppers generally do not know the right part for their car and prefer the service offered at an auto part store. It is very convenient to go up to the desk, have the employee search the computer, and go get the part for you.

Higher volume customers may have a preferred store due to a relationship developed over time or the location. Some professional shops probably order from multiple stores and cancel whichever order does not arrive first.

Valuation & Pricing (3/5)

In my DCF model, I estimate revenue to grow 5% on average over the next decade, with EBIT margin expanding modestly to 22%.

There have been four cases in the last 30 years of the economy going through a significant shock, leading to materially higher growth in sales and profits without a corresponding decline to prior levels for AutoZone. Reinvestment is higher in the near term to match the more aggressive spending by management. My estimated value per share comes out to $2,614 with a 12-month price target of $2,833. Shares look much more attractive than in late March but are still slightly overvalued today. I’ve been valuing AutoZone every year for the past five years and these last 18 months were the first time the stock has been overvalued for me. Shares have been slightly lagging the SPY since late 2022.

I would definitely like to own AZO again in the future!

In terms of pricing, AZO typically trades at a discount to the market. AZO’s 20-year median P/E multiple (NTM) is 14X compared to SPY’s 16X. Compared to ORLY, AZO has always traded at a discount (probably due to AZO’s more-aggressive balance sheet and lower growth). It looks like AZO’s EPS could be around $170 in the next 12-18 months, so I am looking for a 16.5X multiple on the stock as fair value one year out. My buy-below price is going to be the $2,614 that I estimated in my DCF.

Risks

Auto retailers compete with dealerships, warehouse clubs & big box retailers, online shops, and gas stations.

We saw auto retailers, including AutoZone, struggle with slower topline growth in 2016-2018 as the narrative turned negative, focusing on competition from Amazon, Carl Icahn’s Pep Boys acquisition, and the threat of electric & autonomous vehicles.

The Amazon threat fell short because of the non-discretionary nature of car repairs. While planned maintenance, like oil changes or brake replacements, can be ordered online, other repairs require failure parts immediately and Amazon struggles to match the 30-minute windows & in-store help that AutoZone can offer.

Electric cars are exciting to talk about but I believe fears are overblown as electric cars are only expected to be at 12% penetration of the total car parc by 2050, according to the EIA. Electric cars have less moving parts but require more expensive parts and complex repairs. AutoZone should have plenty of runway over the next 30 years even as more electric cars are sold.

Q3 FY24 Earnings Update

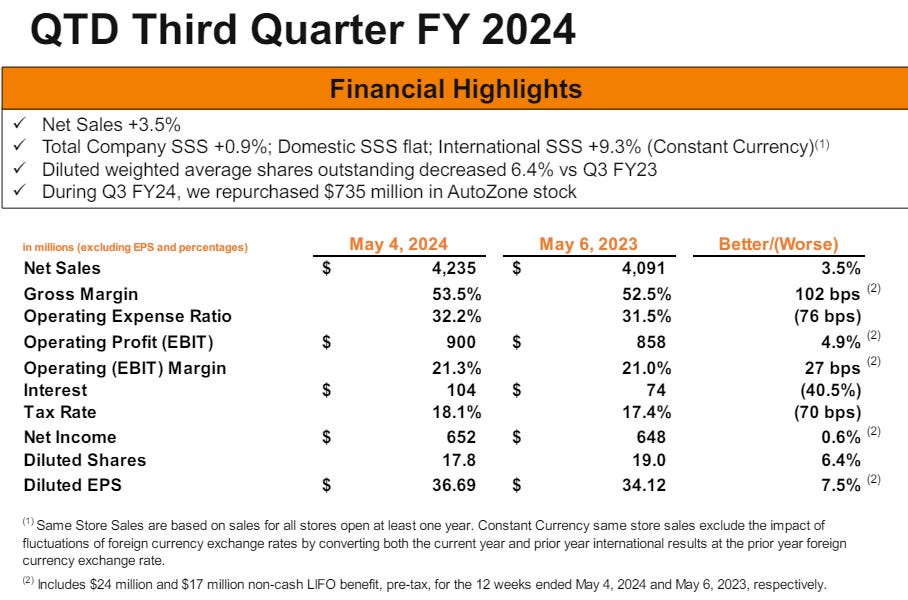

AutoZone reported Q3 FY24 results that showed net sales up 3.5% and flat Domestic SSS. Management noted that sales were negatively impacted by a late start to the tax refund season, along with cooler, wetter weather, particularly in the Northeast and Midwest markets. During the quarter, management repurchased $735M of AutoZone stock, leading to a 6.4% decline in shares outstanding compared to Q3 FY23. Gross margin improved 102 bps to 53.5%, while EBIT margin improved 27 bps to 21.3%.

Commercial business grew 3.3% in Q3, with the strongest performance in the first 8 weeks of the quarter. Two new Mega-Hubs (key growth assets carrying 100,000 SKUs) opened in Q3. The last 4 weeks of the quarter were weaker due to the cooler weather, which impacted categories like A/C chemicals, hard parts, and batteries. These categories should improve as the weather warms up. Management said it has a strong pipeline for future Mega-Hub openings, with plans to accelerate expansion in FY25 and beyond.

In terms of inflation, management notes that ticket growth and overall top-line performance were impacted by more muted trends. Certain highly discretionary items with higher ticket prices have been challenged, leading to slightly fewer items in the basket. According to management, some of this was simply due to weather conditions impacting the timing of maintenance jobs. While discretionary categories have been more impacted, maintenance items show resilience as customers prioritize upkeep of their vehicles to save money in the long run.

To conclude, AutoZone scores a 21/25 in my latest review of the company. See where it stacks up with the other companies I follow, now on Tableau!

Thank you for reading! Please share your thoughts below. In addition, please like and share this newsletter if you found it helpful. Your support means a lot and will lead to me being able to continue providing stock research in the future.

Disclosure:

I do not own AZO stock. Please see my holdings disclosure located in the Google Sheets link.

Any views or opinions are my own. I do not represent a firm. I am not giving financial advice. The stocks that I write about could increase in value, lose value, or stay the same value. Investing involves risk and losses can occur. Some stocks I write about may not be appropriate for you and you should consult a professional investment advisor. Data presented is from sources I believe to be reliable. The opinions and commentary presented reflect my best judgement at this time and may include “forward-looking statements”, all of which are subject to change at any time without obligation to update them. Actual future results may be different than my expectations.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, the author has not independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author assumes no liability for this information and no obligation to update the information or analysis contained herein in the future.